Carysil Ltd -

Q1 concall and results highlights -

Revenues - 201 vs 141 cr, up 41 pc

EBITDA - 37 vs 27 cr, up 37 pc ( slight dip in EBITDA margins due ongoing Red Sea issues and costs related to integration of their US subsidiary - United Granite )

PAT - 16 vs 12 cr, up 33 pc

Quartz Sinks capacity utilisation stood at 70 pc

The contract with Reece Australia and Howdens UK are progressing well ( these should bump up company’s revenues going fwd )

Exploring new Mkts like - Turkey, Croatia, Vietnam for Quartz sinks business

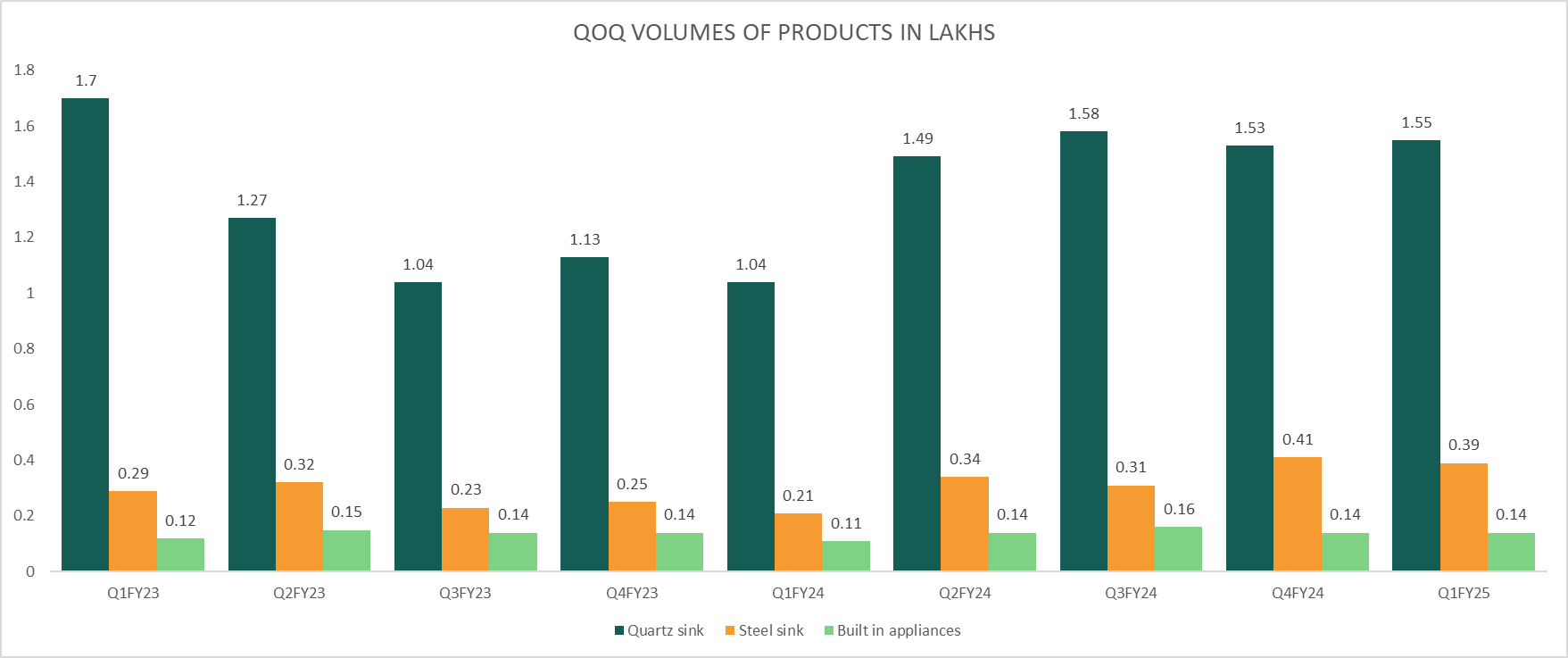

Volumes sold in Q1 -

Quartz Sinks @ 1.55 lakh vs FY24’s Qtly avg of 1.41 lakh

Steel Sinks @ 0.37 lakh vs FY 24’s Qtly avg of 0.31 lakh

Kitchen appliances @ 0.14 lakh vs FY24’s Qtly avg of 0.137 lakh

Export : Domestic sales breakup @ 82:18 vs 80:20 in last FY

Product wise sales break up -

Quartz sinks - 45 vs 52 pc

Steel sinks - 11 vs 13 pc

Solid surfaces - 32 vs 25 pc

Appliances - 11 vs 11 pc

Revenues from overseas subsidiaries -

Carysil Products UK - 31 cr ( selling steel and Quartz sinks )

Carysil Surfaces UK - 42 cr ( selling solid kitchen surfaces )

United Granite US - 21 cr ( selling solid kitchen surfaces )

Recently concluded a QIP of 125 cr. This amount shall be utilised for acquiring new moulds for Quartz sinks, expanding appliance and faucets manufacturing capacity and for brand building in local mkts

Company expects their Qtly revenues to improve going into Q2,Q3,Q4 ( vs the 200 cr clocked in Q1 ) - subject to no major geo-political disruptions

In Q1, domestic sales have grown by 16 pc YoY

If the Red Sea issue doesn’t worsen further, company’s margins should see an upward trajectory going forward

Management believes that Quartz Sinks business has a long growth runway ahead ( globally ) and the company is extremely well positioned to benefit from the same

This year, the company is expected to do 150 cr of sales from India. Aim to do 300 cr / yr of sales from India Mkt within next 4 yrs

Disc: hold a small tracking position, biased, not SEBI registered, not a buy / sell recommendation