As per Acrysil Limited's Chirag Parekh Speaks On The Firm's FY23 Business Outlook | Chartbusters - YouTube

IKEA share of overall revenue is in the range of 10 to 20%. They can’t share the exact numbers due to NDA with them but the interviewer was clever enough to still get some rough figure. ![]()

Considering 15% it would be around 75 Crs which they expect to grow even further.

3 Likes

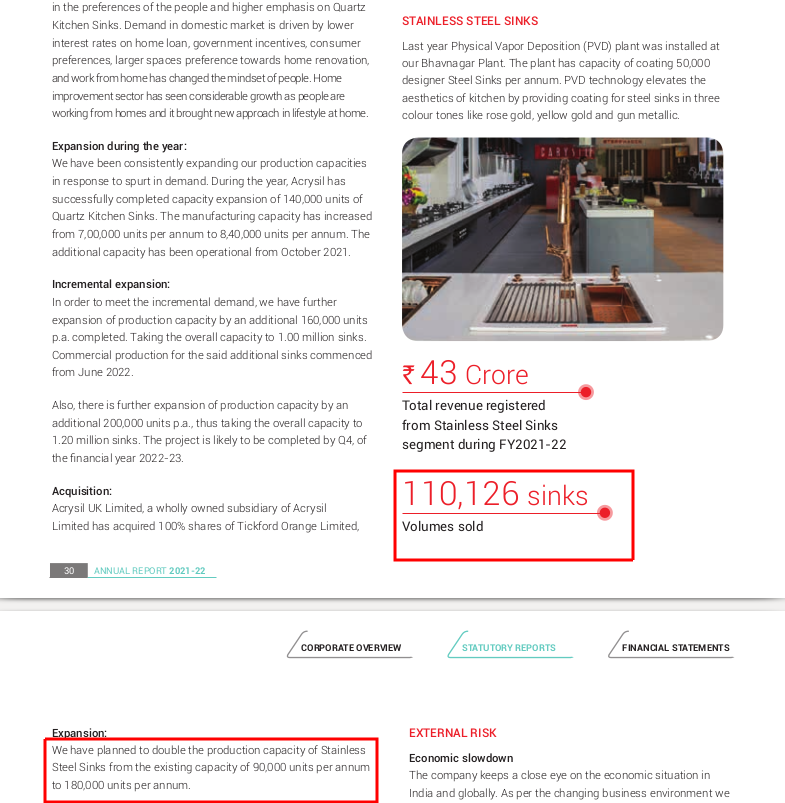

I was going through the annual report of Acrysil and found that they have sold more stainless steel sinks than the capacity they have. ![]()

Can we trust this management?

4 Likes

Well The difference is 18%, assuming the utilization rate was 100% (100% really? maybe). So, the extra amount could be some more sales from the existing stock (inventory/safety stock) or may be they have some capacity with 3rd party manufacturer or subcontractor.

Can’t say anything w/o doubt, could not find any information on this.

4 Likes

Check this.

Expansion plan is Bigger Picture or By what year they will expand while in phases they keep on adding the capacities and utilize it as soon as they are ready.

In This Particular case by Q4 FY22 was estimated when capacities will be ready for commercial use.

Poor results on both QoQ and YoY basis.

1 Like

I would give them some leeway due to inventory pile up and a slump in current conditions. However, in my research, it appears that their customer service is abysmal. You can see the reviews in amazon, facebook and in google maps. Without fixing this, they wont be able to scale up sustainably.

If anyone is attending today’s earnings call, can you please ask why customer support is poor for last 3 years and what steps they are taking to address this?

4 Likes

Rather than decrease in net profit, I was disappointed by,

a) Shelving/postpone of capex for Quartz sinks. That means revenue and earnings goings ahead will be muted.

b) Management’s obsession with diworsifications.

Board has decided to utilize the capex amounts and resources allocated for quartz sinks facility towards setting up a plant of 200,000 units p.a. for manufacturing of built-in kitchen appliances. This will entail the company to reduce its dependence on imports and become self-reliant.

They keep venturing in other products categories instead of realizing full potential of main bread and butter product.

c) Debt has increased significantly compared to March 2022. I am not sure whether this was on account of takeover of SIL.

3 Likes

Well, atleast the diversification is into kitchen and bath related things and not into a completely different unrelated segment…

1 Like

Few positives that i could find in the investor presentation

-Domestic business has increased by ~58%

-the overall capacity of quartz sinks stands at 1,000,000 sinks

-The Company is doubling production capacity of stainless steel sink from the

90,000 units p.a to 180,000 units p.a

-Company Increased dealer network in domestic market from 1500 to 2,200 dealers

during H1 FY23 and plans to increase by ~3,000 by end of FY23

-Developed new type of sinks which will have strength that is twice of existing sinks

without any increase in manufacturing costs

-Received orders from France for new PVD sinks & under mount

sinks models, which will be a great opportunity in export market

5 Likes

My reading of the call

Focus till now was on export. Management has realised potential that domestic market can offer and thus increase in dealer network.

Business has slowed in global market but performance may bounce back after 2 quarters and then may grow from there.

Good part is they are selling new products to same.customer . They can’t sell more of sinks so might as well sell faucet and top.

This thesis may not playout in next 3-6 months . This could be a good to look at from 3-5 year view. By that time global market may settle down and also other triggers may start playing out ( domestic market ) .

Some time diworsification can help to find a much more scalable line of business.

It’s good to try to grow buisness then to say global factors are spoiling the party.

Right Efforts help buisness scale over a period of time .

Biased views are personal.

Hold stock in portfolio.

6 Likes

IMHO, don’t think diversifying from sinks to kitchen appliances is diworsification… don’t think TAM and replacement market for quartz sinks in itself a big market… selling 600k/ 4m schock technology sinks… capacity to go upto 1m/ 4m sinks…

they are already cross selling with faucet + top, so adding a related area of appliances is a good move to capture the entire kitchen space…

More concerned about the sanitary business diworsification, beyond faucet and bath sinks…

4 Likes

CapEx and acquisition of subsidiary has resulted in increase in goodwill and borrowings. ROE and ROCE expected to have some pressures unless capacity utilization goes up.

3 Likes

Not just the capacity utilization, right? The newly acquired subsidiary will contribute to around 20 percent of the revenue i guess, so that should help with the ROCE?

What is the Acquisation your Mentioning? And how much topline we can expect in the next quarter?

They recently acquired Tickford Orange Ltd and its Subsidiary Sylmar Technology.They manufacture solid surfaces for Kitchen and bathrooms.

I think this their website www.sylmarsolidsurfaces.com

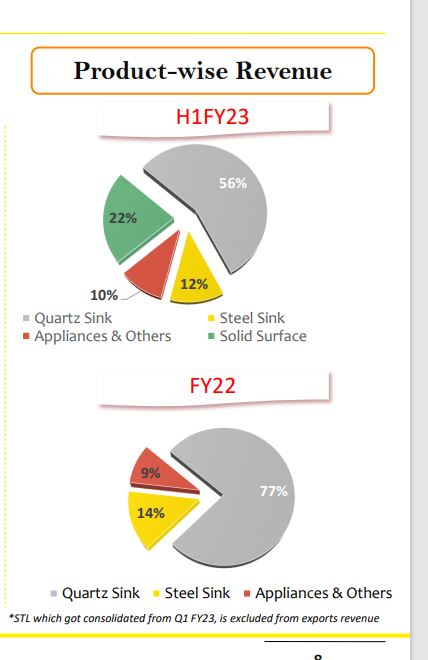

Regarding the topline…i cant remember the exact number , It was mentioned in the conf call in August i think. But here is the revenue breakdown from their recent investor presentaion

So the solid surfaces are set to contribute 22 % to the topline from fy23

3 Likes

I have a different opinion on product line expansion. As someone who has been in startup world businesses do not have a lot of luxury to present your approach in the most articulate and strategic manner. Sometimes you just try few new things and see what works. You drive your core business but you also try to see other avenues of growth.

Here i do see some sense in the way management is thinking. They are targeting the kitchen setup budget that the home owners have while building their house. They have a broad sum of money which they spend on sinks, hobs, ovens and other appliances. Generally this spending is done together so it makes sense to target this consumer need occasion. If you have the distribution strength and a brand you can leverage your association with overseas partners to expand your share of the kitchen budget pie. Bathroom sinks are also is an extension of this and probably a more immediate opportunity as product is much more similar to existing core portfolio. My feeling is that some things will work and some will not. Things like Oven and Dishwashers have strong established brands and it is easy to choose their products. There is also a strong after sales service and trust required in these products so are much harder to break this market. But sometimes decisions are made by architects or builders who may see some incentives in buying the bundle and that maybe and entry point for management.

I think company also would be aware of their strengths and weaknesses and in some cases it could be a distribution partner and be more of a trading channel for some newly launched international brand in some of these categories.

It would be interesting to see how it plays out and finally the proof will be in the execution over long term. Right now this will not move the needle on the performance but will come to play over a longer term time horizon.

Disclosure: Invested

13 Likes

If anyone has info on: Do they have higher margin for export or domestic?

Am asking as, as per latest concall - they will be 50-50 split between domestic and export in coming years.

Thanks

In domestic they sell the products in their own brand name “carysil” while in exports it’s mainly white label sales.

Selling in own brand requires tough field work on terms of establishing robust dealer network and constantly training, hand holding them. It Requires targeted advertisement (digital, physical).

Once you do this, you enjoy decent margin and regular sales.

2 Likes

Changing company name and ticker is not a major concern as it is still inline with their focus on brand building and expanding on domestic market. If the mgmt does some other crazy thing to shore up share price, that would be a serious red flag compared to this.

2 Likes

Notes from November concall:

- Higher inventory buildup by sales channel previously. This should get liquidated by Q4 next year.

- Doubled supply to IKEA and sales to Grohe is increasing year-on-year basis.

- Board has decided to postpone the expansion of an additional 200,000 capacity of Quartz Sinks.

- 3 million to 4 million sinks are being manufactured in the EU area around Germany

and Italy. Due to EU energy crisis and rise in manufacturing cost of EU companies. Acrysil will look to enter the market. - For H1 FY2023, domestic revenues have increased by 58% Y-o-Y to Rs.71 Crores. We

aim to achieve a turnover of Rs.300 Crores(annually) in the domestic market in the next two to three years. - Lower margins this quarter due to standalone sales being down by 12%

- EBITDA margin will return to the normal level once sales normalize. Ideally post Q4.

- Debt on the balance sheet to increase from 130Crs to 150-155Crs by next financial year.

- Have entered into built in appliances and expects margin profile to be better than quartz sinks.

- Long term India versus export revenue will be about 50%:50% from current 29-71%.

- Management targeting sales of 1000Crs by next 2-3 years.

12 Likes