Any idea how much they’ve paid for this new capacity? Earlier they acquired Sarju Impex, is that already delivering CNG cylinder revenues?

3 Likes

Promoters are continuously buying the stock from the open market.

In Q4 so far, promoters have increased their shareholding by 0.47%.

In Q3, they had increased their shareholding by 0.99%.

Since March 2019, in 3 years, they have increased their shareholding by 6.81%.

Open market buying by promoters plus aggressive acquisitions are good signs. EKC and CONFIPET’s actions certainly mean that demand is healthy for the near term (1-2 years at least). Remains to be seen if demand can stay ahead of new capacities coming in.

4 Likes

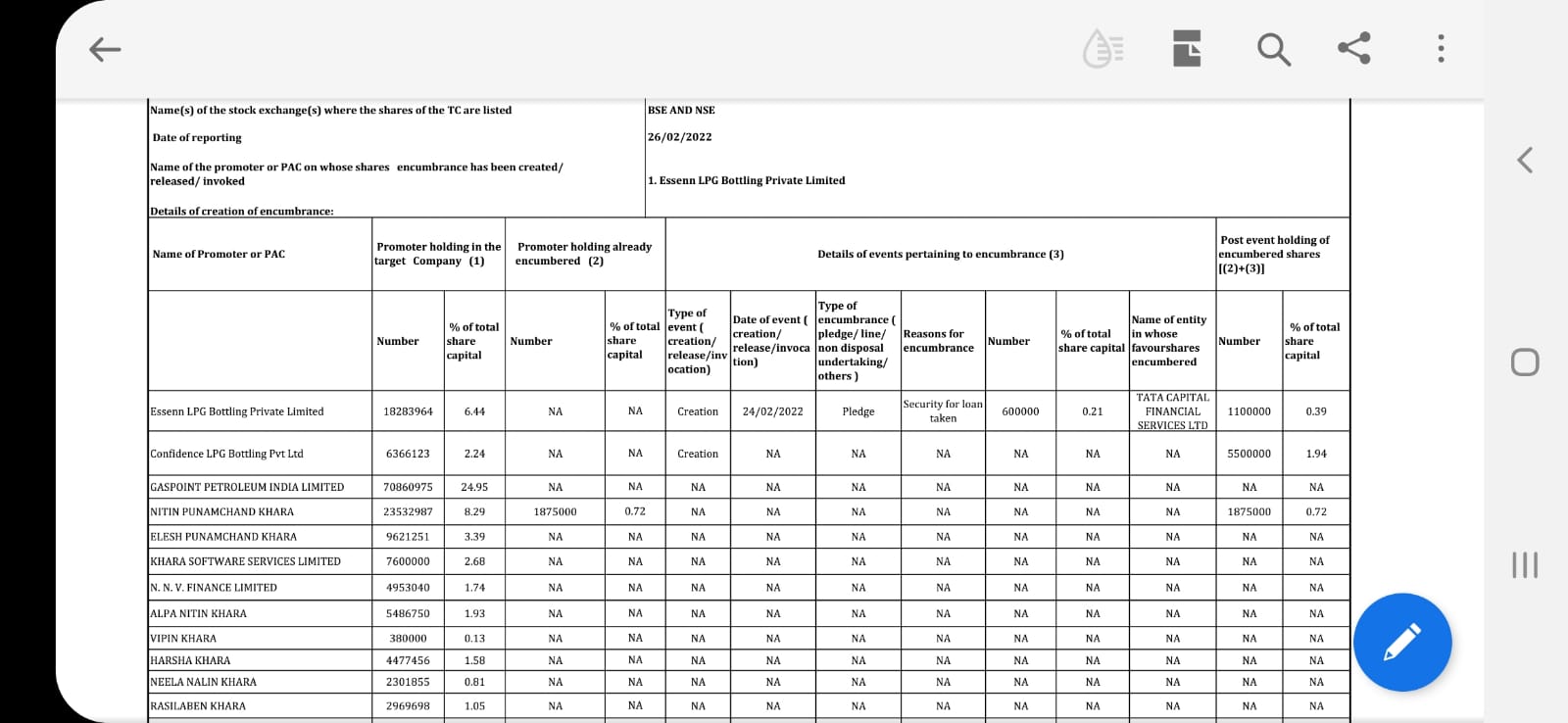

but the last day they pledge a bulk of their shares again after december. It seems they are pledging the double of what they buy in a dip every month. Does it seem like a pump and dump thing?

Sorry but what has a pledge got to do with a pump and dump? Pledge is for taking loans for the company right? I did not get the connection.

Same here. Just calculated quantities they bought and quantities they pledge. It really seems they are pledging more than what they bought. Can any one please explain for what purpose they are doing this pledge?

1 Like

just that by buying small quantities almost every week creating the impression that there is a lot of promoter buying in the company and later pledging the quantity bough together or more to buy again. I noticed the company because of promoter buying and many other people also will be fooled by this buying thing and investing just on the basis of that.

5 Likes

My observations on Micro & small cap cos is many times lenders will also tell promoters to infuse some capital if they are not confident of debt servicing capacity. So its not always negative. We have to wait till next share holding. If promoters are not selling their stakes its very positive sign. I’d guess pledging is because there isn’t enough collateral acceptable to lenders. Which is fine, it happens often. Banks aren’t interested in taking buildings on leased land as collateral, because buildings themselves may not have enough value. I’m just guessing btw, from experience

1 Like

We can check for reason for pledge mentioned in the pledging disclosure. I do not think that lender will insist for any pledging as its financial are not that weak.

It seems that Confidence would not have pledged for their on borrowings but for other promoter Company Esteem LPG.

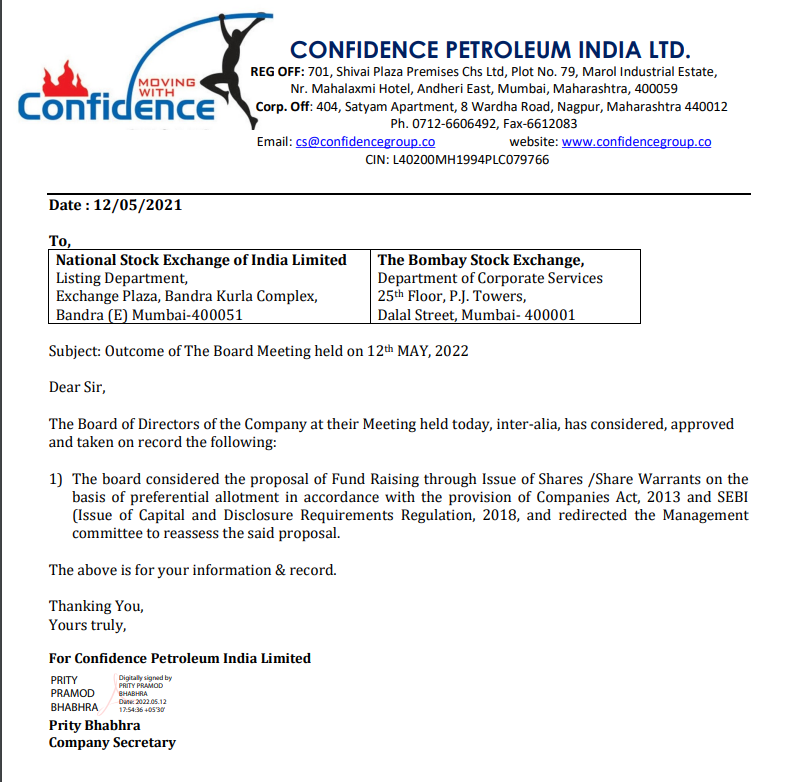

I am a bit surprised why would you do a pref allotment at this price? Unless the promoters want to take advantage of the price and issue themselves warrants by paying a marginal amount upfront.

Confidence Futuristic (listed group company) is probably in operators hand since Pref Allotments were made. These things made me nervous about investment in this company. Promoters lacking clarity.

Disc: Invested in 2020.

1 Like

1 Like

1 Like

Don’t you guys think the projection of 2.5 crores per station per day is a bit ridiculous? More importantly what are the margins the business makes at these levels?

Company intermittently engages with stakeholders which is a bit frustrating.

Clearly 2.5 cr which means 30daysx 2.5cr= 75cr per month per station.if we compare Gujarat price presently which is 82rs. Then company has to sale around 3.04 lakh kg gas per day.i have inquired near by cng station and average sale is around 5000kg with two despense r. Pure cng station which is having generally 6 despenser, we can expect sale around 15000 in kg and 15000x82 =12.8L in value. Company needs to do math check ,I think🤔

4 Likes

In this interview, the management expects to do 5000Kg per day per station after 1 year.

So, that brings a total revenue of 5000*82(cng price)*365(days)*100(stations) = 1496 cr.

2 Likes

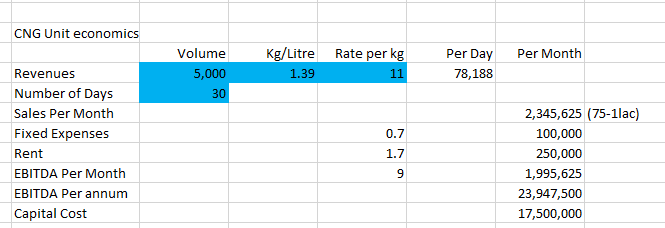

If you listen to the question around minute 58 they talk about the profitability of the business. My rough math gives me 23 alcs of sales per month per station with some crazy EBITDA margins .

We will get a better idea re the unit economics in the next few qtrs since the stations set up during March should be ramping up by H123.

1 Like

1 Like