Thanks @VJ_4402 and @Prdnt_investor for taking the discussion forward. I agree that they are also looking at the institutional market and adjacent market of IC through the R&G market which is largely small players in the south. Maybe organized/maybe unorganized.

I am trying to look at CCL as a call option. Where in I don’t lose much if the domestic business doesn’t fire and I will earn a lot if the domestic business does well. Thus the discussion.

Following excerpt from a recent Moneylife article on CCL Products explain the difference in profitability from B2B and B2C sales.

In FY17-18, CCL achieved revenue of around Rs1,100 crore at roughly 28,000 tonnes of volume. This comes to around Rs0.04 crore per tonne for B2B business. (Note: branded business in FY17-18 was just 2% of turnover).The cheapest variant of its branded product, Continental Strong, sells for Rs650/ kg. This comes to around Rs0.065 crore per tonne. And Continental Strong is not even a pure coffee product; it is 53% coffee and 47% chicory. Its freeze dried product, Continental Premium, sells for Rs200/50gm; i.e., Rs4,000/kg. This means a realisation of Rs0.40 crore per tonne, a 10x realisation compared to what it gets on B2B.

Nestle India launched ‘Nescafé É Smart Coffee Maker’ and is priced at INR 6,499/-. It will be interesting to see the response for this product and adoption. Currently they have very few reviews since product launched very recently.

Below are the product features from Amazon.

É by NESCAFÉ is a first of its kind, smart, app-enabled coffee maker

Pair via Bluetooth with NESCAFÉ É Connected Mug App for personalised experience

Enjoy a wide variety of indulgent coffee recipes at the touch of a button

With its heating and frothing features, É prepares great tasting coffee quickly (60-90secs) and silently

This trendy, 100% leak & spill proof mug let’s you enjoy coffee on the go, worry-free

Thermal insulation keeps your drink warm or cold in this 210ml mug

It has been very clearly mentioned on this thread that CCL as a company can completely pass on RM costs as they work on fixed $$ margin. So all these vagaries of crop cycle does not affect the company. Also the management has clarified that it has ability to procure green coffee from all important places in the world. So unless there is like “end of the world shortage” of coffee, none of these events matter for CCL’s EBITDA or PAT.

Also company says they have natural hedge with respect to rupee depreciation as they buy raw materials in dollar and sell products in dollar - Source Q1 FY19 Concall

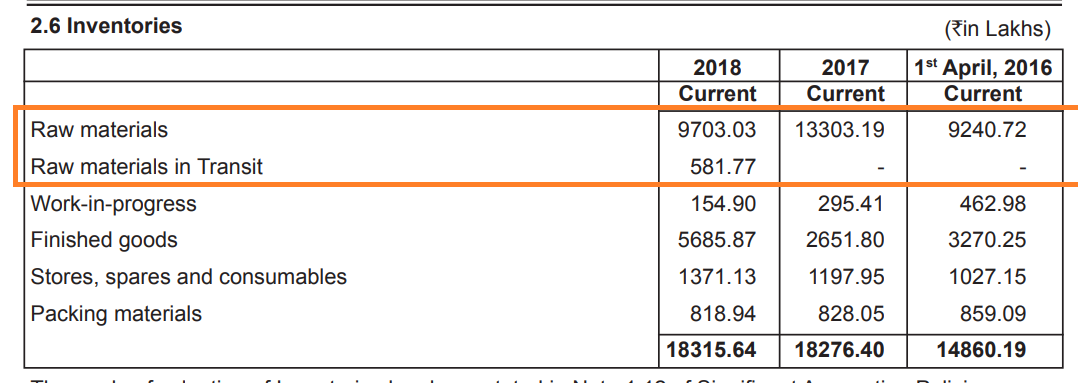

With lot of indepth discussion done about CCL products, No one has checked on CCL’s working capital which seems very stretched both on standalone and consolidated basis. Wc is close to 1/3 rd to 1/4th of net sales. That WC turnover ratio is too low for a company like CCL.

What has made the receivables so very high compared to payables?

If anyone has studied this, do share about WC and why receivable being significantly higher than payables?

Taking a snapshot from Edelweiss report shared above, the working capital looks absolutely normal. Debtors days are ~50. With overall cash conversion cycle of ~140-150 days. Nothing to be concerned.

It just that it supplies to B2B the debtor days looks higher than payable days. Upto 90 days credit cycle is normal in my view.

I would take some of this with a pinch of salt @rupeshtatiya . Raw material sourcing always has a location component. For example - they would probably set band wise price revision targets in their contracts based on global coffee prices. (X% increase for every y% increase in green coffee). However, in reality some of their supplies would be from nearby location where plants are based , some through longer term contracts et al … and therefore, the situation may be a tad nuanced.

Particularly, floods in India would have impacted some of their sourcing costs to the tune of 5 - 7% assuming 20-30% of the raw coffee coming from outside INdia

My understanding is as follows -

CCL goes into contract negotiations based on quantity & I am not sure there are long term contracts like - 5/10 years. They use current market price of green coffee during contract negotiation & the moment contract is finalized, they place orders with green coffee producers.

As said in one of the conf call, almost 50% of the capacity for next financial year gets booked in December of current financial year. This consciously protects them against any coffee price variations & protects their margins in $$/T basis but maybe they take a hit in working capital due to higher inventory days.

The only scenario in which RM costs might impact margins is if green coffee producer is not able provide green coffee due to some special circumstances (like natural calamities etc.) but that would be an one-off event.

That’s fine. My point was about backward linkage. They don’t produce their own coffee beans. And when they buy, I’m sure there may be variations in sourcing locally with lower transportation costs or sourcing from better yield varieties versus what they may have planned.

Launched Malgudi and other similar brands in INdia

Reaching optimal capactiy in Vietnam. Doing de-bottleknecking to get some more capacity ~3500 tonnes (will cost 8m USD)

Raw material, coffee prices declining; Business doesn’t impact from raw material prices (only margins seems higher due to this); Per KG realization is still the same

Utilization levels: 1H >> India 90-95%; Vietnam 75-80% (target this year)

Maintenance shutdown completed (for 20 days)

Private labels: Local ads in south (TN, Kannada, Telugu) is being targeted; Not targetign North since filter coffee consumption is very low

Setting aglomeration (5000 tonnes) and packing (300-5000 tonnes) plant next year; Spending around 12m USD Land is already purchased; Value addition/automated packing line; Outside SEZ; Can be incremental realization of ~5% due to this

INR depreciation >> Natural hedge; 30% is open

Multiple advantage giving us competitive edge: Old plant, economies of scale etc.

Freeze dried plant: Not yet declared the commercial operation; On CWIP under BS

Export incentive: 21 cr in 1H

If volume picks up for few targeted customer then more capex after 3 years will be planned

180cr is loan component out of 360 cr.

PAT guidance 15-20% growth next year

India duopoly: competition from Nescafe and BRU

Adding 10-15 customers every year; major volume would be coming from 3-4 out of this; Existing clients also keep increasing volume with us

Aglomeration demand increasing: COntinental Extra has been introduced, there is volume demand for this (main reason); Other export customers also having this demand (earlier was being done by re-sellers to some extent); Nesle doing all in aglomerated; Perceived as better and premium (have better look, aroma etc.)

B2C offers are being phased out, these are introductory offers; Also getting revised

Blends increased to 1000+ (many permutations are possible); No product that we cannot produce; Capable to produce any product similar to other product in world

Tax holiday in Vietnam extended (every year need to apply, haven’t given deadline yet)

No debt being raised for incremental capex currently; All from interal accruals