In ship building industry, when a customer pays advance, usually it is against a Bank Guarantee. IMHO most of the contingent liability should be towards this. IMHO the order value of Rs.125 crores for 2 electric propelled vessels looks very low . Request you to check the concal once again.

PS: I have some experience in the Shipbuilding Industry.

1 Like

Hello respected members pls give us some comment on impact of raw material price hike for csl… is that big issue for company or digest these kind of speed breaker? And how much margin shrinkage for that issue?

2 Likes

3 Likes

Interesting development: India to develop and build first indigenous Hydrogen Fuel Cell Vessel: https://www.bseindia.com/xml-data/corpfiling/AttachLive/a60999a6-e7d3-482c-bce9-82a5f7dcb9c1.pdf

Great performance again. Q4 EPS of 21.6, 2022 of 45.

Debt free, Trading at 0.9 of book value as cash position improved significantly.

1.3x price to sales in covid impacted year.

5% dividend yield, which is expected to increase in coming years.

I think this has huge upside potential delivering dividend in worst case.

7 Likes

2 Likes

My notes based on Q4 2022 Concall:

Order Book close to Rs 20,000 Cr (majorly constituting of ASW and NGMV). NGMV order of 10000 Cr will be exhausted in 8 years. Rough revenue run rate from ASW and NGMV is 800 Cr each yearly. Overall order book strength is not great.

IAC contribution expected to be close to 1400 Cr and ASW contribution 600 Cr in FY23 revenues. Ship Repair revenues for FY23 expected to be ~900 Cr. Overall revenues in FY23 will be similar to FY22 reveues. However revenues will increase by 12% from FY24 onwards.

Management trying to get hold of International orders, being a PSU, I am not sure of its success, both from securing and execution of orders.

Both big CAPEX projects (ISRF and Dry Dock) delayed. Tentative timeframe of commissioning FY23-24.

The commentary from MD - Madhu Nair is quite clear and transparent and gives quite good view of where company stands.

6 Likes

My notes from the Q4 concall

- FY23 will be flat, FY24 will go up by 15-20% and FY25 by 12%

- FY22 turnover at different ports → Mumbai: 85 cr., Kolkata: 33-34 cr., Got started in Andaman

- Will have some headwinds in ship building revenue recognition in FY23, this will start growing in FY24 and FY25. Ship repair will do well in FY23 and be around 900 cr.

- For ASW SCW corvette, targeting revenues of FY23: 600 cr., FY24: 1’000-1’200 cr., FY25: 1’200-1’400 cr.

- For next-2 years, EBIT margins will be ~15% (will be higher at 18% in FY23 due to IAC order execution)

- Most of the commercial contracts (including naval) are fixed cost, only price pass through contract is with IAC

- 2030 revenue target is 10’000 cr., realistically they are targeting 6000-6500 cr. revenues by FY26

- In terms of competition in European markets, Cochin can outbid East European companies but Turkey and China are very competitive

- Trying to get orders of 120-130 m kind of vessels in Europe, this is a very large market with a large replacement demand coming up. Chowgule has done well in this segment executing orders for 20-25 ships

- Secured a new 900 cr. order for one large dredger from Dredging Corporation of India which could go up to 3 vessels

- Indian private ship companies only use Cochin Shipyard’s repair services for critical parts (like under water). PSUs on the other hand use whole range of ship repair services

Disclosure: Invested (position size here, bought shares in last-30 days)

11 Likes

Cochin Shipyard -A detailed study

3 Likes

Latest Interview of MD of cochin shipyard

Smooth Sail For Cochin Shipyard’s Orderbook Growth - BQ Prime Smooth Sail For Cochin Shipyard's Orderbook Growth

discl: Invested and hence biased . Not a buy or sell recommendation

Notes from recent BQ interview

05.09.2023 BQ interview

- FY23 was disappointing as supplies of certain components weren’t made in time to the shipyard which is why despite them having a good order book, revenues lagged

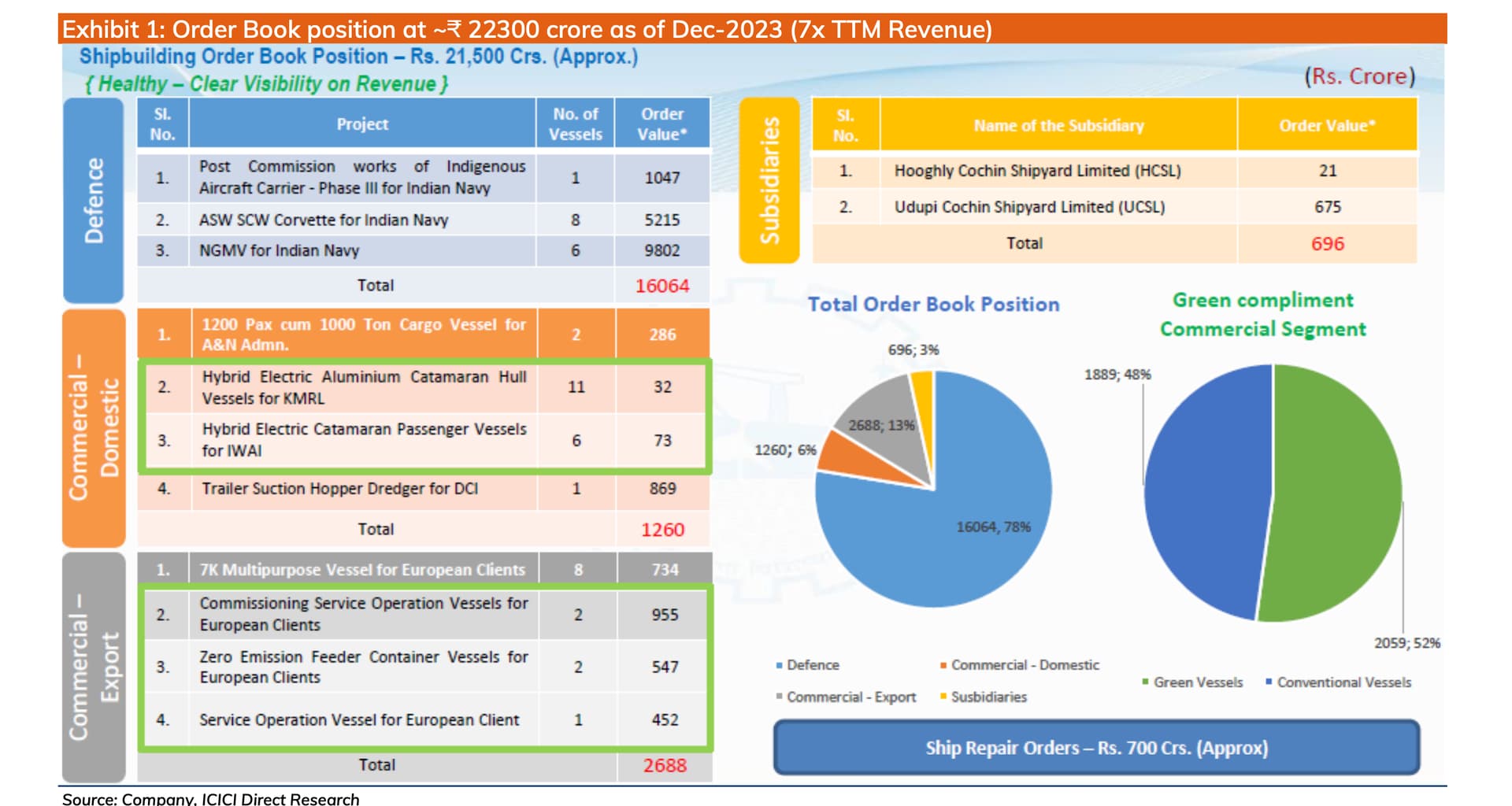

- Order book: 22’000 cr. (600 cr. ship repair + 21’4000 cr. shipbuilding)

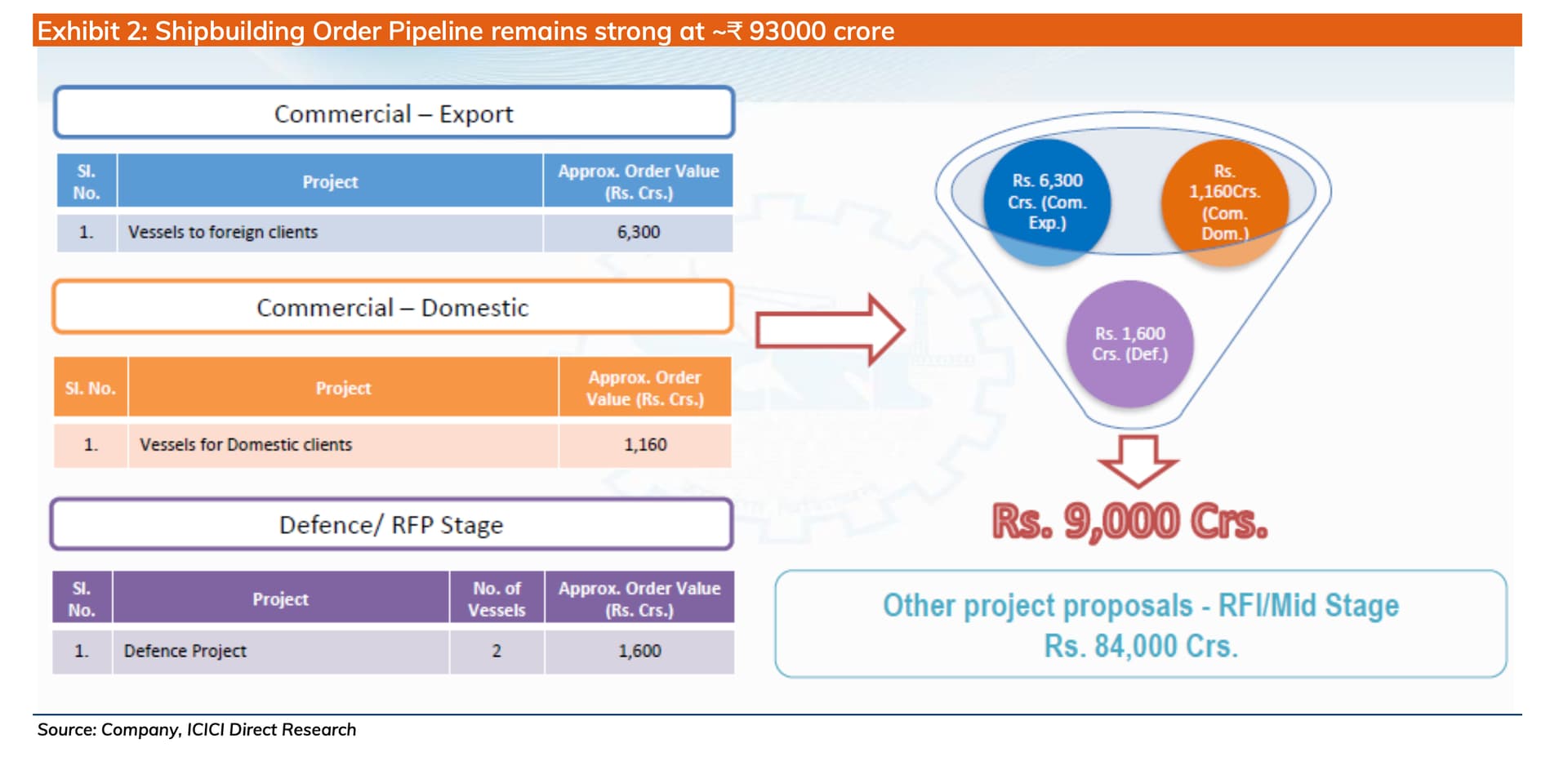

- Received order for 6 ships from Wilson Shipowning (Norway). Expect 8 more vessel orders after completion of this order. This gives them a break into Norwegian markets

- Defense: 48 vessels with total order book of ~16’000 cr. 8 ASW Corvettes (3 close to launch) + Next generation missile vessels (currently in engineering phase). Expected timeline of delivery of 5-7 years

- Not looking at submarine opportunity as its not their strength, focusing on naval defense, European green vessels and ship repair opportunities

Disclosure: Not invested (no transactions in last-30 days)

5 Likes

Would be great if you can share your views on below, As per AR FY23, the weakness mentioned in the business , none of them can be mitigated. I am wondering even if the execution improves, how will EPS increase. The weakness mentioned in AR are per below

- Virtually non-existent indigenous ancillary industries and consequently non-availability of major equipment/raw materials in India;

- Difficulty to arrange long term project finance to ship owners which is offered by other overseas shipbuilding countries;

- Higher finance costs and logistics costs resulting in higher input costs for production;

- Comparatively higher social and employee overheads and certain restrictive labour practices especially for contracting labou

- Governmental system induced procedural delays.

2 Likes

I have nothing much to comment on 2022-23 Annual report.

The key parameters as mentioned keep varing from time time ,Quarter to quarter as other economic conditions change. That is true for most sectors.

For Cochin shipyard quarterly performance in the past has been quite lumpy with poor performance for 1-2 quarters followed by excellent perfomance , which perhaps could even out the overall performance. If you refer screener data for last 3-4 quarters performance data, may be you can get some idea.

Market is valuing it due to bulging order book and expected further orders keep flowing due to Atma nirbhar Bharat scheme, strengthening Indian Navy and the other geopolitical situation. Also, these companies could benefit as India can be a base for ship repair maintenance for US Navy and other countries

I had invested as high dividend yield stock some 18 months back. I find now the stock is moving because of industry tailwind.

Discl…Not a buy or sell recommendation. please do your own assessment before investment

2 Likes

Good set of numbers from Cochin shipyards. Net profit up 61% Revenue up 48% Stock split 2:1 and Interim dividend Rs 6 per share announced

1 Like

PM inaugurates new Ship repair facility at Goa shipyard

Is this the news good enough to send the stock price to sky high today - increase by 10 %? especially on a day when the market is dull.

Not sure if there is some other news.

The Rs 1,799-crore dual purpose dry dock can be used both for ship construction as well as for ship repairs. It can accommodate large LNG carriers, Capesize and Suezmax vessels, oil rigs and semi-subs and other large vessels.

D8scl: Invested from lower level in my Defence basket. Not a buy or sell recommendation. pl do your own assessment before you invest

1 Like

How could a stock move up after a split ? Makes no sense. If there is no news then markets are irrational. Disclosure: Sold after split.

4 Likes

1 Like

2 Likes