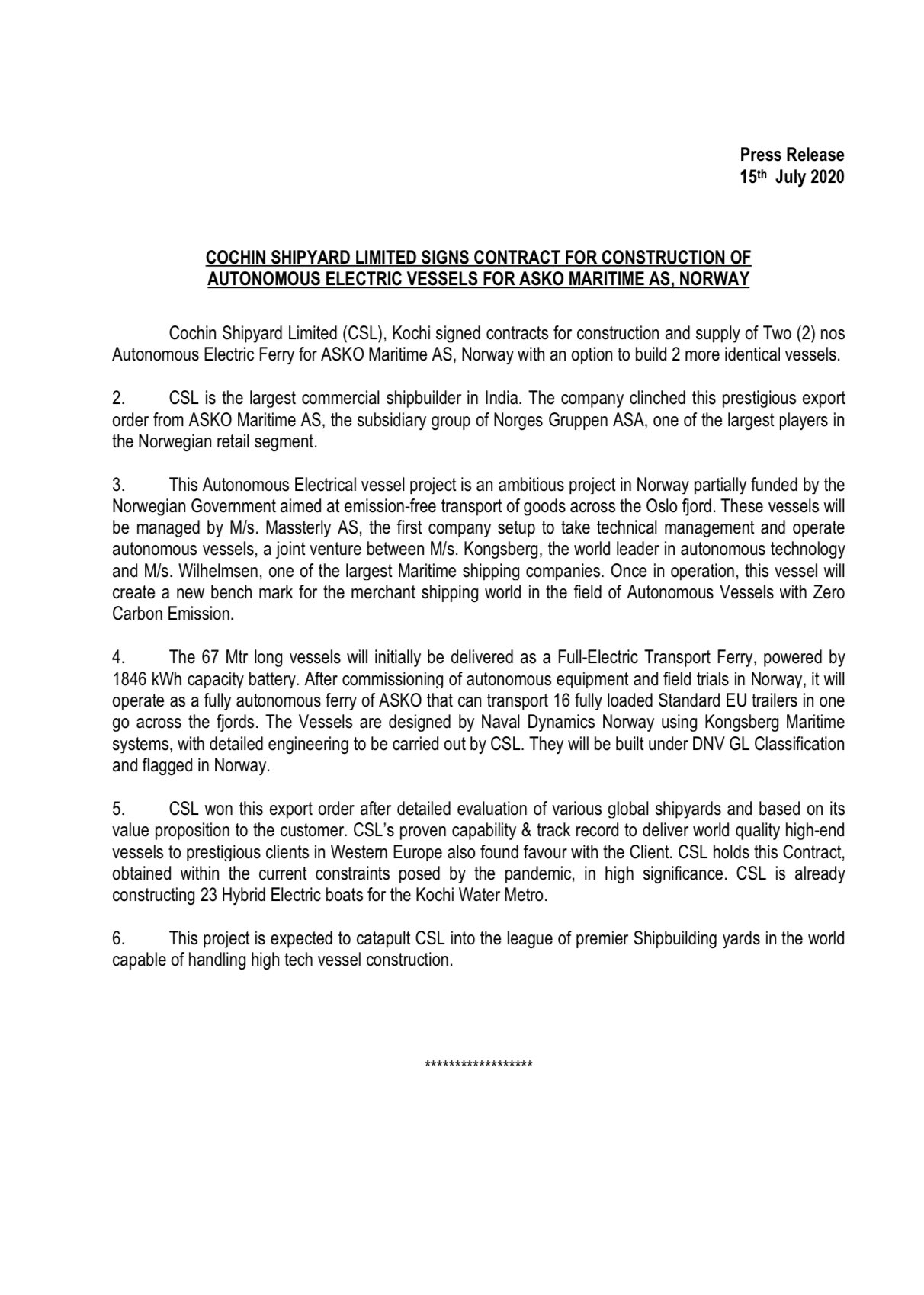

Thanks to this thread, I started looking into the Indian shipbuilding industry a week back. Below is my summary. Hope it helps others in this forum. Caveat: I have no experience/contacts in this industry. Below is a summary of the various ARs/Research Reports. Links to these is given at the end)

Shipbuilding Industry

The shipbuilding industry consists of both new ship construction and ship repairs. Within each segment, companies are involved in both defence and commercial.

Commercial Shipbuilding

Commercial shipbuilding consists of cargo ships, tankers, fishing boats, passenger ships etc. Commercial shipbuilding is a cyclical industry and is currently witnessing a slowdown. Maritime trade witnessed a drop in FY18. As a result, the global commercial fleet has grown by only 3% in FY2019. China, South Korea and Japan have been involved in a fierce competition and own 95% of the order book. Europe has only 1.6% share of the remaining. (source)

Defence Shipbuilding

Defence shipbuilding too has witnessed a slowdown due to cutback in military spending. It is expected to pick up due to replacement of older ships. More importantly, defence is not cyclical and is a counterbalance to the cyclicality of Commercial Shipping.

In India, the Indian Navy has 140 ships and the Indian Coast Guard has 120 vessels. Both are expected to grow to 200 each. The government will placing orders for 165 ships by 2022. The estimated capital budget for up to 2027 amounts to ₹4.5 Lakh Crores - submarines (₹2.2 Lakh crore approx.), destroyers / frigates (₹90,000 crore approx.), aircraft carriers (₹45,000 crore approx.), corvettes, landing platform etc.

Defence projects have always been awarded on a nomination basis to the Defence PSUs (DPSUs) with a fixed margin - MoD has set it at 7.5% (source). However, the Government is now moving to a RFP based competitive bidding process, leading to better margins for DPSUs and opportunities for private players. Additionally, the government has provided for a Right of First Refusal (RoFR), which will provide priority to bidders building the vessels in India.

Ship Repairs Industry

Ship repair and maintenance services market is estimated to reach $40 billion by 2028. Though India’s share in global ship repair is less than 1%, the country’s location is favourable with 7-9% of the global trade passing within 300 NM of the coastline.

The new environmental regulations, such as Ballast Water Treatment Convention (BWTC), the Energy Efficiency Design Index (EEDI), Emission Control Areas (ECAs) and the 2020 Sulphur Cap, are expected to impact the ship repair market as well.

India has a market potential of ₹2,600 crores from repair of domestic fleet out of which only 15% share is currently captured. Further India can grow its ship repair industry to ₹9,000 crores in the next 10 years through infrastructure and process improvement

As per the Maritime Agenda 2010-2020 issued by Ministry of Shipping, the following targets are set for ship repair industry:

- To be self-sufficient in ship repair requirements of the country and to emerge as a dominant ship repair centre.

- To achieve a share of 10% in global ship repair industry by 2020.

One of the major initiatives under the Sagarmala project was to lease out the ship repair facilities available at the major ports to specialists to generate more revenue and create a positive ship repair industrial climate.

Industry Players

A comparison of the capabilities of the various Indian shipbuilding companies is shown below (source)

|

Defence |

Commercial |

Others |

| Mazagoan Dock |

Destroyer

Submarines

Frigate

Corvette |

Anchor Handling

Water Tanker

Dredger |

Floating Cranes

Pontoons |

| Cochin Shipyard |

Fast Patrol Vessels

Corvette (ASW) |

Platform Supply Vessels

Anchor Handling |

Ship Repairs |

| Garden Reach |

Frigate

Corvette (ASW, Missile)

Fast Patrol Vessels

Landing Craft Utility

Landing Ship Tank

Survey Vessels |

|

Portable bridges

Deck machinery

Engine test and overhaul |

| Goa Shipyard |

Frigates

Landing Craft Utility

Patrol Vessels

Survey Vessels

Interceptor Boats

Mine Sweepers |

|

Ship Repairs |

| Hindustan Shipyard |

Submarines

Patrol Vessels |

Tugs |

Pontoons

Ship Repairs

Submarine Retrofit |

| L&T and RNEL |

Landing Platform Dock

Patrol Vessels

Interceptor Boats |

|

Ship Repairs |

| ABG |

Interceptor Boats |

Tug Vessels

Cement Carriers

Diving Support Vessel |

|

A quick comparison of these companies

|

MDSL |

CSL |

GRSE |

GSL |

HSL |

RNEL |

L&T |

ABG |

| Financials |

2019 |

2019 |

2020 |

2019 |

2019 |

2019 |

|

|

| Revenue from Op |

4649 |

2962 |

1433 |

905 |

605 |

180 |

Amalgamated into L&T |

Delisted |

| PAT |

519 |

481 |

174 |

131.52 |

36.24 |

-10927 |

|

|

| NPM |

11.17% |

16.12% |

12.14% |

14.50% |

|

|

|

|

| EPS |

23.18 |

35.47 |

14.27 |

10.58 |

120 |

|

|

|

| Dividend |

45% |

36% |

72% |

56% |

|

0% |

|

|

| Shareholding |

Govt 100% |

Govt 75.21% |

Govt 74.5% |

Govt 98.3% |

Govt 100% |

|

|

|

| Order book (Cr) |

NA |

15253 |

26540 |

15319 |

2689 |

|

|

|

Thoughts

In the above list, CSL and GRSE are the only candidates for investment. The rest of the PSU are not yet divested and of the private players, RNEL is deep in debt. Below is a comparison of these two companies across various parameters

|

CSL |

GRSE |

| Business Profile |

Larger of the two with more revenue and shipyard capacity.

Defence contributes 80% of the revenues and makes the business less cyclical.

The company is working on the prestigious Indigeneous Aircraft Carrier (IAC) and ASW Corvettes for the Navy. |

GRSE is older of the two and larger in terms of delivery to Navy. It has delivered close to 105 vessels to the Navy. It is currently working on the large P17A frigate project. |

| Diversification |

CSL has good diversification with 28% of the revenue coming for ship repairs (defence 56% and commercial 44%). This segments has been growing at CAGR of 32% over 3 years.

This business is recurring and CSL has invested in ISRF (Internation Ship Repair Facility) to further grow this segment |

GRSE has Engineering and Engine Plant divisions, but these provide less than 5% of revenues. |

| Order Book |

Order Book is Rs 15253 Cr. A major portion (>85%) of this is contributed by the IAC and ASWC projects.

With IAC-I and IAC-II completed, Rs 6800 Cr is scheduled to be booked in 20~22 (delivery date) |

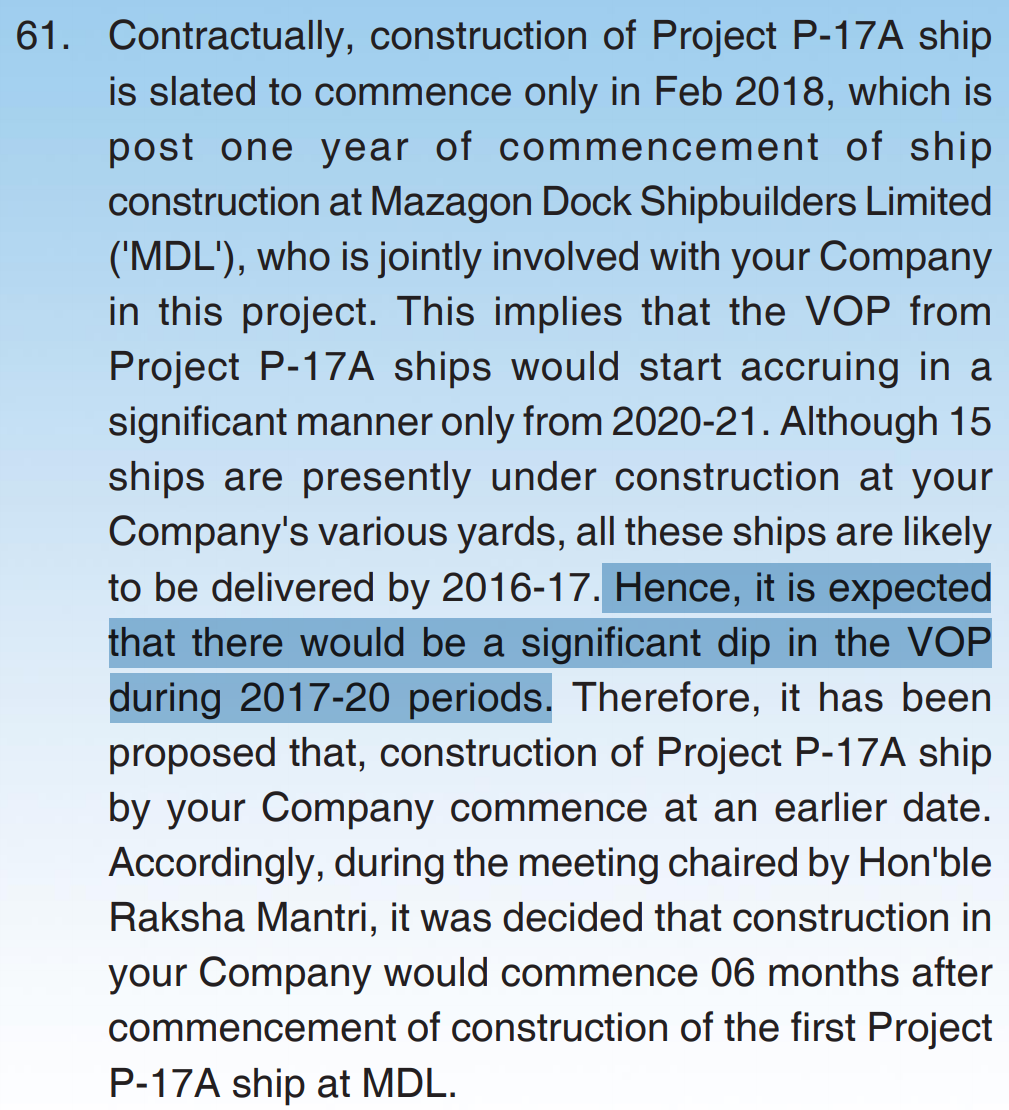

GRSE has a larger order book of Rs 26540 Cr. 66% of this is contributed by the P17A frigate project.

Bulk of the project payments is going to be over the next 3 years. The project is ahead of schedule and due to the COVID disruption, revenues are expected to jump from FY22 onwards |

| Ratios |

ROA - 9.07%

ROE - 14.61%

ROCE - 22.44% |

ROA - 2.58%

ROE - 10.67%

ROCE - 17.87% |

| Relative Valuation |

P/B - 1.06

P/E - 6.5

EV/EBITDA - 1.51 |

P/B - 1.98

P/E - 15.34

EV/EBITDA - 1.04 |

- It’s clear that the cash on the books of CSL is just optics and is due to the payment schedule of the IAC project. It should not be a trigger to invest in the company.

- There aren’t a lot of shipbuilding companies to compare and the international companies (Daewoo, Hyundai etc.) are not strictly comparable.

- Between the two, the market is assigning a higher P/E to GRSE. This could be due to the higher order book and upcoming schedule payments over the next 3 years.

- CSL does have a strategy to grow the ship repair business. It’s a nice diversification from defence shipbuilding, which has lumpy revenues.

- On the other hand, with defence projects moving from nomination to RFP mechanism, we can expect GRSE to have better margins and efficiencies.

- Both companies management do not foresee LDs due to COVID.

Both look like good investments. I am inclining towards GRSE. However, not yet decided on the ideal price and the entry point. Please provide your thoughts…

(Disc: I have just started looking into this. No investments and the above are not suggestions)

Ref: