hi Jiten,

Any idea on Cement industry ? I guess they are in the upcycle now.

hi Jiten,

Any idea on Cement industry ? I guess they are in the upcycle now.

Iron ore prices surge:Any further rise would impact Steel margin: Industry

Global steel output jumps in H1

http://epaper.business-standard.com/bsepaper/svww_zoomart.php?Artname=MjAxODA3MjdhXzAxMzEwMTAwOA==&ileft=573&itop=1264&zoomRatio=162&AN=MjAxODA3MjdhXzAxMzEwMTAwOA==

Hello friends.

Found good blogs to track latest developments in ferrochrome industry in China and all over the world. I found it very helpful to understand basics behind price change of iron ore.

Hope you would love it.

Hello friends.in cyclical investing does management and balance sheet matters?

It matter in all investment - cyclicals, secular, special sits etc.

For cyclical e.g if balance sheet is not good than even a good management can’t take much advantage e.g. Tata steel

If managment is not good then cyclical may not see good return e.g. KMB and his focus on growth instead of quality of earning in aluminium etc.

Is anyone tracking ferroalloys.promoter holding is good.balancsheet is also good.stock at all time low.pe of 1 price to book of .30 .price to sales0.20.is there any problem related to management?or cyclical low price?

Hi friends,

Some developments on my side. Our firm is now a SEBI-Registered Investment Advisory firm. Will be constrained on talking of any buy/sell/hold on any stocks. Will try to contribute (time permitting) on sectors, and to an extent on companies, without giving any advice.

have joined your advisory, waiting for some amazing research reports from your side.

All the best Jiten Sir.

Sir, being an expert in cyclical commodity stocks i have a doubt to ask you.

In my childhood days we used to buy unbranded salt, but now we are buying branded one. ie now salt has been become an FMCG item rather than a commodity. But still we are buying unbranded sugar. Recently when I went to the local supermaket owned by my cousin, I found one rack fully loaded with branded sugar. I enquired about it with him and he said that there is a very good responce for it. Our town is a small C class town in Kerala which consists of 99.9% middle and lower middle class people. (I am not specifying the brand as you have started advisory firm and it will be difficult for you to comment on a particular stock.) I feel a shift is happening in the behavior of consumers. I cant understand that if we are ready to buy branded salt, why should we not buying branded sugar.(Not forgetting that branded salt got the biggest push from the iodized salt drive for the fight against goiter from various health organizations and the govt

So I feel if there is going to be a change in customer preference from unbranded sugar to branded one, the sugar sector will become an FMCG segment rather than a commodity one and market may assign FMCG valuations for the sector rather than a commodity valuation

Pls share your views. Thanks in advance

I think it will take quiet a long time for this to happen.

VEDANTA - Q1 FY19 (Cons)

Net Revenue at 22,206 Cr

18,285 Cr (21.4%) YoY | 27,630 Cr (-19.6%) QoQ

Net Profit of 1,533 Cr

1,501 Cr (2.1%) YoY | 4,802* Cr (-68.1%) QoQ

EPS (in Rs.) 4.13

4.04 YoY | 12.95 QoQ

*Distribution Tax credit

Good war chest of cash and liquid equivalent of 35k crores. Nos on face of it looks above average…copper sale is down, need to see mgmt commentary…

Cabinet Approves

Reducing Stake In Hind Copper To 66.13% From 76.05% Earlier.

Hind Copper to Invest ₹5,500 cr for Expansion

Rakhi.Mazumdar@timesgroup.com

Kolkata:

Hindustan Copper (HCL), the country’s only integrated copper producer, on Thursday said it will utilise funds from issue of fresh equity shares to expand mine capacity nearly six times. This will be part of the company’s plan to spend ₹5,500 crore over the next six years on expansion.

A day earlier, the Cabinet had given its approval for issue of fresh equity shares amounting to 15% of equity capital in HCL, which is tipped to raise ₹900-1,000 crore through qualified institutional placement (QIP). In the absence of budgetary support for the expansion plan, the fund raising plans, which will be a mix of equity, internal accruals and debt, are critical for HCL to achieve its production target of about 190,000 tonnes of metal-in-concentrate. Internal accruals are likely to be about ₹300-500 crore per year within the span of six years.

The company said capital expenditure plan for mine expansion along with a further investment of ₹175 crore on exploration activities spread over three years will increase availability of copper and enable HCL to meet 30% of the country’s demand for copper, up from 4% now.

This will also help reduce the country’s dependence on imports to the extent of 25% of copper mineral.

World’s biggest miners want more copper, but nobody’s selling

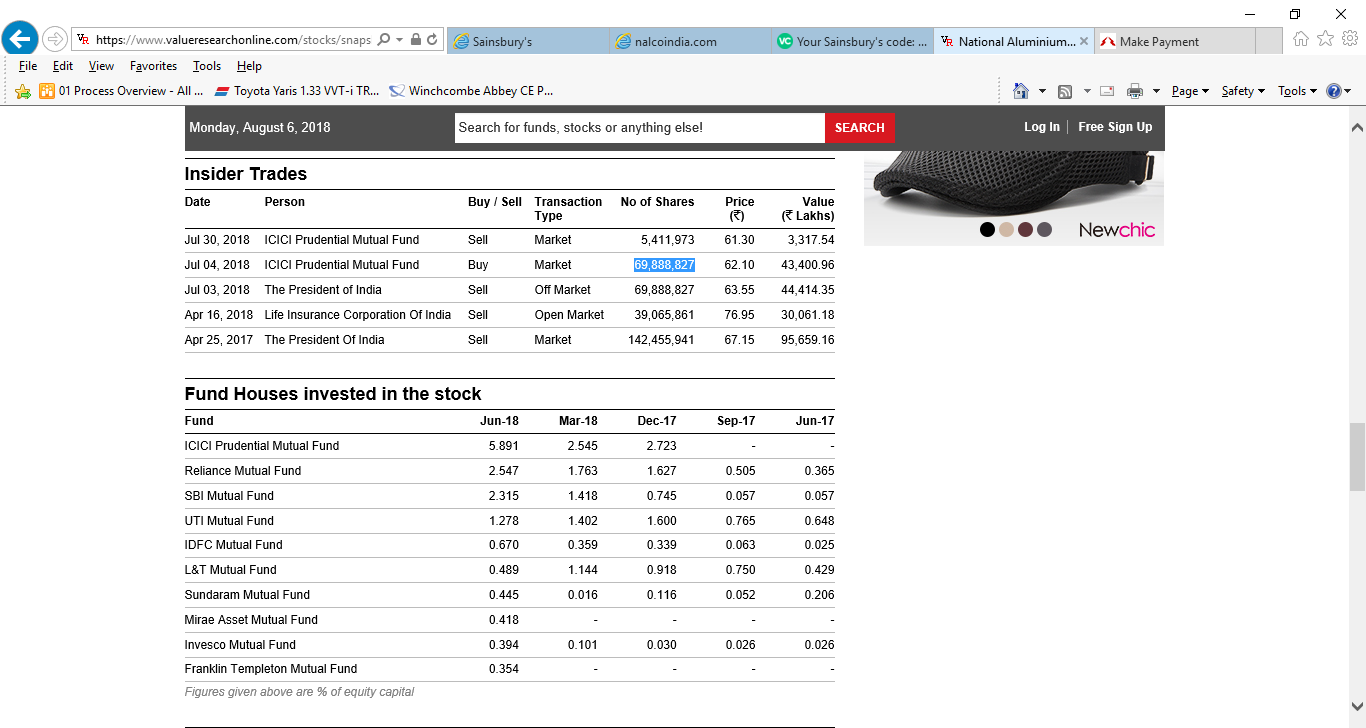

Just checked the Mutual Fund holding and Insider trading report for Nalco from Value Research.

Disc- Invested

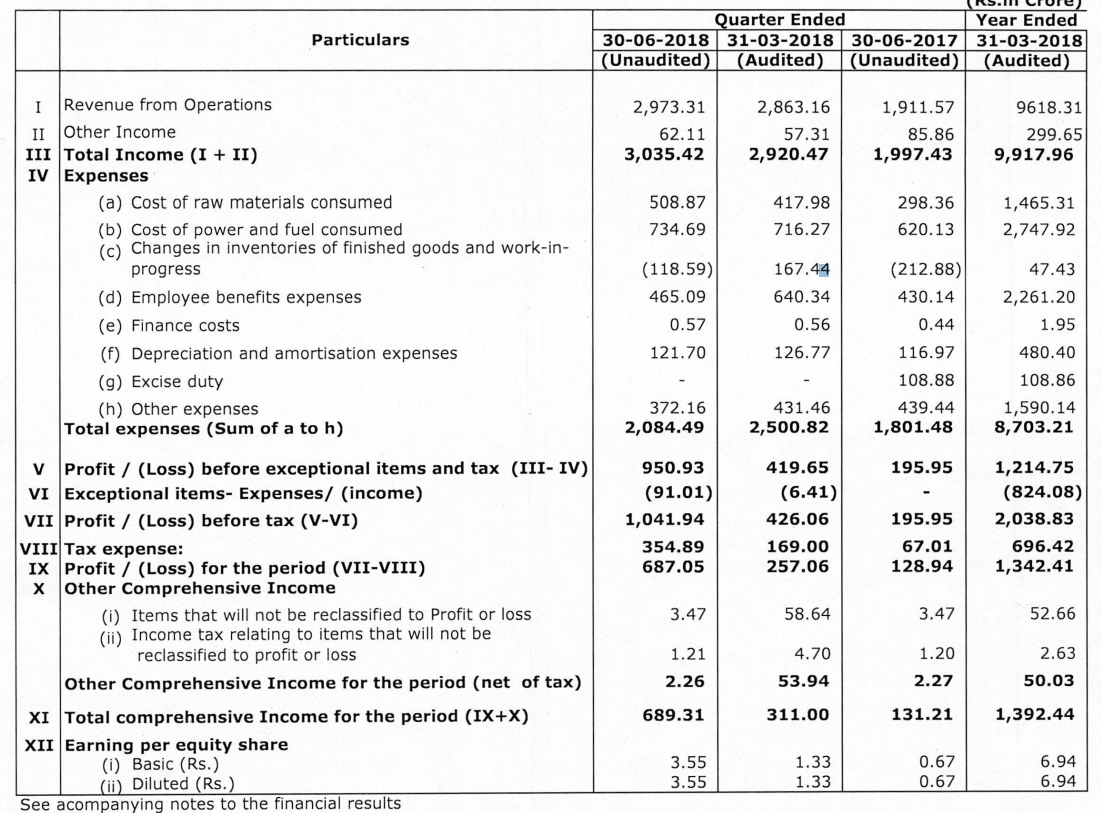

Nalco has posted very good numbers. Revenues up 55% and PAT up 425% on the back of great margins on Alumina exports.

Disc: Invested

Are these results one-off due to short term effect of higher alumina prices due to Rusal sanctions by US?

Do you these kind of results are possible into future? What are you estimates for FY19?

Thanks

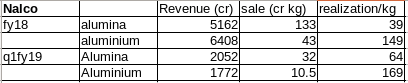

According to q1fy19 results and press release. Alumina realization per kilogram for Nalco is Rs. 64 compared to Rs. 39 for fy18.

This is close to $927/ton, compare this to average Alumina price on Shanghai Metals Market today’s rate of 2960 Rmb/mt which converts to $435/mt. Quite a difference.

Am I doing some mistake in calculation?

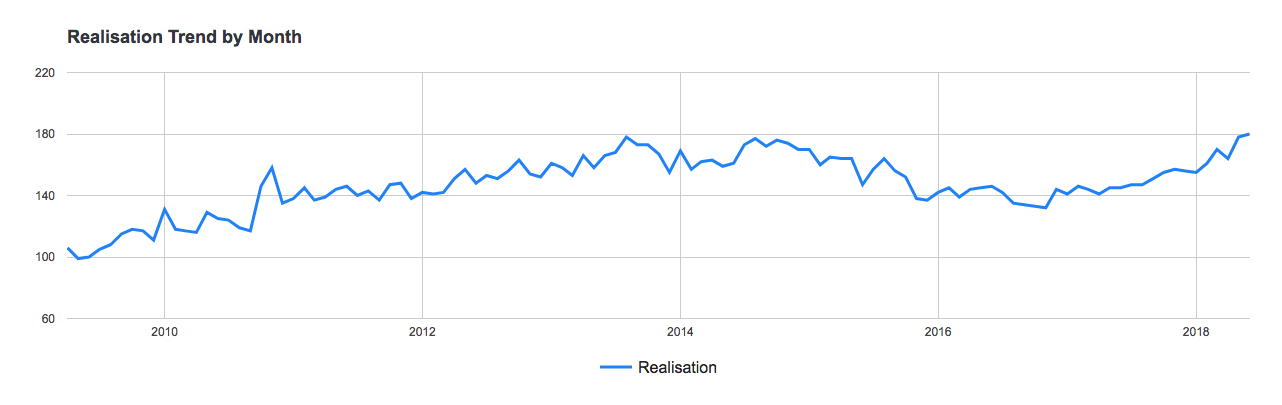

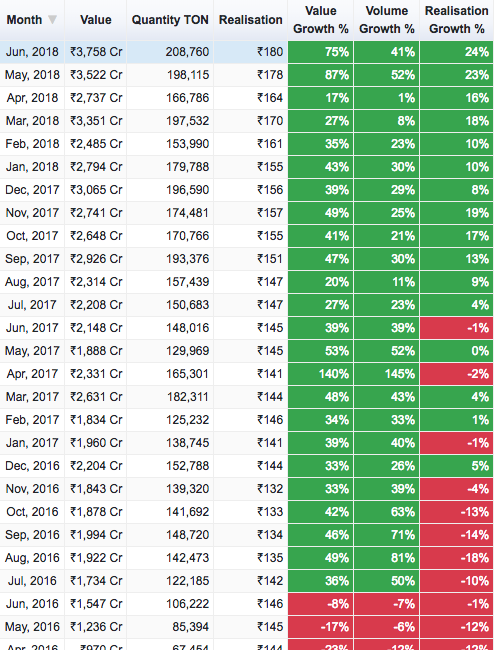

As per exports data for “Aluminium and products of aluminium” (I assume alumina exports would be part of this), May and June saw realisations of Rs.178 and Rs.180/kg respectively.

Realisations should come down in the coming months as the prices have softened since. The thing is, during May and June, Nalco must have made the most of the prices, as the volumes as well were at an all time high

See the volume growth of 41% and 52% in May and June when realisation growth was around 24%. Lets see how the July numbers look. It should come in 10 days time.