I hold that stock close to a year and every time listened good commentary from management. Eventually excited with Q3 result as I was not able to see any reasonable growth.

@AmarP Hi, What is your defination of reasonable growth?

Total income for 9MFY25 grew by 24%.

Last 3 and 5 years growth is 30% and 22% respectively.

Current PE is 24.6.

Disc: Invested since long, added in last 2 days. Views are biased.

5 Likes

Hi Deven,

for me the rate of EPS growth along with other opportunities available in the market at a better growth rate matters hence the sale & switch. It’s totally a personal preference.

Dec 21 EPS was 6.47 and Dec 2024 EPS is 4.40 INR.

2 Likes

You are right, they are majorly B2B players, but even in B2B segment if they are maintaining 18% margins means they have some good power.

They are supplying to major brands and dealers.

They are trying to diversify some portion to B2C in coming days.

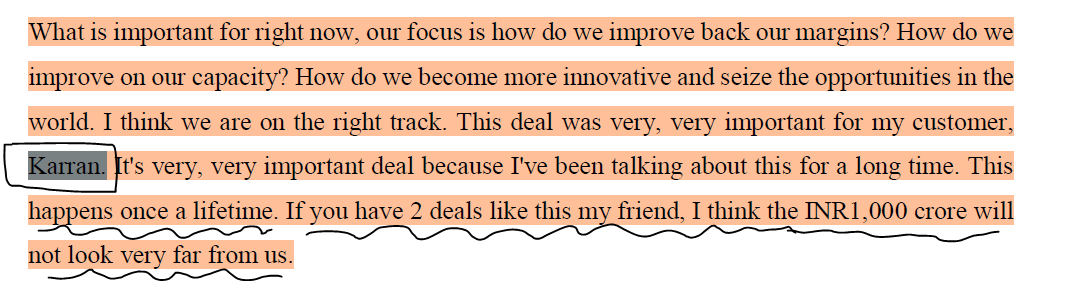

Management told that they can’t hit the 1000Cr mark in FY25, they may end up around ~820-830 Cr. Discussed about one big order from US brand, which can boost the sales by Q4 end & FY26 also. Margins will be back to 18% in Q4 as US subsidiary losses will decrease in Q4 & softening of freight charges.

Company can grow at 20% rate going forward, its available at < 25 PE of FY25 now (considering 25 EPS with 18% margins). I feel valuation’s are very attractive now and we can expect entry of institutions also at this price. I am not expecting any more correction going forward as its already fell > 50% from the ATH.

8 Likes

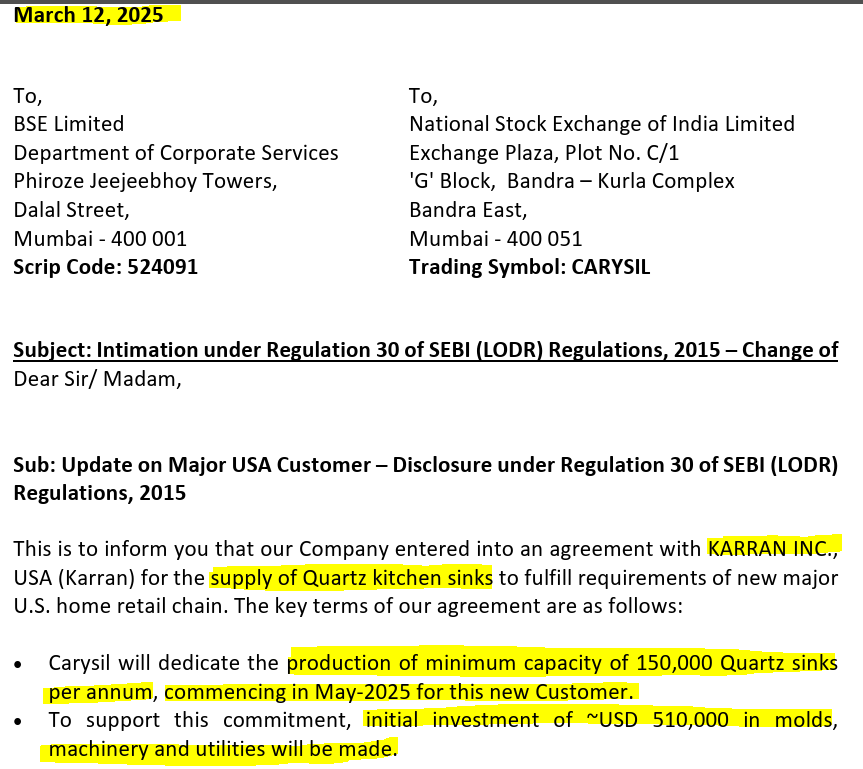

Carysil Enters Agreement with KARRAN INC., USA for Quartz Sink Supply to Major U.S. Retail Chain

This what Management had said in the latest concall.

Sources: Latest intimation to SEBI & latest concall Transcript.

8 Likes

What is the duration of this deal?

Update filed with the exchanges just seems to give the headlines without the fine lines

Its clearly mentioned that 150k sinks per annum ~85 Cr.

I think with addition of new SKU for IEKA & this deal they can hit 1000 Cr mark easily FY26

2 Likes

Where do we see how much worth is ths 1.5 lakh sink

I saw one here at this furniture store. The Carysil sinks were set in a separate aisle surrounded by cooking ranges and microwaves. The sinks looked good. Nothing epic.

1 Like

FY24 revenue was 684cr. Of this 52% came from Quartz sink. So roughly, 356cr. And quartz volume for FY24 were 564,300 So, per sink revenue is 6,300. Assuming some discount on large order, price should be around 5800-6000 for Karran.

For 150,000 sinks it would result in 87cr based on 5800 per piece price

9 Likes

Things are panning out very well, accumulated some shares around 500. Value left on the table is completed with the recent 30-40% move.

1 Like

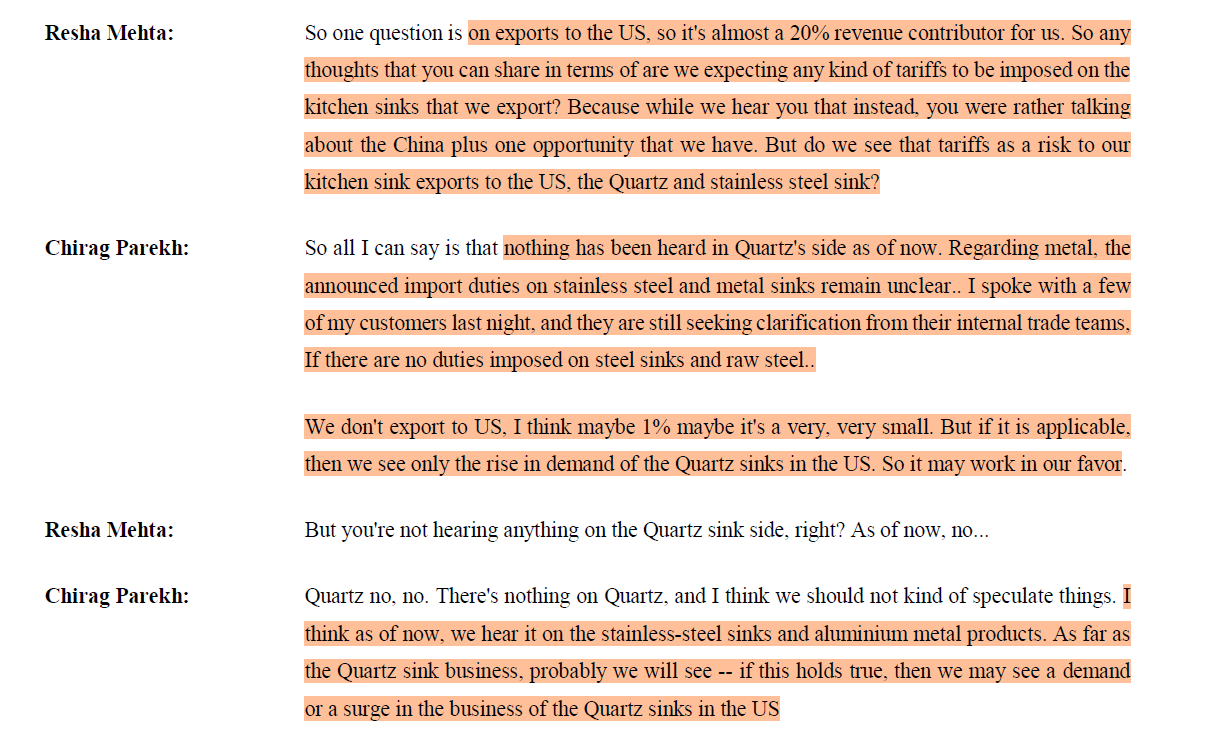

Has anyone assessed the potential impact of recent reciprocal tariffs between the U.S. and India on Carysil’s profitability, especially given that quartz sinks are a major revenue driver? Could increased tariffs affect export volumes or margins?

As the company’s performance is closely tied to the U.S. market, where reciprocal tariffs could impact profitability

- Carysil plans to invest Rs 500 crore to expand its kitchen solutions manufacturing in India. The company aims to establish Bhavnagar as a major global kitchen sink manufacturing hub.

- Rs 100 crore will double sink manufacturing capacity from 1 million to 2 million units annually.

- Rs 50 crore will increase stainless steel sink production to 2.5 lakh units per year.

- Rs 30 crore will boost kitchen faucet production to 50,000 units annually.

- Rs 20 crore will support the manufacturing of 50,000 built-in kitchen appliances per year.

Source: https://www.dailyexcelsior.com/carysil-to-invest-rs-500-cr-to-hike-production-capacity/

Management clarified that they have invested 300 cr since 2020 and looking to invest 200 cr more in next few years

Source: https://www.bseindia.com/xml-data/corpfiling/AttachLive/321856ec-616a-4c50-824b-a89cdad2d807.pdf

2 Likes

Carysil’s management, represented by Chirag Parekh, clarified in their concall that they haven’t heard of any imminent tariffs on quartz sinks exported to the U.S. at that time. While there is uncertainty surrounding the potential tariffs on stainless steel sinks, the company’s export volumes in this area are minimal, with only about 1% of sales being impacted by U.S. imports of stainless steel sinks.

On the quartz sink side, no tariff imposition has been mentioned, and management believes that, if such tariffs are imposed on metal products, it could even work in favor of their quartz sink exports due to rising demand.

Regarding the broader question of U.S.-India trade relations, it’s worth noting that discussions between the two countries are ongoing, and it’s not certain that President Trump will push for reciprocal tariffs on India, as these policies can change frequently. It’s difficult to predict, given Trump’s tendency to make unpredictable trade decisions—one day imposing tariffs, the next backing off.

Sources:

3 Likes