I doubt they will release their weights anywhere. They may speak about them during the Webinar’s in one off cases for one or two stocks.

Everyone already knows their stocks, I do not think they will release their weights haha!

I doubt they will release their weights anywhere. They may speak about them during the Webinar’s in one off cases for one or two stocks.

Everyone already knows their stocks, I do not think they will release their weights haha!

Nice Newsletter from Marcellus on capital allocation of such companies…

They have exited Marico and added Divis as per this newsletter…

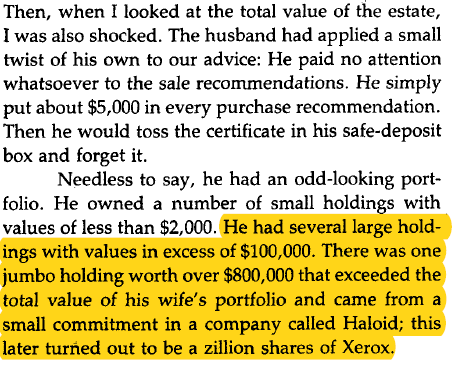

I read Original Robert Kirby Article published in 1984 where he explain coffee can investing approach first time. The example which he mentioned about success of Coffee Can was $ 5,000 invested becoming $ 800,000 in company called Haloid, which later become Xerox. I do not have any information about other companies, but it does mentioned some companies holding being more than $ 100,000. I am pasting relevant extract from 1984 publication in which we mentioned about value of various companies in portfolio.

So, we do not know date. I assume same being somewhere near 1980s (article was writted in 1984). Price of Xerox in 1980 was around USD 27 per share, going up high of USD 180 in 1998 and then steep downward decline to USD 35 in 2020 as sourced by me from Yahoo Finance.

Since we do not have any information about other holdings in the Kirby Coffee can portfolio, we can not conclude conclusively. But just wondering, the largest holding in portfolio, Xerox has provided provided total shareholder return of 7.5% p.a. (dividend and price appreciation adjusted with split) since 1980 has When one compare same with S&P 500, it appear very mediocare performance in relative sense.(Please refer to light blue line in Xerox price, that is S&P 500 Index).

Hence, Coffee can may work, but there is no substitute to hard monitoring. Fill it, shut it and forget it applies only to Hero Honda Motorcycle and not for portfolio investing my view.

I am enclosing my calculation for Xerox share return since 1980 in US market.

@basumallick

HUL last 10 years sales cagr is around 7% only and profit cagr is below 10% while stock price rose at above 25% cagr which seems irrational.

Basic question still remains the same: what is the definition of quality? and why HUL should be given even 30 PE if its earning cant grow even at 15% cagr? isn’t it a speculation?

“What is quality” is not an easy question to answer. To people like Joel Greenblatt, quality is high ROE or ROCE. HUL, btw, has an ROE of 82% and a ROCE of 116%. This means if you have invested 100rs, every year you are getting back 82-116rs from the business. This is just one way to look at it.

Other ways of understanding quality is longevity of the business. Can it last 10-20-50-100 years?

Another is from the customer viewpoint - are customers loyal? Do the company have durable brands? How frequently do the customers buy the products/services? Are the customers willing to pay a premium to competition? Are the products/services available across a large geographical footprint?

The list can go on… but I hope you get the idea. Fixating only on growth is absolutely the wrong way to think about businesses. For example, an HUL or a Nestle can possibly grow at 8-10% for the next 50 years. There are not too many companies that you can think about in those time frames. A lot of high growth businesses will not even last half that duration.

Caveat: Please read the below post only if you think a 15-20% CAGR over the long term through Coffee Can method represents a good return which you may want to aim for!

I came across the book, Coffee Can Investing, last September randomly at the airport and thought to give it a try given all the carnage in equity markets at that time - wondered this book couldn’t do much more harm to my already bleeding PF ![]()

And thank god that I read this book in-spite of some people saying this book is nothing great!!! I have become a big fan of Saurabh Mukherjea ever since reading this book!

There are probably hundreds and thousands of books out there which tell you how to pick stocks, identify great businesses, make money in equities, bla bla bla. But none of them are as simple and as rule-based as this one!

This is the beauty of this book - with just 2 simple rules mentioned in the 1st post (non-financials 10 year revenue growth and ROCE %), you can identify some of the best fastest growing businesses in India led by excellent capable managements! (You may want to slightly modify the 10 year YoY revenue growth to 10 year CAGR depending upon some companies which might have had some global / domestic event / incident impacting their business for a short duration. Bit of a personal call there on what you’re willing to live with)

And if you put a couple of further conditions on the above filters - non-cyclical, B2C business, low debt, promoter holding, CFO trend, etc. and you could get a winning portfolio!

But then the next question? How do you build your portfolio? How much to allocate to which company?

For most retail investors, this book has the perfect answer! Once you identify those great businesses, just have equal weight distribution across them and forget it for 10 years! Because as this book showed with back-tested results - the winners in the PF will become a substantial part after 10 years while any losers will become inconsequential.

And over 10-15 different back-tested CCPs from 2001-2017 - it sure does beat the benchmark Nifty/Sensex significantly!

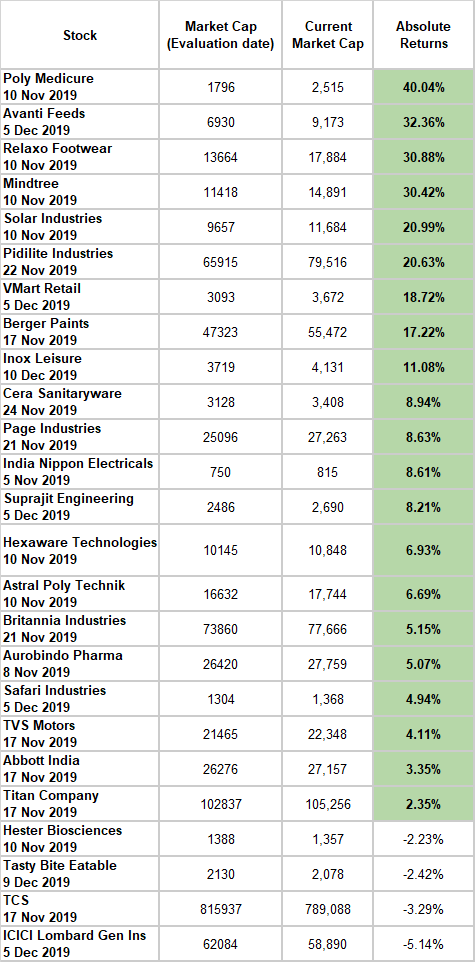

Okay - so the proof of the pudding is in the eating, so after finishing reading this book in Nov, I got down to trying to identify some businesses which fit the Coffee Can style of investing.

I’m sharing some of the companies which I’ve been able to identify over November-January (2-3 months)

I’m invested in some of the above companies and think the absolute returns using this approach on Coffee Can Investing speak for themselves.

I know it’s an extremely short duration to come to any conclusions - but the single most important aspect I find in the above list of companies is the low risk of complete blow-up of capital and 100% loss of capital. Something which has been a real risk in some of my previous investments.

It is also no wonder that their PMS Consistent Compounders Portfolio has delivered a 30% return in FY20 when compared with 3% of Nifty!

The only thing which has changed between my earlier method/approach of stock selection where I ended up stepping on some live minefields and my current approach is purely this book!

Cannot recommend this book and approach enough to new retail investors!

PS: I have also read One up on Wall Street, The Thoughtful Investor, 5 Rules for Successful Stock Investing and few other books and none even comes close to this in my view.

I think you yourself have identified the pitfall in the table as it’s an extremely short duration to judge. If you go a little behind, there were many companies rising 5% every week (eg pcj, DHFL, Vakrangee, yes bank and many more) and I used to wonder why I missed them. Some of the channels used to recommend them v frequently with higher targets.With a huge loss in some of them, I have reached the conclusion that management Q and integrity, clean intentions are the most important aspects while choosing a company for investment.

Valuations are what people have a concern with, with such names.

In 2017 many justified the valuations of small caps and mid caps.

In 2017 asian paints traded at around 45x on PAT of 2000cr.

In 2019 end of FY PAT of Asian paints was 2200cr and the PE was nearing 70x. TTM PAT is around 2700cr and it trades at a 65x multiple. In the past few years clearly returns have come from multiple expansion.

Berger in 2017 traded at 45x and earnings were around 450cr. In 2019 earnings were around 500cr and the multiple had expanded to 65x. TTM earnings are 600cr and the multiple is 90x. Again here we can see that returns have come from multiple expansion. Usually multiples expand to abnormal levels when there is some sort euphoria being built. This happened in 2017 and 16 with the small and mid caps. At that time no one wanted to buy these bluechip companies.

During the peak of the 2017 small and mid cap rally Berger traded at 50x, Asian paints at 50x, Nestle around the same 50x (I dont recall when the maggi issue happened). If you look at it in that way, the last three years the multiples of these companies alone have expanded very meaningfully coupled with some moderate PAT growth. So returns have come largely through re-rating as was the case with small and mid caps during the peak year(s) of the rally.

ITC traded at 45x in 2017 and at around 40x in 2013 and today trades at 16x and earnings have grown from 7500cr to around 12,500cr in 2019. These things can also occur with such franchises if there is a disruption or distortion to the terminal value premise.

If JSW Paints starts rapidly garnering market share we may see a derating in Kansai Nerolac or Berger Paints. We can look at Page as well as a recent case. In the short run that is 3-5 years the multiples can influence the outcome either way. And in many cases it can lead to a long time correction until the earnings and fundamentals catch up.

If one looks at the case of ITC, the business is stronger than it was in 2013, the company is far more diversified from cigarettes than it was in 2013. Inspite of everyone understanding taxation on cigarettes, the stock has still derated very heavily.

The truth is that this method is only back tested. Even Ambit does not have a decade in practice to show for it. And the market, India & the companies were very different 10-20 years ago. Asian Paints in 2008 had sales of 4000cr today it does close to 20,000cr that is 5x increase in top-line alone over a 10 year period.

Can asian paints do 1,00,000 cr in top line by 2031? and most importantly will it still command a 35-40x multiple at that point, let us understand that the business is far more mature today than it was a decade ago and will be far more mature as a business and industry 10 years ahead.

If the PE halves over a decade that means a minus 7% cagr just on account of derating. Assuming an 18% cagr growth in earnings over a decade and a halving of the PE from current 70 or so to 35 you are looking at something like 11% plus some dividends.

This is all assuming that indeed earnings do grow at 18% and the multiple is not below 35x or half from your purchase price at the end of the decade

There are many caveats to this method and over the last 2 years it has worked very well due to circumstances of the markets. And of course on back testing it has worked very well as these businesses were much smaller back then.

The premise is exactly what marcellus states. But please understand that Marcellus is an actively managed fund and Marico was part of multiple coffee can iterations until recently as per them. In fact they hold some auto companies as well, so they look at alpha through playing cyclicals. And he has said this before as well regarding pharma and playing the rupee depreciation.

It is not at all a passive portfolio. I do not think Divis was part of any of the iterations. Dr Lal is another recent candidate and could end up being their best performer looking at the growth runway for path labs in India in general. Further I do not think Dr Lal has a 10 year track record to make it to the list (do check on this) and perhaps Asian paints looked the same a decade and a half ago.

If this is a method that you want to follow then it makes sense to invest in the PMS. Otherwise please be wary changes in the fundamentals of these businesses. Marico has been a favourite for a long long time, in fact in his first book a lot was written about the business.

This is an active investment philosophy. It is just that the companies are well known household names in a sense.

Further, Marcellus has launched a small and mid cap PMS recently to the public. I think one should go through that data as well. I’m sure they see some value in that space.

Can you please share the list of probable stocks under Marcellus PMS of Consistent Compunders and Little champs if you have ?

Thanks

@arpitjain512 I’m not invested in either of their funds.

Their website has alot of info on their coffee can pms, if one reads their newsletters, books & watches their webinars the names would be pretty clear. If you were to simply scroll this thread I’m sure you will get a broad view of what names their PF might have.

This is actually a very good point - over the last 12 months there have been way too many people out there trying to justify the quality at any price theme and the stock price movement is backing them up as well ![]() . But it has to end someday right! Who knows when

. But it has to end someday right! Who knows when ![]()

Even though the method is back-tested, that data and last many years market environment is enough for me to agree with the conclusions being drawn by them. In any and every market (except some black swan global catastrophe when the whole market will go down) businesses with long runways of growth (over decades) having high return on capital >25-30% and ability to reinvest capital at those rates with reasonably long execution track record of management will always do well, outperform any major market indices and command premium multiples because such businesses are extremely rare. The rush to own such rare businesses can obviously lead to some type of a euphoria as well (we may well be in that euphoria phase now). However, such businesses rarely lead to capital destruction and wealth erosion especially if the growth doesn’t just drop off a cliff for an extended time. And in that case, the market’s perception itself of a particular business being an extremely rare quality business would be wrong.

Agree with this line of thought - that’s why I have a few more filters on top of the one proposed in the book. I check the difference between the 10 years revenue CAGR growth rate and the last 3 years CAGR growth rate. If there is a huge difference with former being more, then it’s a strict no no due to fast dropping growth and expected de-rating of multiples.

Example:

TCS - Revenue Growth

10 yr 18% CAGR

5 yr 12% CAGR

3 yr 10% CAGR

That’s why even though a company like TCS shows up as part of Coffee Can methodology - I’ve skipped investing in it.

If everyone had 1 crore to invest in the PMS ![]() . This is the new minimum for the Little Champs PMS. Don’t know about the other - even 50 lacs is a lot at my age of 30

. This is the new minimum for the Little Champs PMS. Don’t know about the other - even 50 lacs is a lot at my age of 30 ![]() . And yes I’m aware about their Consistent Compounders Portfolio having an active investment philosophy.

. And yes I’m aware about their Consistent Compounders Portfolio having an active investment philosophy.

The point I’m trying to make is there are 5000 companies listed on the BSE. Their approach and methodology helps you shortlist that to about a 100-150 market cap agnostic investable list of companies (out of which I’m pretty confident more than 50% will be honest fair managements with solid growing businesses).

It seems a reasonable expectation to do the hard work of trying to identify 15-20 solid businesses within those 100-150 companies which can give above average returns over the long term.

This helps build a very solid base to the portfolio which then gives you the option to experiment and go out of the comfort zone if people still want to try their hand at IPOs, special situations investing (de-mergers), technicals based calls, etc. A solid portfolio will not be significantly impacted by the odd wrong call.

For me that filter of removing four thousand nine hundred odd companies (even though some of them may be huge winners historically - doesn’t matter you only need a handful of good businesses to change your life) is a huge huge head-start which should not be underestimated.

PS: As been highlighted this CCP methodology is purely based on back-tested results. Since I’ve recently started following the coffee can method, I will get to know the results only with time which I shall share on the forum at regular intervals.

Great point. This helps address one of my major misgivings against the coffee can method.

I have scanned most of Saurabh’s interviews in CNBC since almost 4-5 years. GMM Pfaudler and Alkyl Amines seem to be two names that are a part of the Little Champs portfolio. Any other names one can think of?

I’m also thinking Amrutanjan Healthcare is a part of it.

Mr. Mukherjea is among the smartest investors in the world.

It is pretty clear where he feels returns will come from over the next few years…

https://marcellus.in/newsletter/little-champs/introducing-little-champs-marcellus-small-cap-pms/

Kotak Bank a Coffee Can Franchise?

I have been reading into Kotak Bank. Below are some insights (please go through the kotak thread as well as it has a full write up)

It has survived every crisis including the recent blowup. Whatever be the crisis we rarely see Kotak and HDFC’s name among the lenders.

Large scale corporate lending has not worked in terms of long term wealth creation for a long time, so why bet it on it now. Kotak has a very strong Retail Franchise.

ROE is low primarily due to Kotak’s lower leverage (on average 5x vs 8-10x for other banks). If this were to expand ROE’s would increase as well. This is the risk averse nature of the management. And clearly this has carried through in their lending business as well.

Kotak has a very high CASA (50%, highest in the industry I think). They do pay high rates on their Savings accounts to bring in customers. However, they are slowly decreasing it and this extra income will flow straight to the bottom line over the next few years thereby giving a big fillip to ROE (mentioned in the company thread). CASA is a very sticky form of funding and people rarely change even if customer service is poor (not saying Kotak’s is at all). With the fear of smaller banks winding up, the big guys will benefit from this.

Kotak has its other businesses under its listed banking business. That its AMC, Insurance business. AMC ,wealth mgmt, brokerage are business that do not need equity to grow and hence this can given kotak a kicker on its ROE hopefully as they scale.

Fee income is of course a big factor in expanding ROE for a bank. And Kotak’s Fee income has grown from 1500cr in 2014 to around 4500cr in 2019 that would be more than 25% cagr.

I think they had maintained a higher ROE of 15% plus until the ING Vysya merger post which ROE fell to the 13.5% range and stayed there. This should improve as CASA rates are slowly decreased, Fee income grows & their other businesses grow.

Typically ROE will be around ROA x Leverage. ROA usually shows the underwriting process of the bank and its other income streams etc:. So ROA of Kotak is 2%+ around the same as HDFC Bank’s.

But Kotak has a much smaller fee business, credit cards business etc: (I don’t know all the businesses that both banks house so do check on that). This shows that Kotak is an extremely high quality underwriting bank.

So as you can understand, if leverage increases then ROE increases. An ROA of 5% with a 2x leverage will be nowhere close to a 2% ROA and an 8x leverage. So effectively when a bank dilutes equity, its equity base increases and leverage stays as is, thereby as fresh equity is infused the leverage also decreases as equity has increased. This enables the bank to expand its leverage further in absolute terms till it reaches its pre-dilution levels.

Banking is a very risky business and Kotak is among the most conservative lenders. There is also some comfort from the other businesses. But for Kotak to ramp up their ROE’s as per my limited understanding they will need to increase their leverage or increase their ROAs, increasing ROA’s beyond this number would be a very tough task unless their other busnesses and fee income skyrocket.

I think they could be a good core position along with HDFC Bank for ones long term portfolio on the financial services side.

Came across “Voya Corporate Leaders Trust”. Seems the strategy is somewhat similar to Coffee can method. It was created in 1935 with an equal number of shares of leading U.S. companies at the time. One of their rule is they dont purchase new companies ![]() . And seems they have been doing pretty ok ! Last 10 year returns from fund is 12.05 vs S&P returns of 13.97. Though it appears slightly underperforming, i think this is not bad returns.

. And seems they have been doing pretty ok ! Last 10 year returns from fund is 12.05 vs S&P returns of 13.97. Though it appears slightly underperforming, i think this is not bad returns.

Extreme Coffee Can Portfolio: The fund’s original sponsor was Corporate Leaders of America. Today, after a series of deals, it’s under Voya’s umbrella. The original fund had a simple mandate, as described in a brochure on the fund’s history: The founders of the Trust bought equal shares of 30 leading companies in 1935 and decreed they could never be sold. The only exception was companies that went bankrupt, merged or spun off. In fact, it’s beaten the S&P 500 for 40 years. The fund’s website doesn’t go back any further than that, though I wonder what its performance has been like since inception. - Chris Mayer

Read this on twitter …amazing analysis by Gordon@gordonmax

2/ Over the last 10y the Bank has grown its other income from 3.7k cr to 15.2k cr (CAGR 17%). This includes fees commissions (~75% mix in FY18) , forex & derivative revenue, etc. So large was the other income that 1136 cr was booked under “Miscellaneous”.

3/ To put that in perspective the Banks “miscellaneous” income of 1136 cr is a respectable PAT for a large cap, and a respectable market cap for a small cap co.

4/ The cost for this income is marginal / negligible being incidental to the lending business. I doubt the outer limit cost for generating this fee will be more than 500 cr. It can be safe to say that fee income contributes 50%+ of the Banks PBT

5/ So if fee income growth matches your ROE, all you need to do is not screw up on your lending. That is relatively easy since you cherry pick borrowers with CIBIL score of 750+. Hence its likely that fee income drives the strategy rather than being like cream on the cake

6/ So where does this fee come from? Large part from cash management for corporate supply chains (incl vendors, distributors, dealers). HDFC is a leader in the space. Once you have your vendors and distributors on the system moving banks is not easy, its impossible. Strong moat!

7/ So when payments are processed, the money doesn’t leave the bank, even better it’s a float for a day, on which the bank pays no interest, in fact gets a fee! More transactions, more float, lesser cost of funds and more fee

8/ Then, it’s the largest collector of direct and indirect taxes with 22% share. This also contributes to float. As tax collections rise the Bank will benefit even more. This is probably the most direct play you can have on unorganised to organized

9/ Beginning with NSE when it started, HDFC is also a large player in clearing services for stock and commodity exchanges. Again as direct a play as possible on higher equity participation in India and a deepening commodity market

10/ Another good part of other income (~12-15%) is distribution of financial products – home loans to HDFC Ltd, MF to HDFC AMC, insurance to HDFC Life/ Ergo, etc and to their competitors also

11/ Unlike other banks treasury income / assets is lowest, implying they are very conservative on treasury.

12/ All this makes me quite comfortable that fee income will continue to grow at 18% if not higher. It is like a positive feedback loop. The more it grows, the stronger it becomes. Given the trends on tax compliance, unorg to org, insurance pen., the runway is really long

13/ This strength allows HDFC to select the best credits. It doesn’t need to run behind lower CIBIL scores. Its an added strength that the Bank is nimble, smells a troubled loan from afar.

14/ Long before fintech crawlers the bank kept a hawk eye on account balances and inflows. Then if your vendors and distributors are also on the system you can tell if something is wrong months before it becomes a sticky issue.

15/ In conclusion, I think (my view, feel free to differ) the Bank is a better risk adjusted alternative to most of the other derivative stories on India’s growth. The retail service sucks most of the time, but that is a small part of the larger story

Found this on the HDFC bank thread posted by @karanjariwala