Thanks for your view Jitenji. One more question,Would you advise in investing in couple of good PSUs in the power/energy sector as a basket? The PSUs seem to be on a strong wicket and are likely to benefit from the cyclical upturn.

@jitenp Jiten bhai, Whats your view on auto ancillaries ? Is it the right time to enter ?

What is view on BOPP films now

The post above says BOPP film cycle is good

Please see the Cosmo Films thread. I have been giving my views on BOPP in that thread.

2 Likes

As mentioned earlier, my view is we should be very careful of valuations we pay in auto ancs. We have had a slowdown in the auto sector. So, few companies are attractive. Have investments in a few.

Also keep an eye on EV threat.

3 Likes

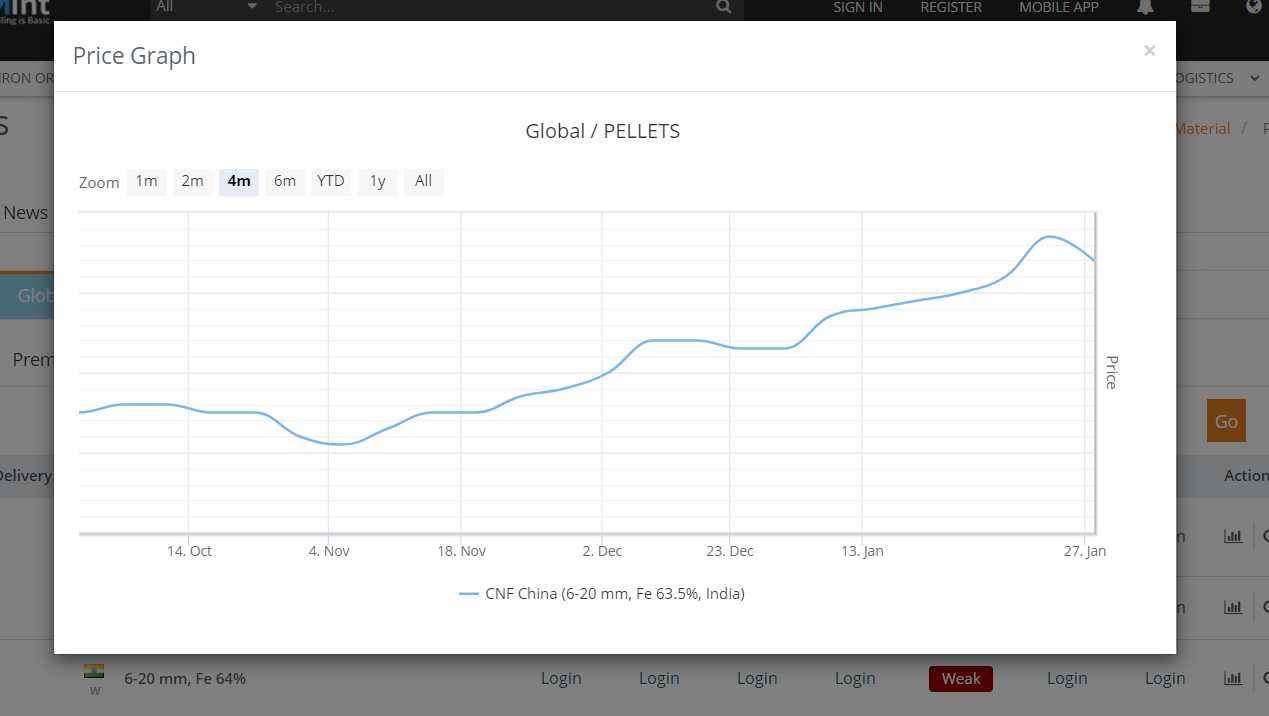

The pellet prices have remained strong and are currently trading close to 4-month high at 120-125$ per tonne. Would love to know your views @jitenp on iron ore pellets sector.

Jiten ji, some auto ancilliaries mfg. axles are trading at reasonable valuations and not dependent on EV factor. Please let me know your views.

yes. am invested in one of them.

1 Like

pellet prices have been strong. but that is not reflected in stock prices of many. That’s why I always say, business cycles and market cycles may not coincide. We do have to see if demand is there or whether it may slow down. Especially Chinese situation may subdue demand, so needs to be seen if prices can sustain.

3 Likes

Cement companies doing well

India’s JK Lakshmi Cement has seen a 251 per cent YoY surge in its net profit to INR493.1m (US$6.92m) in the October-December 2019 period, compared with INR140.5m in the previous year.

Sales rose seven per cent YoY to INR10.05bn from INR9.35bn, while EBITDA advanced 48.5 per cent to INR1.67bn. The improved results were attributed to a reduction in logistic costs and improvements in fuel prices.

During the nine months until December 2019, net sales increased 10.1 per cent YoY to INR29.82bn and EBITDA surged 53.6 per cent to INR4.98bn.

Shree Digvijay Cement has announced an 8.5 per cent increase in total income to INR1.23bn (US$17.2m) for the 3QFY19-20, compared with INR1.13bn in the year-ago period. Net profit also advanced to INR94.4m from an INR3.6m loss in the year-ago period.

In the nine months ending December 2019, income rose 4.2 per cent YoY to INR3.43bn and net profit surged 671.7 per cent to INR332.6m.

UltraTech Cement has announced that the Phase I commissioning of its 2Mta grinding unit in Bara, Uttar Pradesh, India. Once fully commissioned, the total capacity of this unit will be 4 Mta.

2 Likes

Baba Kalyani view

1 Like

Anyone here tracking Ferro-Chrome as a commodity? Interesting set of events going on in the industry- domestically and globally as well

-

Low realisations: Global FeCr prices hit the lowest range within past 10 years around August’19, lower than 2016 when there was a steep correction in the realisations. Low prices are due to low realisations in Stainless Steel manufacturing- application of FeCr

-

Industry was dominated until now by South African Cos like Glencore, Samancor etc. with highest capacities and lowest cost of production due to chrome ore availability. However, structural power tariff hikes by Eskom has resulted in much higher power cost and amidst bottom prices of FeCr, even globally largest players are facing challenges in operations and are no more lowest-cost producers

-

Production Cuts: Many global giants like Glencor, Samancor, Merafe have announced production cuts over past 1 month because it’s unviable to operate at current prices. This is likely to tighten the supply and lead to higher FeCr prices eventually

-

Domestic Scenario: Facor alloy and Rohit Ferro-alloys are going through liquidation; Balasore alloys is suffering from financial stress as per online available reports.

IMFA stands as the survivor among the consolidation of domestic peers as it is financially stable and only fully integrated domestic FeCr producer. Any upticks in FeCr prices will help IMFA’s financials substantially due to high operating leverage

17 Likes

There is a midcap company known as NB ventures which is into sugar production, ferro alloys and has its own captive power plant.csn a senior boarder advise the impact of the above on the company which will obviously be based on our steel production.

Disc: invested for a v long period

1 Like

I feel investing tactically in NB ventures for FeCr cycle revival is not appropriate because:

- It produces other Ferro-Alloys like silico-manganese, Ferro manganese etc. and not only FeCr

- It is not integrated peer as it has doesn’t have captive Chrome ore mines which is the core RM for FeCr

2 Likes

Chemical sector which does not import raw materials from China could be benefitted. Prices might be increased. @jitenp your views on the above. Any chemical stocks you are tracking

3 Likes

Many companies will be affected in the chemical sector for short term. Few who do not have RM dependencies will benefit. In medium and long term, whole sector should benefit. We should be alert to buy something where short term disruption but long term benefit kind of scenario looks plausible.

7 Likes

Hikal LTD has already given heads up on short term disruption in q3 press release

1 Like

@hitesh2710 ji @jitenp ji, In relation to the auto cycle,what are your thoughts on Fiem industries vs varroc or minda?It is a smaller player and relatively undervalued compared to others.It does not face any EV threat(a part of Endurance faces EV threat).As the cycle turns would it not be a source of higher returns compared to other players like minda or varroc?

Or is its relative undervaluation justified due to the overhang of LED division?

3 Likes

Seeing early signs of cycle reversal in the power sector.

a. The power demand grew 3.7% in January after 5 months of decline.

b. The sector is witnessing consolidation as players with healthy balance sheets are lapping up distressed ones (like JSW Energy buying GMR’s Kamalanga Energy)

c. Also GOI’s continuous selling of stocks of companies like NTPC through CPSE ETF is coming to an end and the absence of excessive supply should firm up stock prices.(This has ensured that Jitenji’s mantra of buying at high PE for a cyclical sector does not apply in this case)

d. Power is in some sense a surrogate for consumption & economic recovery

e. Promoters are closely evaluating viability & days of obscene bids are over.

However as Jitenji pointed out, Discoms continued to be a factor of worry. Also, I think the other risk is that power is slowly becoming a ‘good political freebie’ (used by AAP in Delhi elections)

3 Likes

Interesting analysis.

The OPMs of IMFA is likely to be in single digits in this year, which is the lowest in last 10 years. Do you have any visibility about consolidation in the sector, say IMFA buying Facor Alloys or Rohit Ferro-Alloys ?

There was some news of IMFA’s interest in buying Facor’s manufacturing unit of 60,000 tpa and not the mines.

1 Like