But as per my understanding postponing of merger should be good for the small company’s shareholders(here in our case it is Astec) as the company would have more chance to grow and reward investors subsequently.And regarding consumption theme,being a Agri player and government’s focus shifting towards agri more day by day,I believe Astec has a good chance to grow manifold in near future.Please correct me If my assumptions are wrong.

The merger had presented an arbitrage opportunity. Godrej Agrovet-Astec merger ratio was 11:10. This attracted a lot of buyers in Astec to make some quick money. I would have understood the sell-off post the demerger was called off. But that Astec is still rushing down South is a mystery to me. I am not sure if they lost any key client.

Quarterly results are due on 26th July. Lets wait to see what the results are. Generally such severe fall is either due to upcoming bad results or maybe some negative news about plants in Mahad (accident, pollution control board permission withdrawl etc). Fingers crossed

Results are out and they have reported loss.sales have improved but the expenses were more.Also the debt levels have increased.Senior boarders please comment on the result.

Since Astec Life does not hold any concalls, we will have to wait for Godrej Agrovet concall to get more clarity on Astec’s results this quarter. On last concall, Mr. Yadav was very optimistic about Astec. Lets wait for his comments on this quarter.

Agrochemicals business are cyclical, and for Astec normally Q1 is muted. Also, I think the reason behind total expenses being high(although COGS are better controlled and relatively lower than QoQ or YoY while finance cost,other expenses & DA looks elevated) maybe due to IND AS 116 ‘leases’ adoption from this quarter. I am also confused since company says that there is no significant material impact due to this. Please correct if this understanding is wrong.

As per IND AS 116, operating leases are no more an off-balance sheet item, due to which lease costs booked under other expenses so far must be shifted to finance cost and depreciation/amortization in P&L(assets are booked at carrying value under BS).

For the first quarter ended June 30, 2019, company reported consolidated total income of Rs.1,713 crore which reflects growth of 15.1%. Consolidated profit before tax of Rs.113 crore was lower as compared to previous year by 5.9%. PAT was down 4.2% YoY at Rs. 77.6 crore in Q1 FY20 as against Rs. 81 crore in Q1 FY19.

Commenting on the performance of the 1QFY20, Mr. B. S. Yadav, Managing Director, Godrej Agrovet Limited, said: I am pleased to share the financials of Godrej Agrovet for quarter ended June 30, 2019. Godrej Agrovet Limited’s consolidated total income registered growth of 15.1% and consolidated profit before tax was Rs.113 crore.

The animal feed segment registered a year-on-year volume growth of 6.5% in this quarter with a strong growth of 17.2% in segment results. Crop protection segment consolidated revenue grew by 11.6% over 1QFY19. However, segment results were flat on account of poor realization. The performance of the vegetable oil segment was adversely impacted by sharp decline in end product prices and lower oil content due to extended summer and extreme heat. Consequently, segment revenue and profits were lower by 13.6% and 64.5% respectively. In the dairy segment, profitability levels improved in the current quarter as there was no butter provisioning / losses which registered a strong growth in EBITDA of 124.3%.

Promoters are taking benefit of lower prices to increase their shareholding in both Astec as well as Godrej Agrovet. In Astec, they have purchased total 156,686 shares from 1st Aug till now through open market purchase. (around 0.8% increase) . Interestingly their MD (and old promoter) Hiremath also purchased 40,000 shares on 1st August (included above)

Astec promoters continues to acquire shares from open market continuously. 46,935 shares purchased in Sept. After break in Oct, purchases once again started in Nov. Around 31,000 shares purchased till 15th Nov (as reported by 19th Nov 19). It seems promoters wants to have bigger piece of future profits as they already have 69.14% shareholding as on 30th Sept 19.

Not able to understand reasoning behind such depressed levels for Godrej Industries. Even if we treat it purely as a holding company, the discount compared to value held is around 60%. This is higher even for a pure-play holding company(eg: Tata Investments has holdco disc of 50%). Add to this the value of Godrej Industries’ own business, doesn’t that make it super cheap at current levels?

Yes wondering why the shares of godrej industries are available so cheap.seems like market forgot they have also chemical business other than being holding company of godrej property,godrej consumer and godrej agrovet.

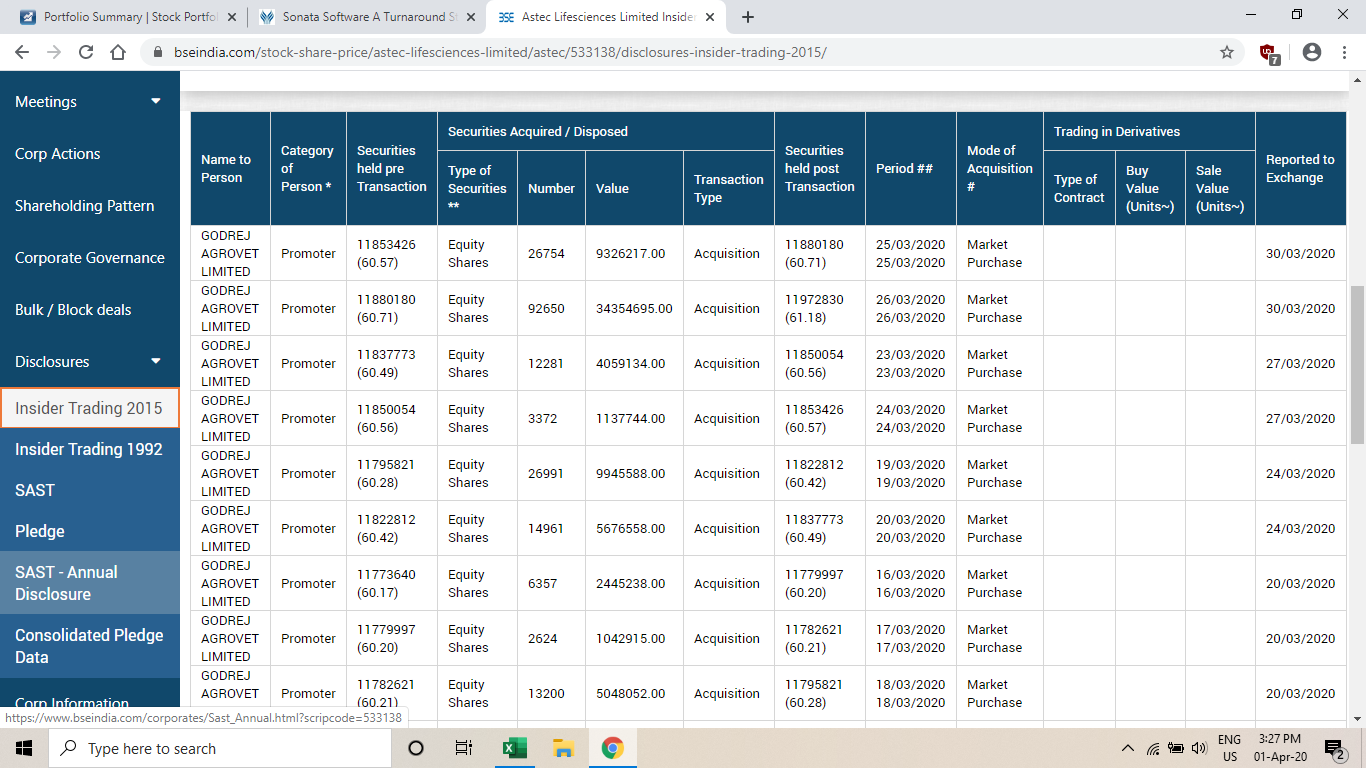

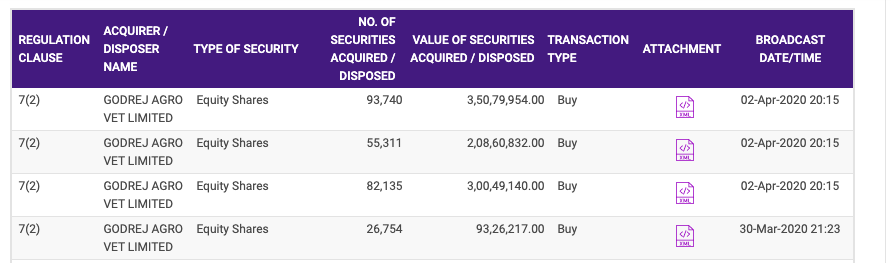

Promoters (Godrej Agrovet) continue to purchase shares of Astec Lifesciences from the market almost on a daily basis. During March 2020, promoters have purchased around 322,000 shares spending around 13 Crores (average price of Rs 400)

Promoters of Astec (Godrej Agrovet) purchased shares worth Rs 8.5 Crores from 27th March to 31st March. Considering urgency of share purchases in recent times, it seems something is cooking…

In addition to buying Agrovet shares, Promoters are also buying Godrej Industries shares.

Promoter holding is up from 61.33% in Jan’19 quarter, to 61.39% in Dec’19 quarter to 62.21% currently. Promoters have nicely used the last 1 month’s carnage to pocket around 0.8% of stake at super depressed levels.

The holding co discount seems to have gone up significantly in this COVID crisis.

Any thoughts on whether this would correct? Any investors here @puneetc,who can discuss governance of this holdco? I read the annual report and it seems they ask for salary etc waivers all the time, but apart from that how is minority shareholder related governance ?

What is the standalone value of Godrej Industries core business alone ?

Its revenue is around 1800-2000 Cr and PAT is 150-200 Cr.

Is it appropriate to give 8 times to get a value of 1200-1600 Cr ?

SOTP of 60% of holding value is 25000 Cr. So core business value is negligible.

As expected, nice pullback in price of over 40% from 230 odd levels. Although the holdco discount has reduced from 67% 3 weeks back to 63% now. It still remains on the higher side among the major holding companies. If the promoter buying seen during April resumes, it would be a great sign.