As far as I understand their holdings include ITC, Nestle, Asian paints, Berger, Dr Lal, Page (largest holding), Pidilite and Bajaj Finance.

They have just built the portfolio as per my understanding so their buy prices should be close to cmp.

Page has corrected by 10+% from their avg buy as per their latest Q4 video on their website. I dont know if ITC was held in their previous portfolio in Ambit or in their personal portfolios. But blindly cloning their portfolio, let alone their’s cloning any portfolio without a thesis & conviction may not be the best idea. I do not know what they hold/what they add/when they buy as I dont have a PMS with them. I simply keep up with their material on their website.

There are not many companies that fit into this criteria I think!

I have no idea on that. I understand that Mr. Mukherjea likes the company.

I think one should not expect more than 14-17% compounding from such coffee can ideas for a long period of time. I do not completely agree with the argument that they will return 20-25% cagr over a long period of time, especially from the valuations that they are at (Nestle, Page inds, Asian paints etc:)

However they are experts and among the best in their field. If what they say works out (and they have backed their process with client capital and their own) then one could outperform by quite a bit in the long run!

I too like the coffee can concept and May be nestle and page may has shown some growth but Asian paints isnt growing more than 10% CAGR since many years .

When I look at these paint companies I make the following observations:

The market opportunity is quite big. India has a lot of infra and housing development that is yet to come as the country moves towards a developed country status.

This not only increases the “new development market” it also adds to the “base” replacement market. As the base increases so does the replacement demand. So this results in a substantial and sustainable increase in business for the industry.

They face very low disruption & rate of change. Cos like Asian paints are among the forefront with regards to innovation in the industry gloabally even. They all command good pricing power as well.

It is basically an oligopolistic market.

It is not like the FMCG space where new brands can come in and take market share. Where distribution moat can be diluted due to newer ways of doing business. In this case control of distribution is a big moat and a moat that will only expand over time. Nobody buys paints online haha!

These businesses are capital intensive compared to FMCG cos. So we have a business that generates a very high ROCE and at the same time invests a respectable amount in incremental capital. So they will have a decent ROIIC as well.

Asian paints actually had a rough patch due to very low crude prices in between. So they did actually take a price cut is what I understand. ( ive not studied the company much)

Earnings for them may cagr at around 11-15% excluding dividend returns. They also have a long runway and substantial visibility. So over the long run your returns should mimic their earnings cagr plus your dividends.

To read the story of asian paints one can read unusual billionaires by Mr. Mukherjea.

I would love to own both the paint companies (berger and asian) but I’m not comfortable with the price. I think buying them over a period of time at market abberations makes sense.

Paint companies dynamics what has changed over years

Life of paint has increased : Earlier exterior paint used to last for 1-3 years - now life can extend up to 15 years . In Interior paints the life has extended from 3-5 years to 5 - 10 years .

Paints are less dependent on Oil - Earlier oil based paint enamels used to be popular , now the major paints are water based and hence oil prices ideally has less impact on paint prices

Paint are basically low tech products can be easily disrupted by substitutes like wall paper , stone , tiles , glass & other alternative finishes .

Paints have better ROCE because of industry structure esp inability of consumer to effectively compare prices, paints still account for smaller proportion of interior expenses vis a vis benefits and lower economic scale of substitutes . This can change with growth of online distribution & service options for substitutes .

Growth rates in paint per say has fallen so even a company like asian paints has expanded to adhesives , water proofing , modular kitchen etc where it does not have good market shares . These products also have entrenched players like Pidilite and distribution dynamics are also different .

The Life of paint has increased but that will not be an issue as the base also increases. India has a long way to go on infra, industries & housing. So this may not be much of an issue at least in the forseeable future.

This is positive as you have rightly stated.

Yes being low tech is another positive. However, a coat of primer/paint is still applied before applying a wallpaper. Stone tiles to replace walls with paint is a very expensive proposition to make it aesthetically pleasing. Otherwise you have to leave brick walls with some touch up to make it look aesthitically acceptable. Alternatives like concrete, marble, wood etc are again expensive propositions.

This is true and another positive.

Online retail of paints may never take off due to various reasons. Customers do not shop for paints online. They ask their contractor to do so.

Builders/contractors approach distributors directly to get better prices etc:

It is not easy to package a can of paint as it could spill during the logistics process thus spoiling other products in the same space.

Paints as a product really have no reason to be online and customers really have no reason to look for deals on paints as they dont buy them as frequently as say a book and hence ecommerce companies wont have any reason to stock paints or even go through the logistical process to ship paints. Further in many cases a contractor may actually have spare/left over paint in which case the customer will pay as per the contractors charges on the paint rather than buy a fresh can and have the rest sitting idle once the work is done.

(Hypothetically speaking even if a customer decided to buy paint online, if they had an akzo nobel product at 10-15% cheaper than an asian paints or a berger they will most likely pay up and buy a berger or an asian paints).

Paints are an FMIG branded product with an oligopolistic market. Asian paints are a virtual monopoly, I have heard that they dont allow their big distributors to stock other brands. And distributors happily oblige because asian paints sells far better than the rest. This is similar to the pidilite and loctite (Distributed by asian paints) story. (This is what I heard so make of it what you will)

Yes this is something that should also reflect in the valuations but that doesnt seem to ever happen haha!

@1.5cr , great description of the paints industry. Just one thing , since Asian paints is doing so well with such a great market share , why does Berger paints find a place in coffee can portfolio . How does it compare with Asian paints ? What is its USP ? Can it hold its own against Asian paints ?

2 Does Pidilite have a distribution network as strong as the paints industry ? The valuation of pidilite is even more costly compared to paints stock on PE basis . Is the 70% market share the only reason or the distribution network ?

Would be great to know your thoughts on the above

Each paint companies has their own strength & markets

Asian paints is market leader is retail , Nerolac leads in Automotive & some industrial sectors also , Berger is leader in bulk segments in both real estate and industrial segments .

Geographically also market shares are different for different paint companies

Asian paints has steady sales and distribution policy - staff work by strict SOP and rules - typically slow in decision making vis a vis rest of players . But this works well in retail segments while creates issues in bulk segments .

They also have not been able to turnaround international operation for last 15 years .

On other hand berger paints has slowly grown out of its bulk segment focus to retail segments - It prices product lower than AP and also is been able to get few great dealers in key markets through special annual deals & sales support.

But internal talent pool for both Berger and Nerolac is very weak compared to Asian paints hence sustainability is often an issue for these competitors

Berger Paints is a great company and somehow they have managed to stand their ground and innovate in the industry. This also goes to show how strong the business of asian paints is to withstand a competitor like Berger Paints. It also shows the strength of Berger Paints to compete and hold its ground against a company like Asian Paints. It is a great industry to bet on (valuations aside) and I think most would be comfortable holding both of them if they were to invest in the industry. I do not have particular reason/rationale (I dont hold either) but Asian Paints are looking into other avenues and products now so that is quite interesting.

I would believe so! Loctite is an MNC product sold by one of the largest Adhesives company in the world called Henkel. They tied up with Asian Paints in India. And they have not been able to come close to Pidilite inspite of the strength of Asian Paints network.

One must understand that we spend alot oof our time using products that have adhesives in them. The cost of adhesives as a % of furniture etc etc: is very small. But a poor quality adhesive could result in the product falling well below standards. So there is a high degree of switching cost in the adhesives space. Even for retail, consumers we would spend a few rupees extra to buy a pidilite product. And Retailers and distributors would much rather stock Pidilite products as they move much faster.

Motilal Oswal has a small research write-up on the same.

What’s your take on Nerolac? They are market leaders in automotive and industrial paints and seem to shift more of their attention to decorative paints by leveraging their success on auto paints (At least the current commercials of the company seem to suggest it). With a MNC parent, negligible debt and a slightly lower valuation (expected because of its focus on cyclical sectors and that such paints have lesser margin) how do you think of it as a coffee-can type investment?

If I was comfortable with valuations I would not hesitate to buy all three of them! I could be mistaken but I believe Kansai Nerolac was in a few of the coffee can iterations written by Saurabh Mukherjea.

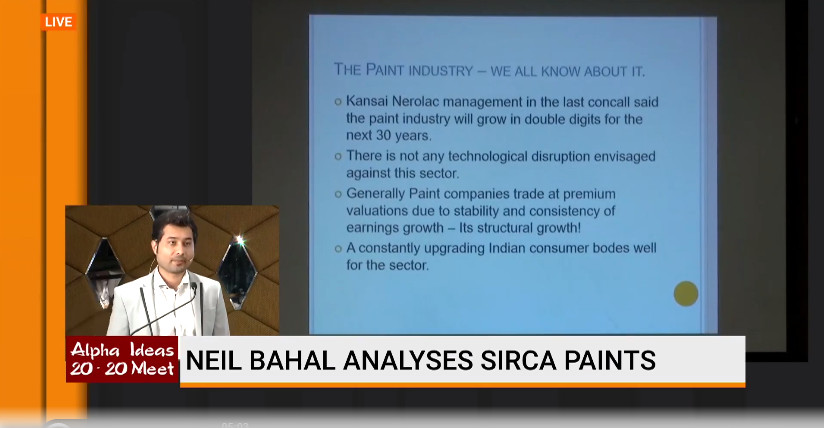

If I’m not wrong Neil Bahal in his alpha2020 talk on sirca paints said that Kansai Nerolac had stated that they expect the paints industry to give double digit cagr growth for the next two decades or something. Needless to say any number compounded at double digit cagr for 2 decades will result in quite a satisfactory sum haha!

My personal opinion is that people underestimate the power of a quality product, service and brand in the building material space. From Adhesives to Sanitaryware.

Facebook was founded in February 2004, Uber in March of 2009, it has a been a long time that we have been in the world of startups, innovation and disruption. For over a decade now funds have been willing to invest capital and back innovative founders with the desire to scale up. We see start ups taking on the alcohol space, that is a difficult space to penetrate due to multiple reasons (Beer companies like Bira). However, it must be noted that till date we have not seen any startup or idea gain any sort of traction in the adhesives space, paints space or even the sanitaryware space. It is not at all an easy space because of switching costs. It is highly improbable that a contractor will switch his adhesive to a new brand even if it costs less. In my personal biased view these companies can sweat their brands for the next 20 years without much external threat. (unless of course the economy slows down, black swan etc:)

I agree with you regarding Paint and Adhesive space. I feel that the companies in these two spaces are much better able to create differentiation through R&D and Patent compared to Sanitary-wares. The only differentiation Sanitary-ware companies have is the brand. Any new features added to a product by Kajaria can easily be copied by Cera or Somany. I feel even Hindware, Parryware, Nitco, Orient Bell have more or less similar kind of offering. In contrast the Paints or Adhesive companies work almost in an oligopolistic environment.

great discussion on paints and a lots of learning thanks to @1.5cr & @kb_snn . I even started reading "the unusual billionaires "book yesterday and has got a lot of insights . Thanks for the book recommendation @1.5cr .

Paints industry is one of the most secular industry followed closely by Adhesives industry and has a long run way with consistent performance in the past . And best part is this companies has a great role to play in development as compared to FMCG names

1 However when I observe the performance in the last 5 years , the performance of Berger paints is better than Asian paints .This is reflected in the share price . Is it due to the huge size of Asian paints and does it find difficult to gain market share given the huge share or whats the other reason ?

2 How is the forward outlook between Berger paints and Asian paints , is Asian paints expected to catch up or Berger with its innovations will go ahead ?

I’m not sure about the exact numbers but Asian paints does have a 50% plus market share in the decorative paints business where the organised decorative paints market in itself is probably at least 70% of the decorative paints market. So they probably make up around 70% of the organised market share itself. A company that has 70% market share will struggle to grow above industry growth levels in that segment. Take Pidilite as an example.

I think one has to do more research on each of the three companies to find out what segments they operate in/ are planning to scale up in, market share in their core segment, other growth plans (I believe Asian paints has entered home decor and water proofing), Capex plans (I think asian paints is looking to increase capacity by a large amount in the near future) and basically the company’s future plans on how they further grow having captured such a large share of its core market. And then ask the question, can they grow faster than the industry as that would most likely mean that they are capturing market share.

I think a bottoms up analysis on all three is a good place to start!

P.S I’m nowhere close to the knowledgeable investors and analysts on this forum so please take whatever I say as a mere opinion to the best of my knowledge.

1 Part of the reason could also be that Asian paints has tried to diversify into modular kitchen etc businesses (although that currently forms a very insignificant part of the portfolio ) while Berger paints is fully focussed on Paints industry . May be it may indicate that Berger is bullish on growth prospects while Asian paints, as you rightly said due to higher market share might find growth comparatively difficult top maintain although I am just a amateur investor and may be wrong .

Another area is also may be if you look at 2006-2011 , paint industry had very high growth rate and last 5 years performance isn’t that strong . It may be due to lack of pricing pass over to consumer and crude oil prices . As per one of the mgmt concall transcript , the earlier period was a period of rising prices while the later was a period of falling prices which also contributed to the profitability difference . So views of inflation going ahead may also seem to have an impact .

2

Even I believe that but in case of a developing economy like us and road construction and development ongoing, Wouldn’t there be sizable chance of market itself expanding ?

My only issue here is that one cant make more than earnings growth rate as there is practically no scope of pe expansion in view of oppurtunity size already prized in .

Would love to know yours and others views on this ?

Great suggestion this @1.5cr

Can smart city project etc have an impact on this industry growth rate ?

i think paint and adhesives are quity sticky buisnesses.

its not something that someone uses daily like a fmcg product.

So for eg, if i want a biscuit, i can try Britannia today, patanjali tomorrow and parle later… however i would use a paint and adhesive product mostly once ever 4-5 yrs and that makes me stick to the brand and trust that pidilite and asian paints have carved for themselves.

i dont think we need to worry about market share for the leader of the segment, because the base of market will always keep growing and as long as its market share doesnt reduce, i am okay with it.

Again, sales and distribution of both these cos are quite a moat that competitiors may have difficulty in crossing…

Completely agree . And more importantly , its the distribution network strength of Asian paints and Berger which is very hard to replicate in other industry (due to the paint industry dynamics ) as also the robust supply chain management monitoring delivery

The video that @1.5cr above posted of Marcellus Q&A with clients is really worth listening to , to understand the supply chain dynamics (which is the main source of strength ) in paints industry