That was a long post

Continuing further on entry barriers -

a) From this Business Today article published recently (http://businesstoday.intoday.in/story/private-sector-manufacturing-of-defence-equipment/1/203170.html), we have some important insights:

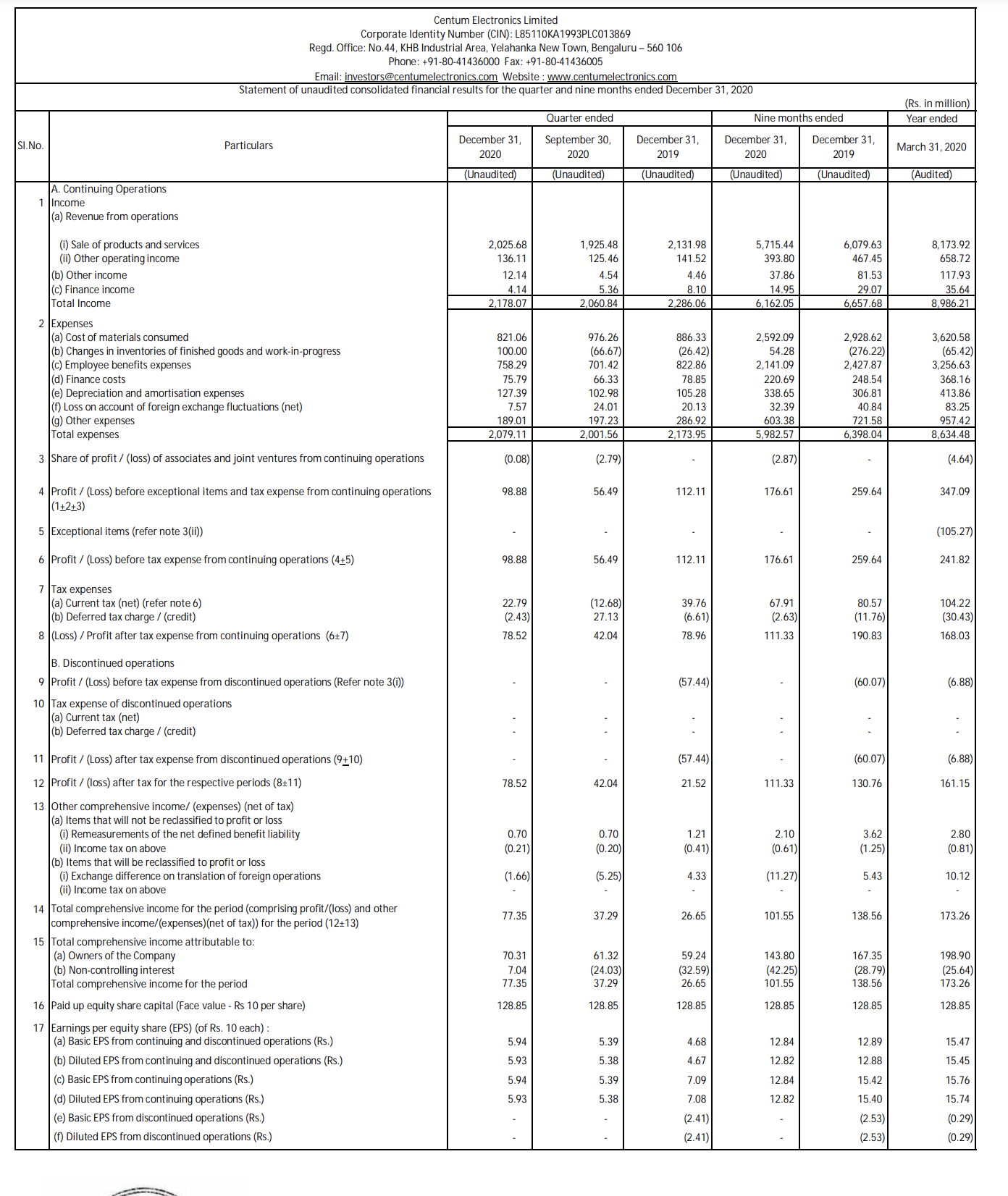

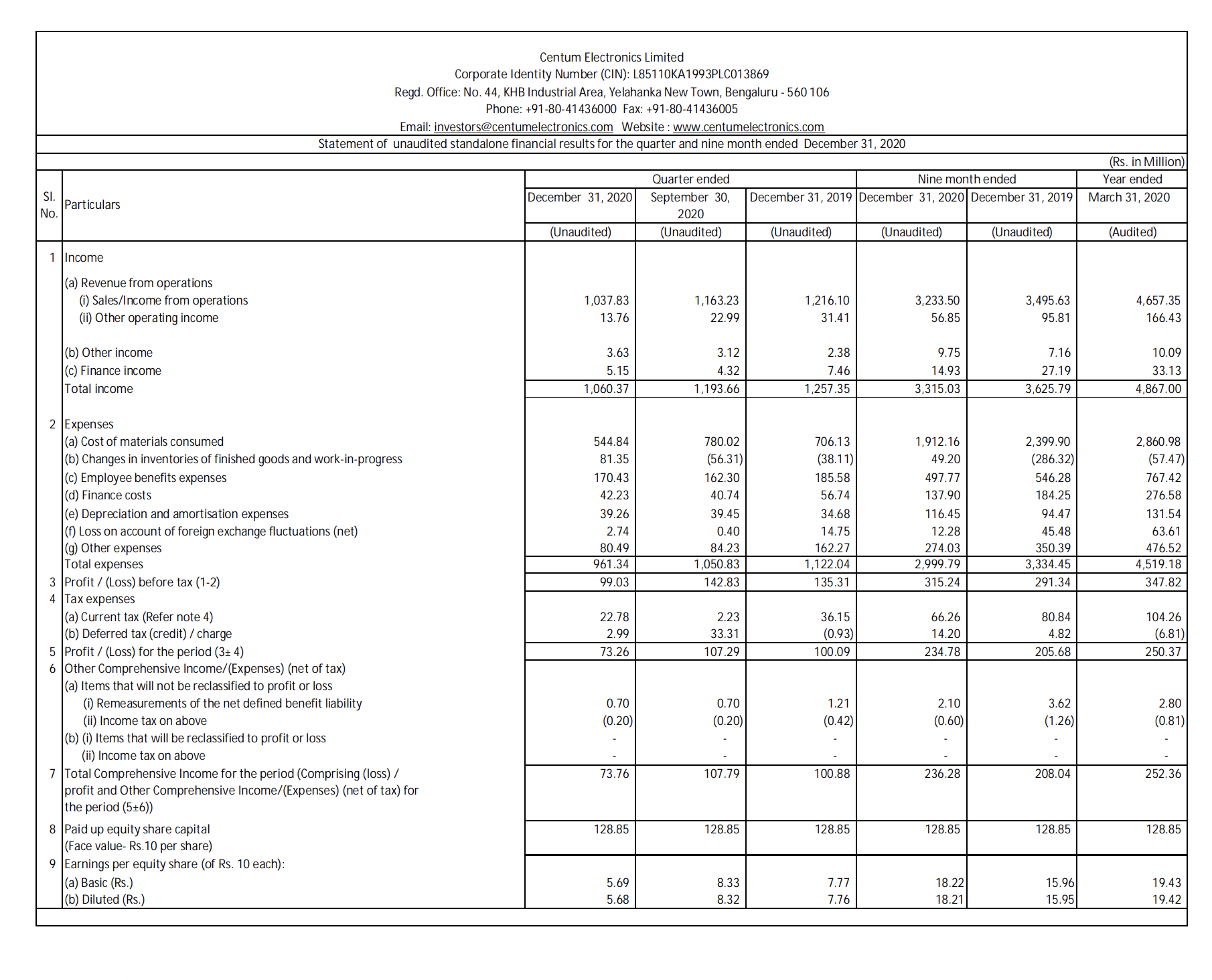

Defence projects have a very high gestation period, says Centum’s Chairman and Managing Director Apparao Mallavarapu. He spent between Rs 20 crore and Rs 25 crore in 2006 to set up capabilities for defence. It was then primarily a supplier to ISRO for its space programmes with annual revenues of about Rs 100 crore. In 2013/14, 25 per cent of Centum’s revenues have come from defence and space projects. In the nine months ending December 2013, revenues were at Rs 313.4 crore. It was 10 per cent of Rs 257.4 crore revenues in 2011/12.

Look at increase in Defence + Aerospace revenues. They have increased from 25 crores (10% of sales) to 100 crores (25% of sales) this year (annualized 3 quarter figures for 4 quarters). We currently do not know if these are high margin areas, but there definitely seem to be huge entry barriers in terms of relationships.

b) Look at this company presentation (http://www.slideshare.net/ssumantha/centum-industrial-presentation). This is no ordinary manufacturer (see their evolution). They seem to have significant IP and technology understanding.

Anyway, there are a few questions:

a) Centum’s receivables from Rakon at the end of FY13 was 43 cr. In Q2FY14, it seems to have increased to 55 cr. It seems Centum received payments from Rakon, and the current receivables stand at only 23 cr, but need to confirm this.

b) In 2012-13, Centum wrote off 11 cr bad debts (more than 1 yr of consolidated profits) - and this was all of a sudden without any provisions in the preivous years, which tells us that this was totally unanticipated (the company in culprit was Datamatics, which didn’t pay up and Centum couldn’t recover dues even after they won a court case). What is the company doing to prevent such a shocker write-off? (11 cr was more than FY13/FY12 profits of Centum)

c) Biggest clarification required: How is the management hedging deteriorating financials of Rakon? What if Rakon declares bankruptcy and sells its technology to say a Chinese players? What would be status of the joint venture, given that 35% of sales and close to 40% of operating profits comes from Centum-Rakon joint venture?

d) What is the new facility about? What is the kind of expansion and for what products? When is it expected to go operational?