Astec Acquisition to Help Godrej Agrovet Attain Backward Integration & Strengthen Product Portfolio in the Pesticides Segment ~ Godrej Agrovet accounts ~5% of Astec’s business which is expected to increase to 15% over the medium term. Astec’s Ag Chemical Intermediates (~70%) continues to be on a strong footing ~ pioneer in Triazole based fungicide chemistry – largest player in the domestic market. CRAMS is a very stable business with 20+% margins and it should only go up with Agrovet Acquisition. Reverse Marger with Agrovet is a major trigger in the future.

The Company is shutting stores and moving to e-commerce platform.

From the news article:

“We are at a very interesting inflection point and are committed to redefining India’s freshest and finest food experience. Our transformation journey entails consolidation in certain markets and sustainable profitable growth that will materialize over the next 3 to 5 years. As part of this transformation, we will serve our customers through the brick and mortar stores in certain markets and through the online channel in all markets,” Davda said.

I was always skeptical about their retail foray. However after demonitization, i thought the sales at natures basket would really pick up. It’s strange that they had to close in the midst of demonitization. ( As they accept cards while most kirana and veg stores don’t )

Or may be due to demonitization they realized that their business model had some huge cracks that could not be fixed even with strong tail winds like demonitization.

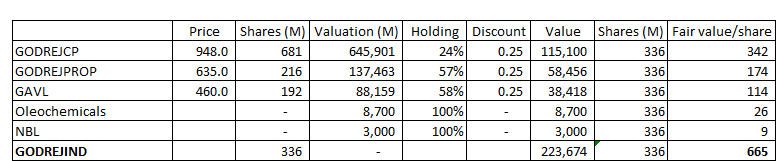

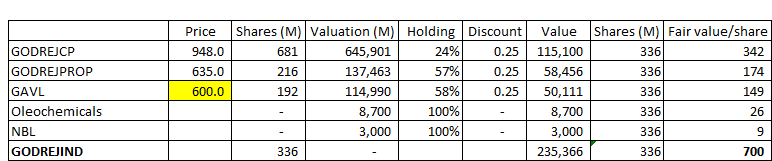

Value unlocking would have been there if Godrej Industries were to demerge and list Godrej Agrovet separately instead of IPO.

But yes, there will be some value unlocking for Godrej Industries as its valuation will be positively impacted by the mkt cap / valuation of Godrej Agrovet. So, not much difference imho for Agrovet as well as for Astec.

They have been buying on multiple occassions in last 1-2 months from open market. Have heard (mind you I say HEARD) that they approached HNI/s holding major chunk to buyout their stake but they didn’t get it.

This buying is obviously positive. I look at it in 2 ways:

They obviously are bullish on long term prospects of the company and hence buying AND/OR

Wondering if they want to merge Astec into Godrej Agrovet (post listing, rather then doing a reverse merger now) and they are listing agrovet for transparent & better price discovery. In case of merger post listing of Agrovet, maybe owning more of Astec would be beneficial for them?

Discl. - Invested since lower levels. Please Note: Always ignore the HEARD part and take it as speculative and rumours.

@hitesh2710…Could I request your comments on below please?

The market cap of Godrej Industries is lesser than the combined market cap of Godrej Properties and Godrej Consumers - the two companies it holds. Is it the usual holding co discount at play?

GI also holds other companies including the formidable Godrej Agrovet (which further has a stake in Astec Life Sciences). These holding amongst other smaller companies like Godrej Nature’s basket is not listed. And these companies dont reflect in the GI market cap.

So, my question. Are we looking a value unlocking whenever Godrej Agrovet is listed? Or the holding company discount will continue?

Disc: Not invested but GI continues to interest me for a complete Agri play. run by an excellent management

Godrej Industries has matured up more as Holding company than stand alone business. It holds interest in different group companies, its own land and hopefully will invest in more startup venture, groom them and list. The listing of Agrovet and subsequently Nature basket will reflect in in its market cap though at a discount. But the business once mature give a substantial value over invested amount. So if they are successful with a bumper valuation in Agrovet which already is reflecting in its market cap. So to answer if its fully valued . On SOTP valuation No if Agrovet is considered to be 4500 crore for their 63.5% holding per market grapevine. Godrej Consumer + Godrej Properties 18000 crore for their holding.But other wise it may look overvalued by all other metrics.

Let me build a scenario here re rise in egg prices. The price spike is majorly due to low production and constrained supply. In order to make the most of price rise, production will be pumped and hence more demand for poultry feed. Godrej Agrovet is a leader in poultry feed. While the prices have been steady off late, it should follow the trend of egg/ chicken price.

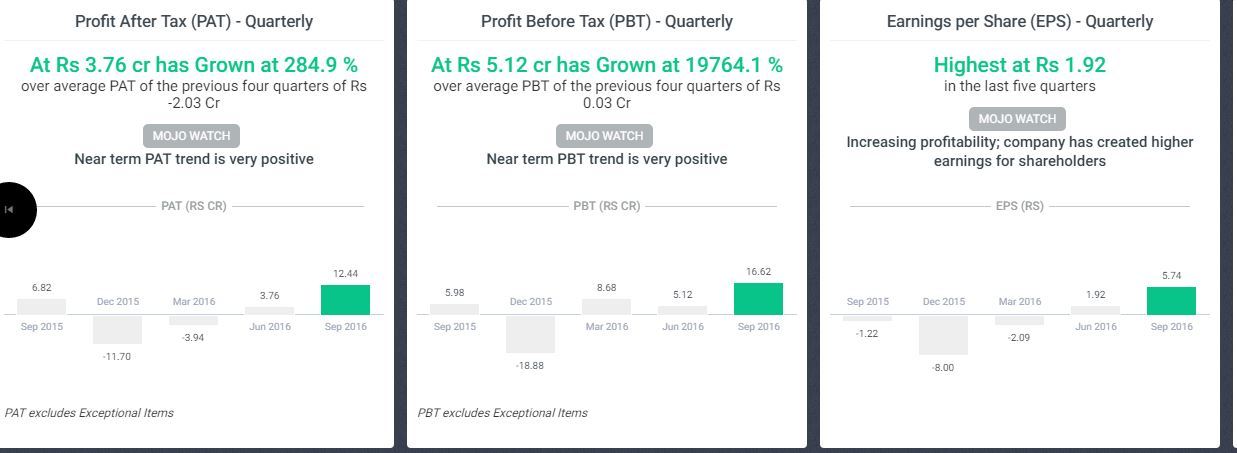

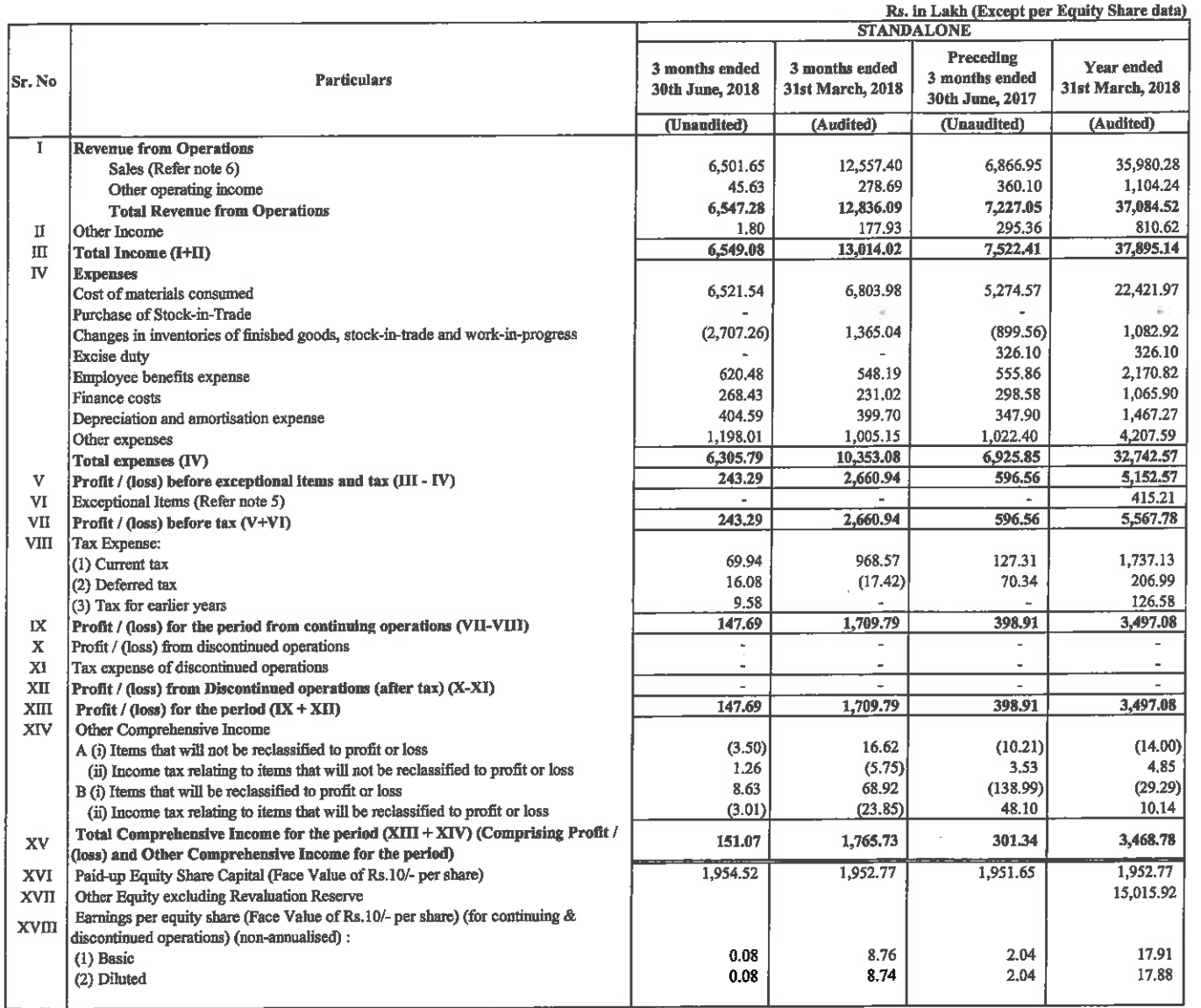

Astec’s quarterly numbers declared yesterday, looked very bad. Could someone please help to understand why there is no consistency in their numbers and variation had been huge even in past as well. One quarter 200-300 % growth and next one halves

[I guess there is a typo in EPS numbers, it should have been 0.8 and not 0.08 … profit/number of shares == 1.47/1.95]

There was an interesting presentation on this in Alhaideas 20-20. There too the presenter had warned against choppiness in quarterly numbers, did he already had some idea about what was coming on 1st Aug.

Choppiness is there as at times there is preponement or postponement of sales in business they are involved in. Here is a snippet of this discussion from agrovet concall…check red highlighted portion.