COHANCE LIFE SCIENCES

CMP : Rs 371 | Mkt Cap : 14200 Cr | P/E : 42 | ROCE : 14.9

About the Company :

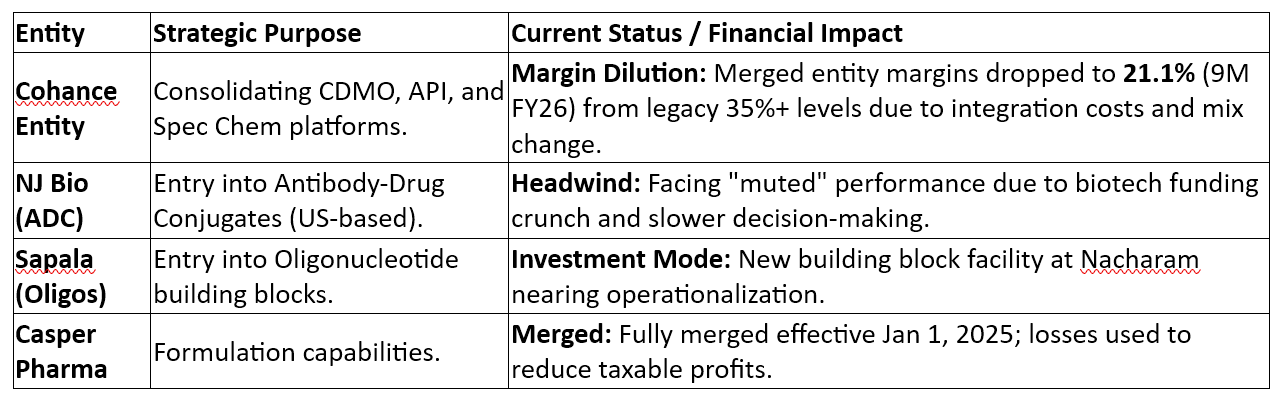

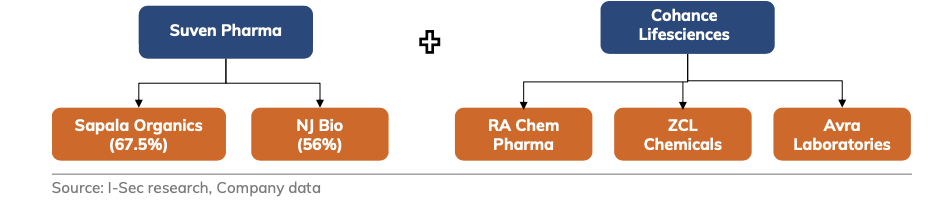

- Merged entity of erstwhile SuvenPharma and Cohance to form Cohance Life Sciences. This combined entity in itself is a sort of platform created by Advent combining : Sapala (67.5%), NJ Bio (56%), RA chem, ZCL chem and AVRA Labs .

- Post merger share holders of Cohance received 11 shares of merged entity for every 295 shares of Cohance. Advent post merger holds 66.7% shares.

- Erstwhile Cohance through AVRA labs was the first company to to develop a synthetic route to Camptothecin based payload platform for ADC.

- Separately Suven acquired NJ bio (based in Princeton, NJ founded by Dr. Naresh Jain). NJ bio has extensive expertise in linker and bioconjugation technologies . This complements Cohance’s capabilities in payload chemistry and CGMP manufacturing facilities in India.

- Suven through Sapala organics has also forayed into Oligonucleotides . It is among the few CDMO to supply complex building blocks of Oligo nucleotides.

- Post acquisition Advent has been pivoting from slow growth but higher TAM small molecule market to higher growth ADC (TAM of 10bn $, CAGR of c. 35%) and oligonucleotides (TAM of 4.6 bn , 20%+ CAGR over FY25-FY30)

- Advent bought 50.1% stake in Suven initially for Rs 495/share for Rs 6330 Cr valuing Suven at around Rs 12600 cr. Juxtapose this with current price and market cap of roughly Rs 14200 cr for the combined entity !!

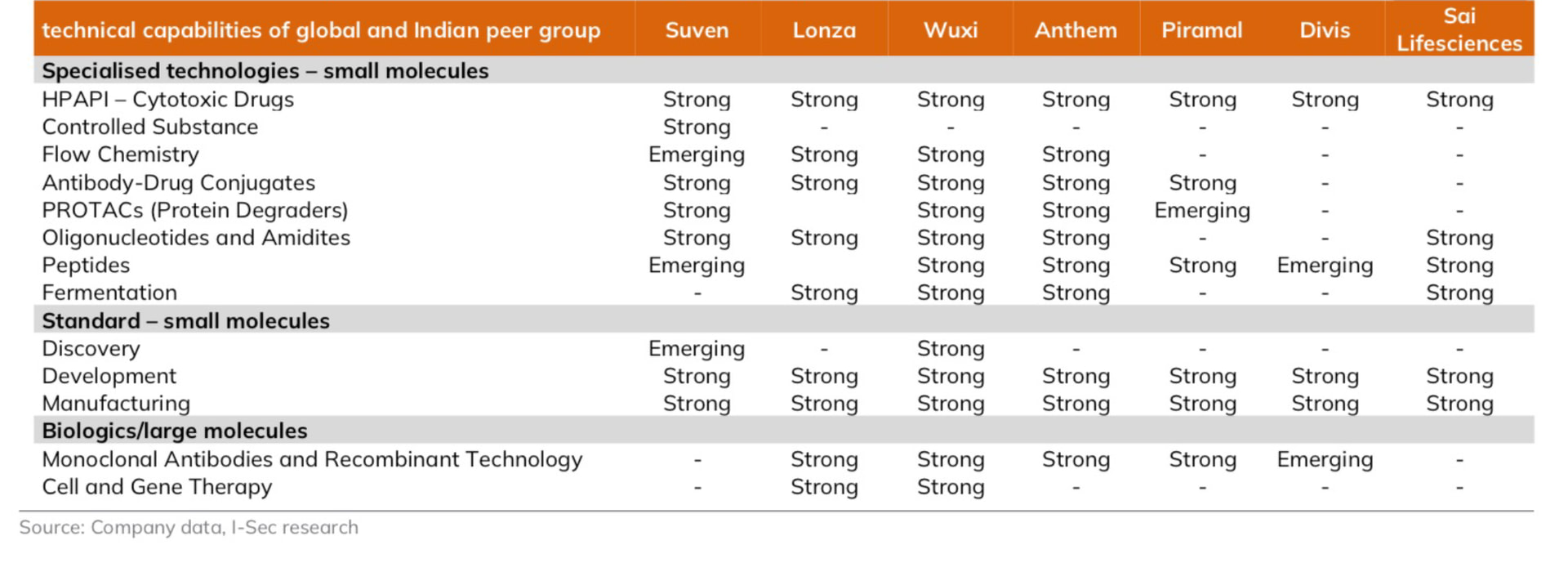

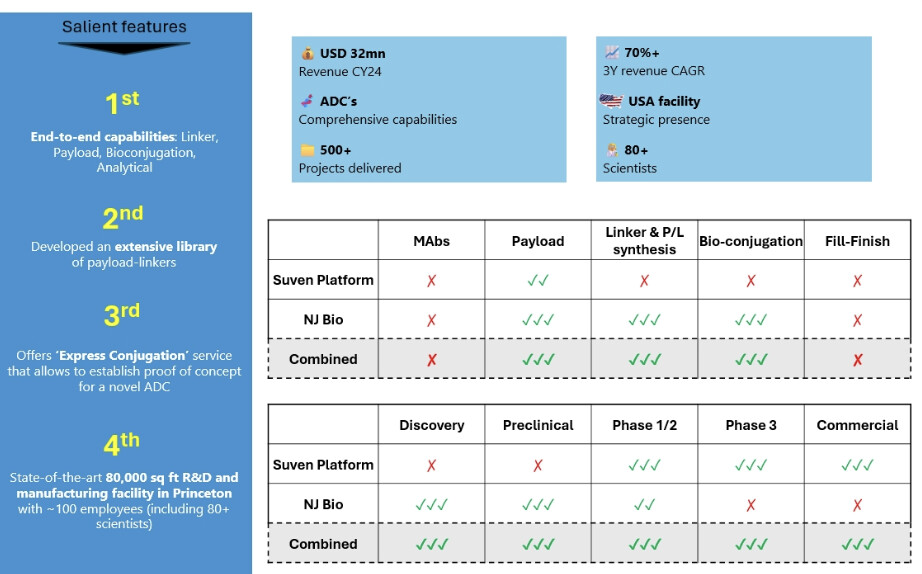

- Above mentioned is their capability matrix vis-a-vis Indian and international peers. I guess the peer 2 with similar capabilities in India should be Piramal Pharma (They also have capabilities in MAb which Cohance doesn’t have). Anthem bio seems to have capabilities across the value chain including MAbs .

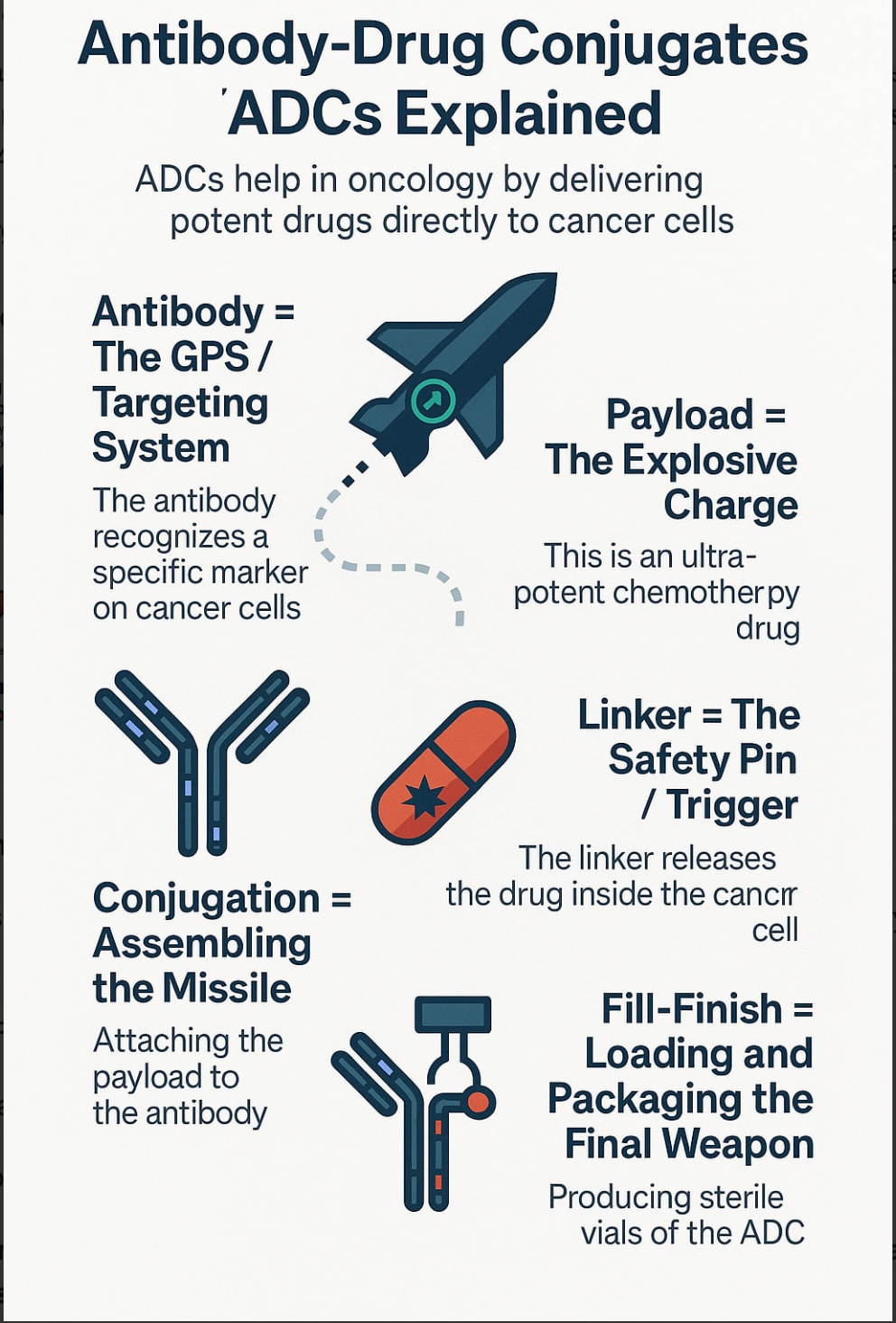

- The ADC therapy is like a guided missile . Cohance has built capabilities in the Payload (through AVRA) , Linker Synthesis and Bio Conjugation (through NJ bio) . Missing piece is Antibody (large molecule | biologics ) and fill finish.

-

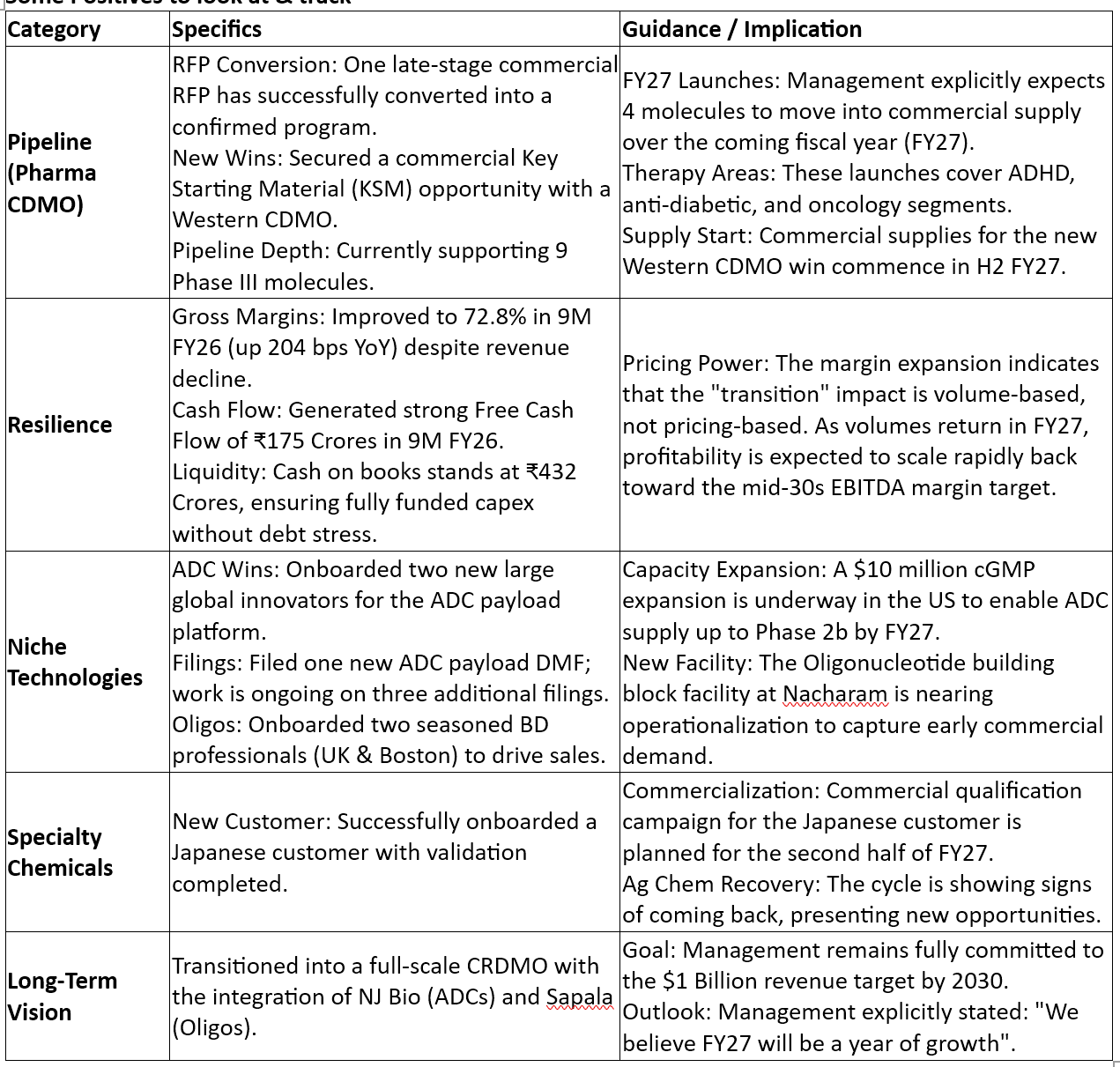

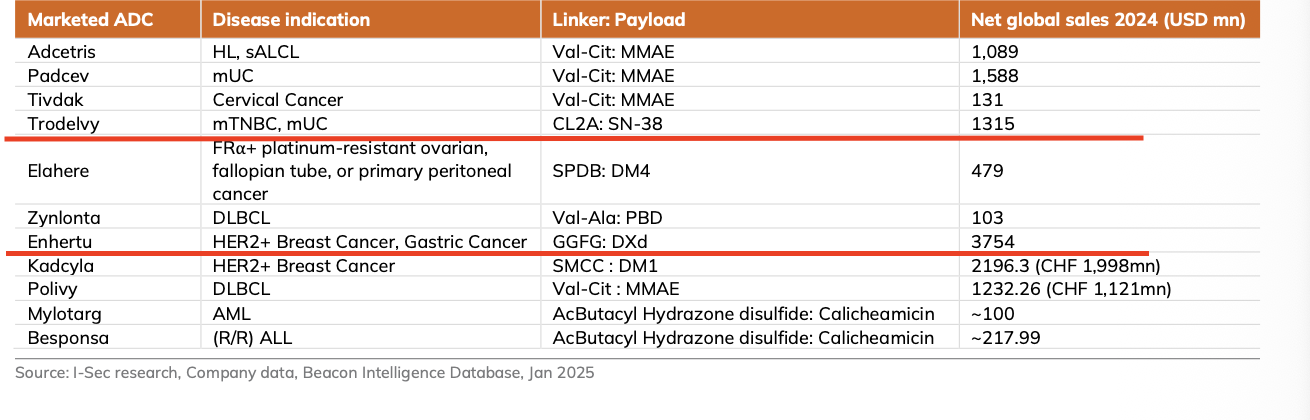

Cohance has an extensive payload library with 500+ payload-linker construct. They have global leadership in Camptothecin payload . Camptothecin payloads for 2 commercial ADCs are supplied by Cohance (Enhertu : Transtuzumab Deruxtecan | Daichi/Astra Zeneca | Payload : Dxd ) and (Trodelvy : Sacituzumab Govitecan | Gilead | Payload : SN-38) . They have plans to launch 3 more payloads in FY 26-27.

-

Cohance supplies a key intermediate S-trione for Dxd . Enhertu sales is expected to be 11.2 bn$ in FY 30 .

-

Below picture depicts the capabilities of combines Cohance Platform and presence across the new drug pipeline.

-

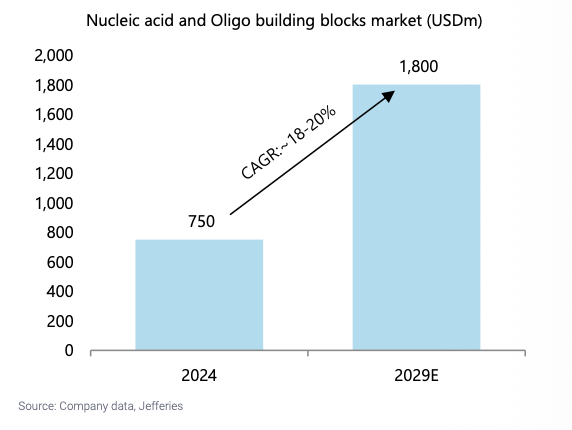

Suven acquired Sapala founded by P. Yella Reddy who spent 20 years as director (R&D) with Toyota chemicals . Sapala has capabilities in Oligonucleotides , mRNA , Nucleic acid etc. It had a revenue of 670mn Rs in FY 24 with EBITDA mn of 41%. It is engaged in cutting edge therapies like : GAINAc - N-Acetyl Glactosamine ligands , Modified Amidities - Basic building block of Oligo Nucleotides , Tricyclo DNA - Nucleic acid Analog , Locked and Bridged Nucleic Acid- LNA /BNA , FANA - 2’- Fluoro Arabino Nucleic Acid. The TAM for Sapala is expected to grow at c. 18-20% over the next 5 yrs.

-

While ADCs recognizes proteins on cell surfaces as a lock and key , Oligonucleotides attack disease at an instruction level (DNA/RNA).

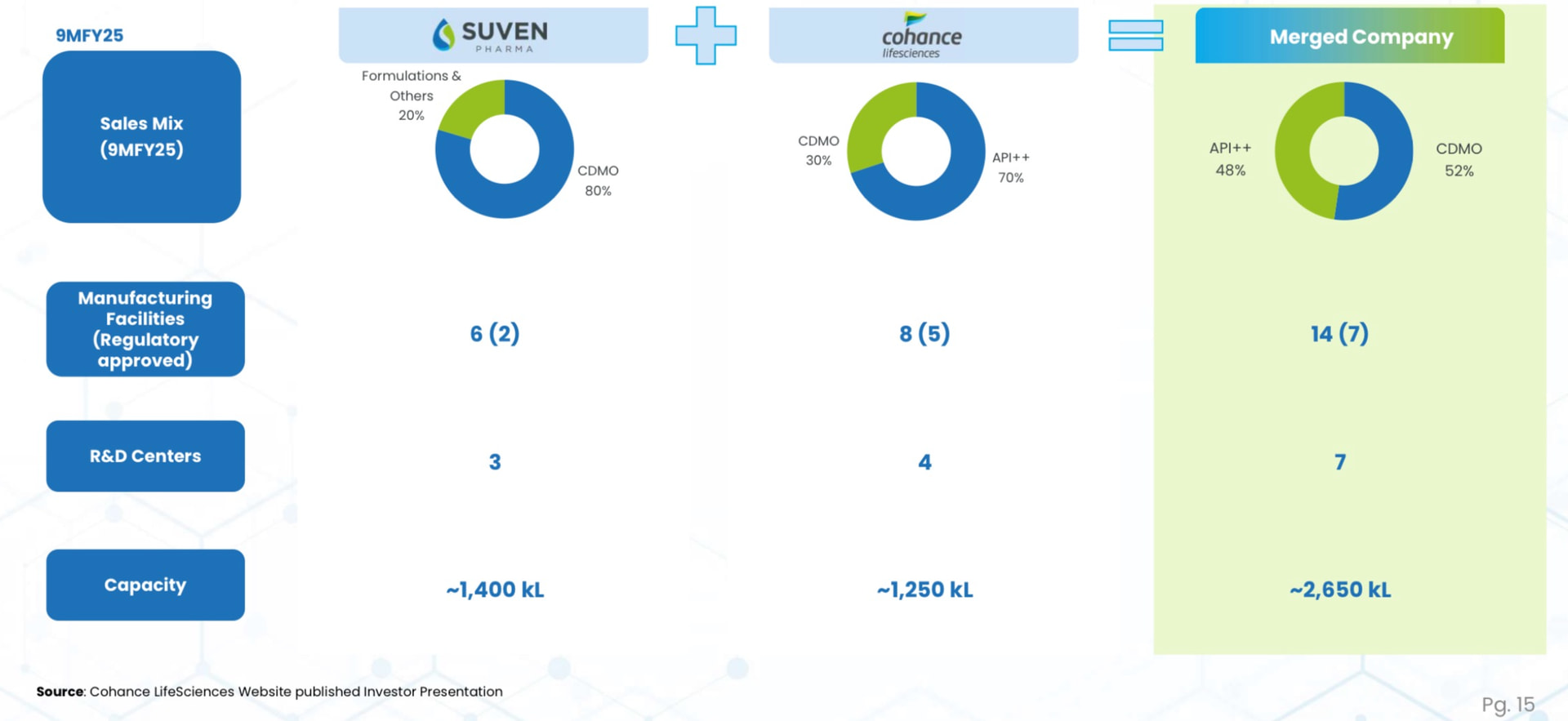

Merged Entity Revenue Dynamics

Erstwhile Suven was CDMO heavy while Cohance was API++ . The merged entity is equally weighted between CDMO and API.

- ADC therapies including Enhertu and Trodelvy (Payload supplied by Cohance) has an expected TAM of 10.4 bn$ growing at a CAGR of 26.9 % .

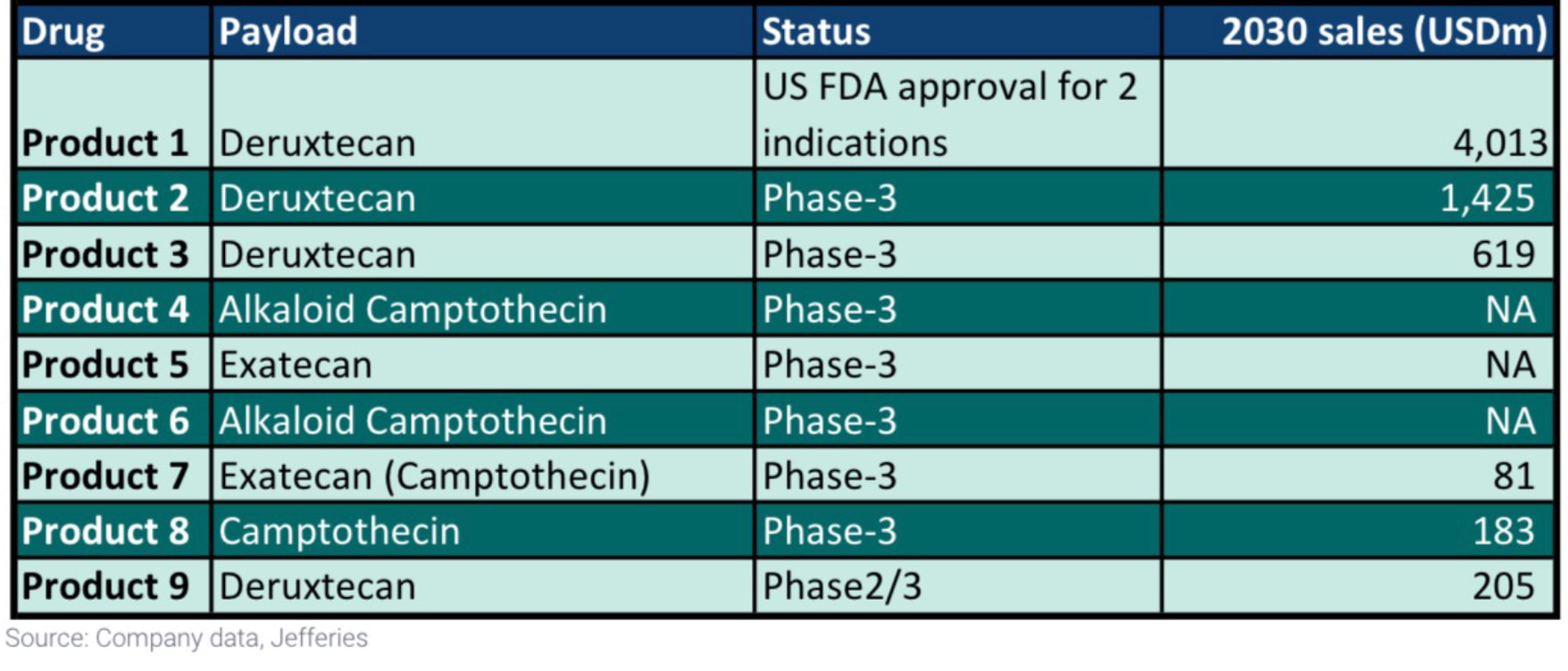

Below are the key pipeline ADC drugs where Cohance is a payload supplier :

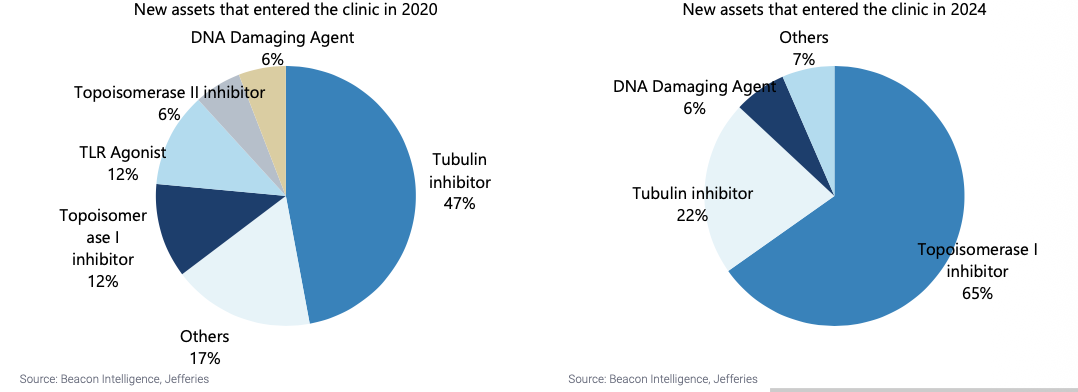

- Cohance has leadership in being the exclusive supplier for CPT based payload (Topomeraise I inhibitor) which has shown superiority v/s Tubulin inhibitors and DNA damaging agents . Currently Tubulin inhibitors have 12% failure rate, DNA damaging agents have 15% failure rate while Topomerase inhibitors have just .4% failure rate . This is leading to higher adoption of CPT based payloads

Notes from Concalls and other forward looking statements :

-

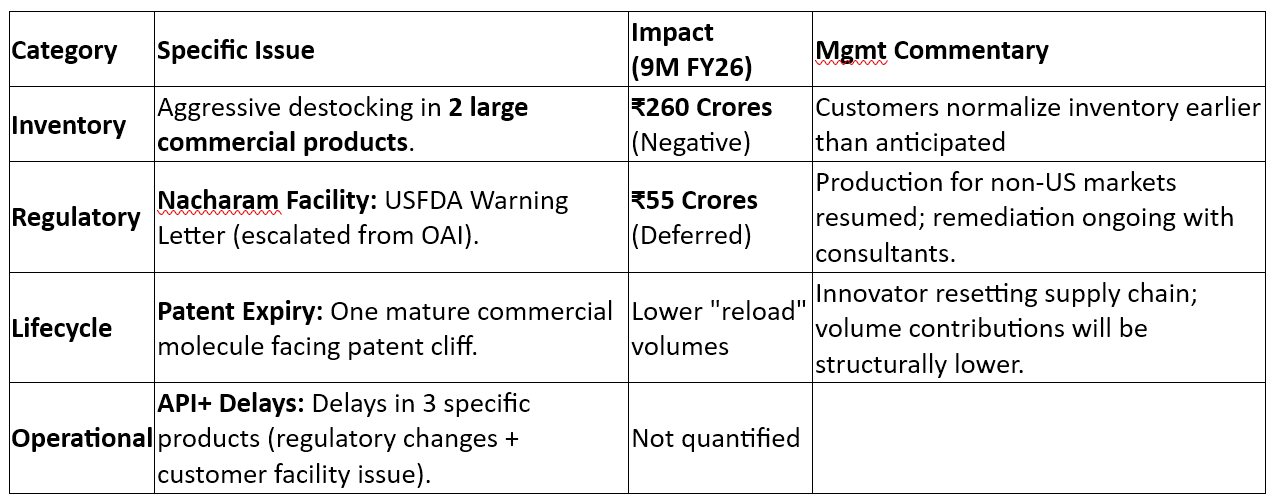

Cohance relies on innovators and big Pharma for their procurement schedule of Sales. There was a destocking cycle going on post covid and it is expected to normalize by H2 FY 26.

-

There was a sort of funding winter for the US biotechs which has seen signs of revival from October , November of 2026. Nandini Piramal also alluded to the same in her concall.

-

The market was spooked by the multiple events of resignation of CEO Mr. Raju , FDA observations at the Nacharam plant , revenue drop and big drop in EBITDA margins.

-

The market seems to be over reacting to temporary blip due to the merger. Since the merger of 2 large entities take shape (Which in itself is a combination of several big entities in their own right), it normally takes time to settle down and for the synergies to take effect.

-

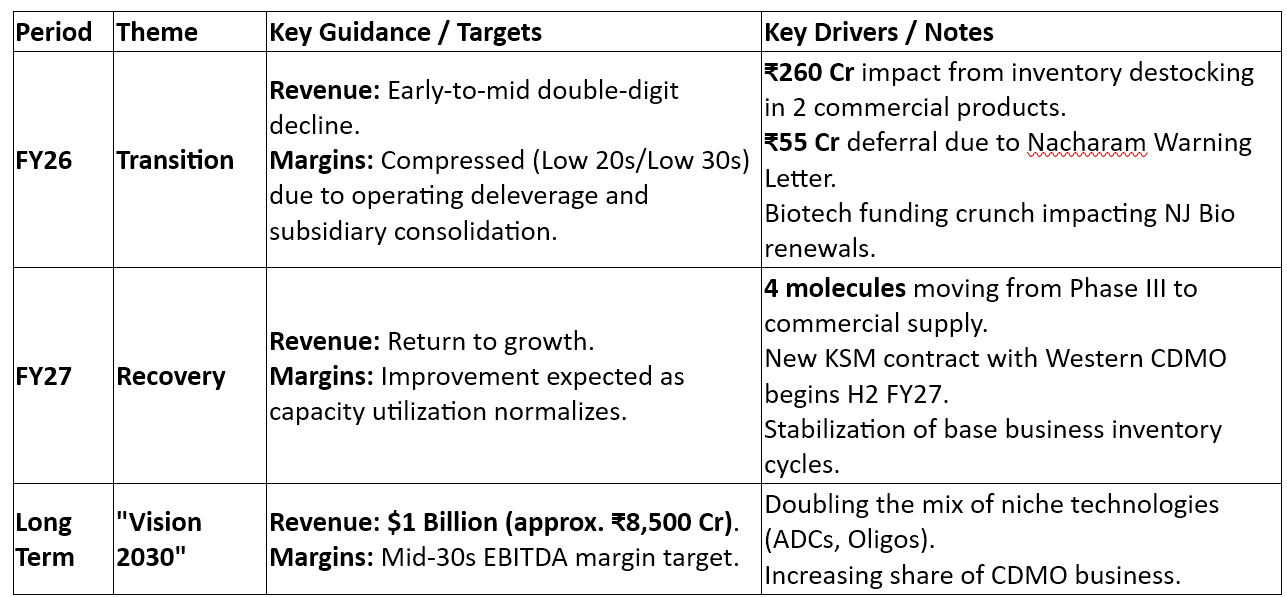

The management has reiterated the vision of clocking 1 bn $ revenue by FY 29 (Current revenue is C. Rs 2500 cr v/s FY 29 plan of Rs 8500 cr). If anything remotely close to that happens then the revenue has to grow at a CAGR of 26-30% .

-

The management has guided for flat revenues with higher margins for FY 26. For that to happen H2 FY 26 has to be significantly better than H1 FY 26.

-

There are 15 ADC drugs already approved and 16th is underway. Most of the ADCs are used in Oncology . Current ADC market is 14bn $ slated to grow to 65 bn $ . Out of the current market Cohance supplies to drugs worth 5 bn $ . Since the market is expanding and share of Camptothecin based payloads are expanding compared to Tubulin inhibitors the TAM for Cohance in ADC payloads should improve much further.

Key Risks :

-

Cohance is a merger of 6 different companies and it might take time for the merger synergies to play out. Without a coherent strategy and result driven management this can go haywire. In silos people like AV Rama Rao of AVRA, Dr. Naresh Jain of NJ bio and Dr. P Yella Reddy of Sapala are pioneers and stalwarts of the industry.

-

Slow adoption of ADC and Nucleotides and rising competition on ADC segment can be a damper.

-

Cohance not having MAb capabilities significantly reduces the TAM as well as target audience like biotechs who would want a single point of contact .

Suven was always known for their industry leading margins which seems to have gone southwards post merger . Cohance bets on high growth ADC and Oligo nucleotides to shore up margins to atleast 35 % from current low of 20-22%.

In Conclusion I believe the pain to ease in next couple of quarters and the current levels are very comfortable in terms of valuation. If things don’t go haywire from here this can be a good entry point to accumulate the stock with a 3-4 yr perspective.

Disclosure : No positions yet in personal portfolio. Actively considering though.

I am not qualified to give an opinion and has been wrong most of the times in the past.

The information is sourced from the AR, brokerage reports from ICICI direct , Jeffries ,Company presentations.