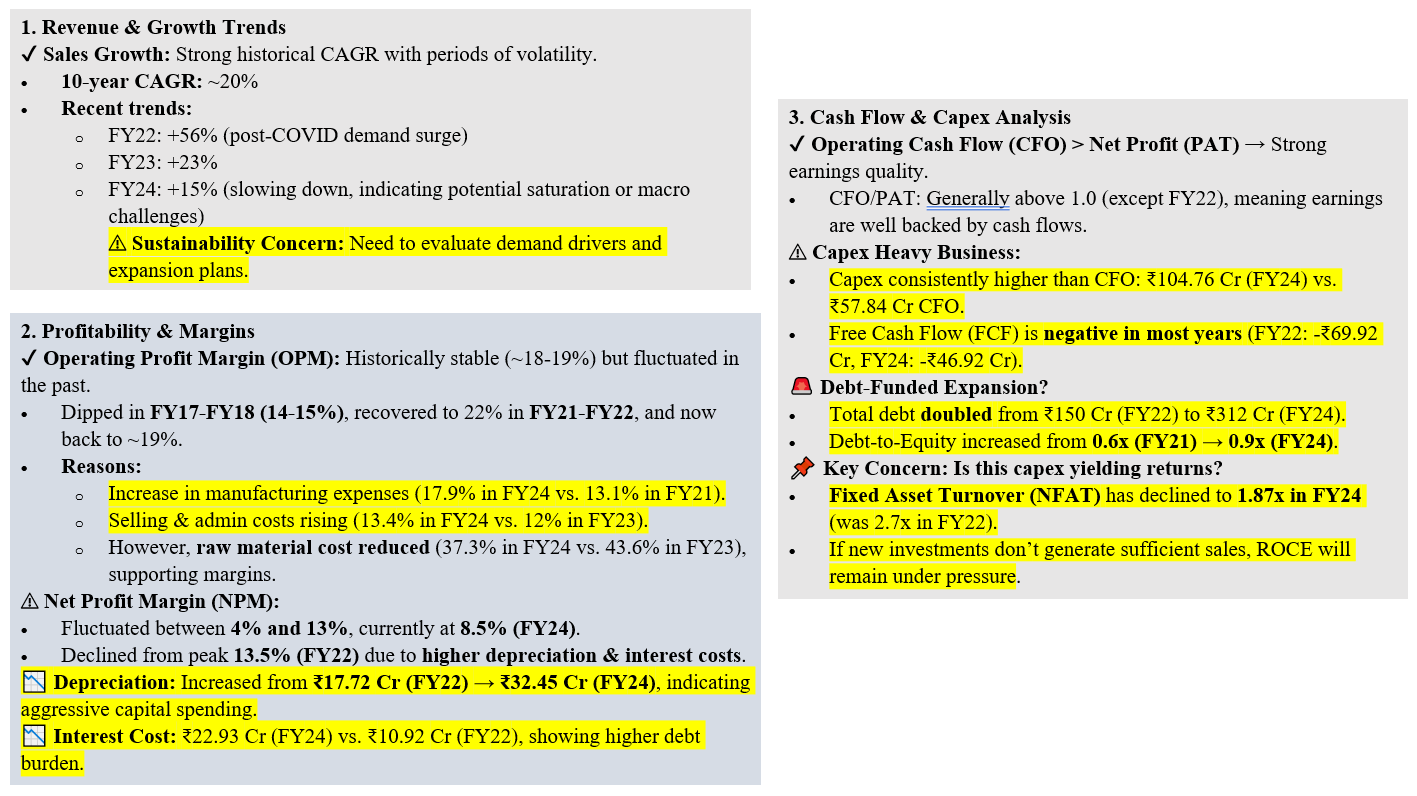

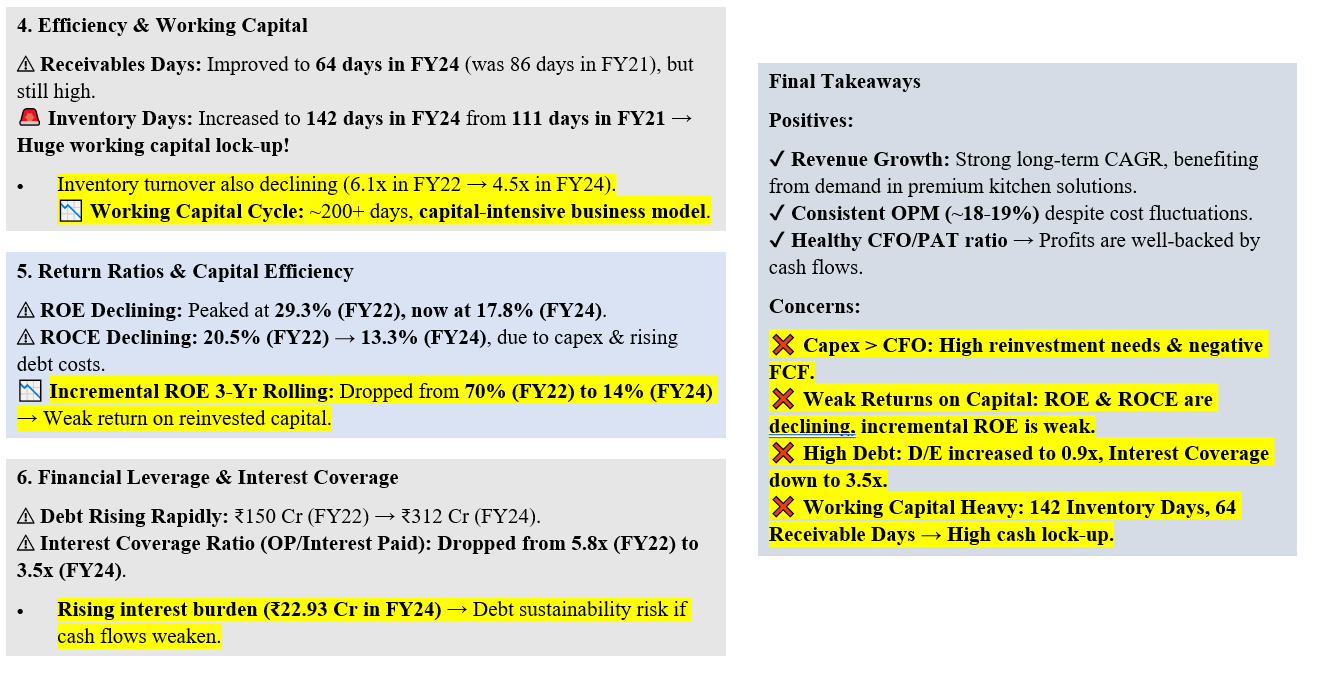

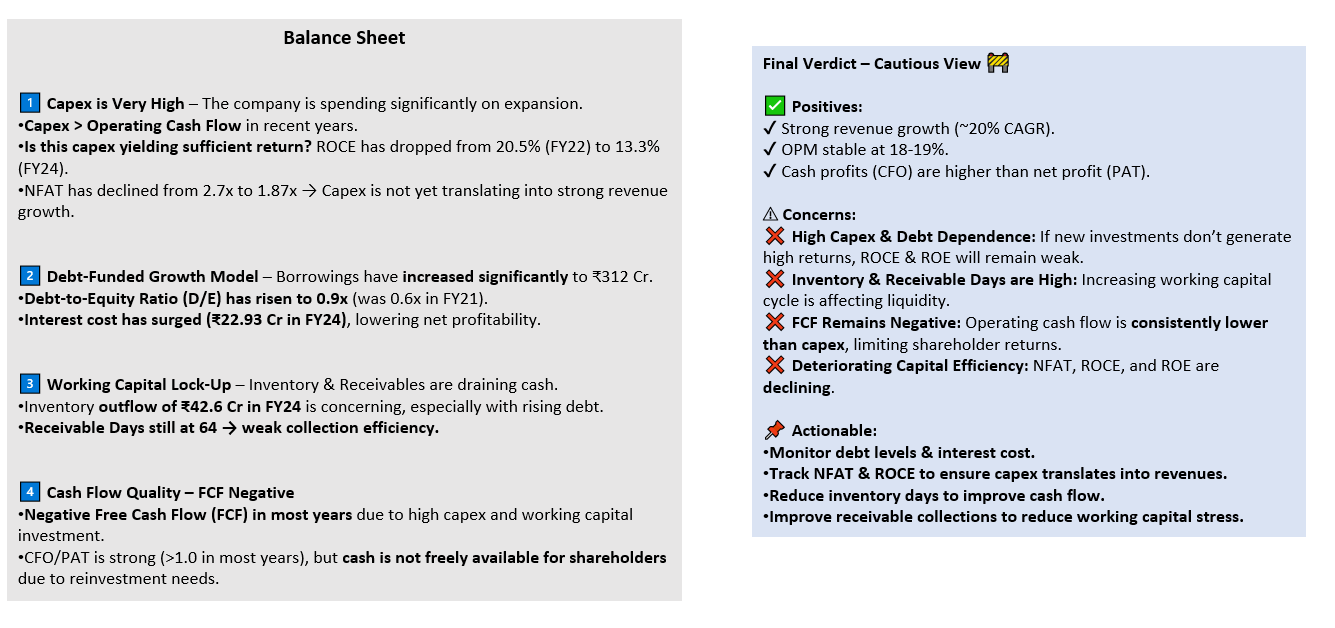

Carysil Ltd has shown strong revenue growth (~20% CAGR) with stable OPM (~18-19%), but its aggressive capex and rising debt (₹312 Cr in FY24, D/E 0.9x) are concerning.

While sales have grown, fixed asset turnover (NFAT 1.87x) and ROCE (13.3%) are declining, indicating inefficient capital deployment.

Negative free cash flow (FCF), increasing working capital cycle (142 inventory days), and high interest costs (₹22.93 Cr in FY24) add financial strain.

The company must ensure its expansion yields strong returns; otherwise, it risks profitability pressure and liquidity stress.