You highlighted all the reasons to buy the stock otherwise when will you buy ?

When profit growth is 25% CAGR for 5 years and Margins are all time high ?

the business depends on Corp Debt cycle which have been grinding since 2009 financial crisis and seemed to have bottomed out hence rating agencies should do good going forward whenever the cycle revives - This blog explained very well in this blog

I second your point. I think the market is still overlooking the potential of CARE going forward in a high capex, high credit offtake kind of environment.

PSBs haven’t been lending & corporates haven’t been borrowing since the profit cycle had yet to pick up. And now there are definite signs of earnings growth.

Plus NCLT resolutions are picking up pace & with fresh recapitalisation, PSBs balance sheets should become healthy enough to lend again.

All this focus on further improving “Ease of Doing Business” in the country, bond market reforms bodes well for CRAs.

The only truant will be further rate hikes by RBI which will push up the borrowing costs for corporates. But if the economy is strong & earnings growth remains strong, that won’t be a problem.

Perhaps corporates could wait for the election cycle to be complete to remove political uncertainty as well before carrying out fresh capex.

Just now I was reading RBI board meet statement which said RBI will take steps to ease liquidity for financial sector (reduce reserve requirements?) and increase credit to MSMEs.

My take of the credit rating industry and the top 3 after going through the RHP of care and other documents.

CONS

interest rate up cycle is bad for CRA as rating revenue fall.

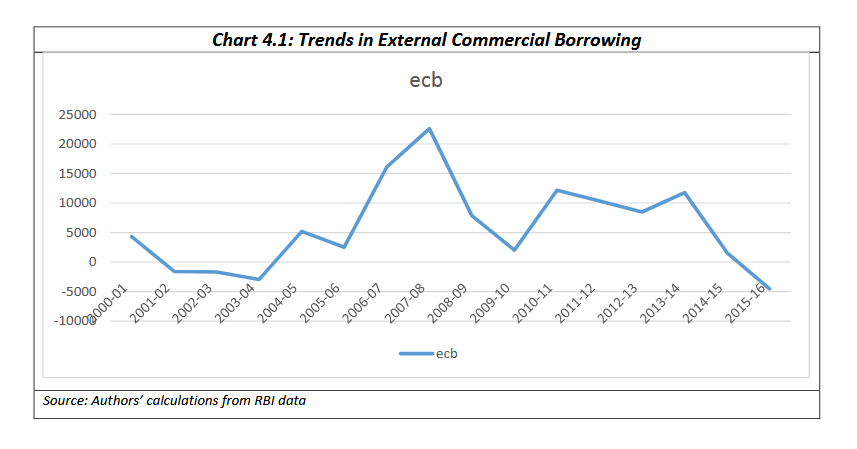

ECB is bad news. NBFC has started using this route for a start.

Indian bond market is very shallow and only AAA rating is feasible. even with this bankruptcy rule,don’t know how the holders will be repaid.

earnings growth has tapered down drastically. opportunity cost as investors need to be taken into consideration. y to invest in low growth companies when u have high growth co? or say a FD/bond rated by CRA

PROS

They are here to stay.just like auditors we need them and there are 3 CRA which control 85% of the business.

Asset light business model.

So to invest here we need to get best price for the business by which we nullify the low growth in sales.

To compare an investment made by Radhakishan Damani in VST industry in 2008-09. He invested in VST knowing it is in a slow growth industry but a solid co. Dividend payout was 70% and now most of his investment is coming as dividend.

so,the only way investing here is to get it dirt cheap during the interest rate upcycle (we have good time to buy this sector slowly).

Interest rates have come down from 2012 to 2017.

However, the Stock or business hasn’t done well when interest rates have gone down. It was at 950 in end 2012 and today almost at same price. 5-6 years of no returns despite the fact that revenues have almost doubled in same period.

Why has that happened?

The other key company of this sector - Crisil has show similar trend. Almost similar revenue and profit cagr from 2012- till date.

Why?

Crisil did very well from 2004-2010. Why?

2004-2010 was period of rising interest rate. Then why did crisil did well from 2004-10 and not so well (same as care) from 2012-2017 despite falling interest rate.

Guess, that’s because real core economic growth and Capex phase was from 2003-10 and the same has been very weak for past 5 years.

They both can do very well in Capex phase again irrespective of interest rates.

And with crude crashing, inflation expectation is now 2.8% or so.

One can raise whatever concerns the truth is monitoring is required and thats the play for auditors in company financials and rating agencies in credit,

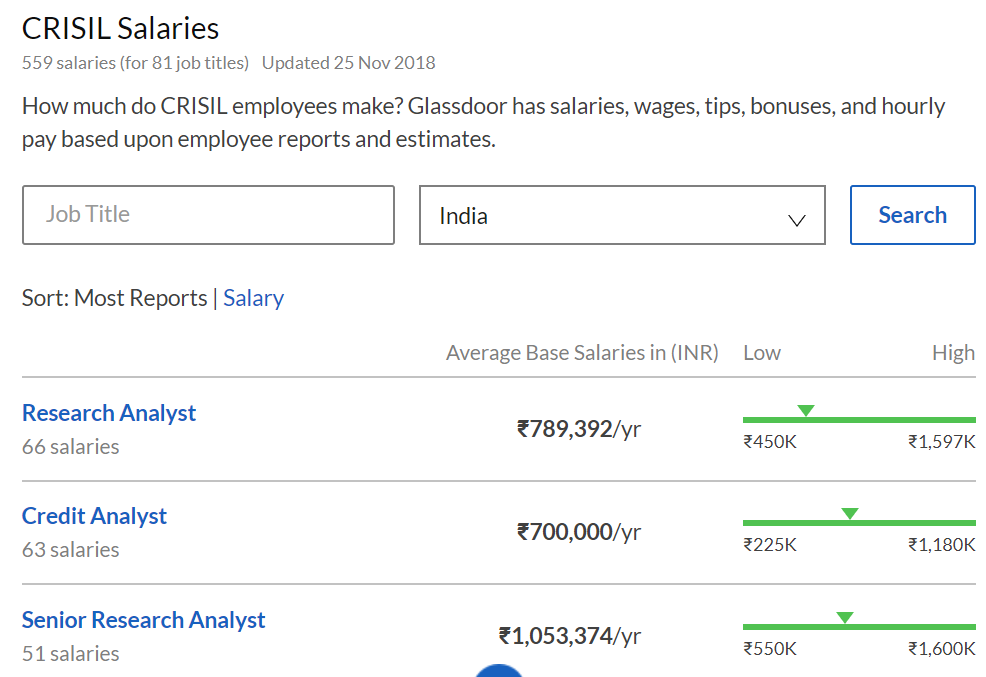

I was glancing through the financials of Care and comparing it with Crisil. It seems that high margin in Care is majorly because of lower employee cost. I did some number crunching. Found out that the employee cost per employee at Care is about half that of Crisil.

Does this mean that Care isn’t hiring quality employees? Few of my friends working in rating agencies also testified this to be true. This is one of the important concerns I had about the company. Does anyone have any insights on this?

The market regulator has specified that mutual funds have to buy only highly rated paper. So, how did the fund companies manage it? With pliant rating agencies, this is no problem. The ratings have been rated AAA by the same ratings agency, CARE, which also rated the Rana Kapoor’s structure as AAA. Commenting on this a very high net worth investor says “ratings is the biggest scandal going.”

Few points I am putting, to rationalize how even the more proven in business perceive CARE.

CRISIL brought close to 10% in CARE.

CARE from inception to today is continuously increasing market share.

CARE is pure rating play so they can anytime venture into data driven analytics etc and hence that growth trigger can come anytime in case they want. CRISIL / ICRA has multiple business line.

Mohnish Pabrai known to play investment with “Heads I win and TAILs I don’t lose much” is invested in CARE and CARE is exactly the same investment thesis.

We know at times Companies default and manipulate financial statements still AUDITORS are required and will be required similarly these rating agencies would always be rating bonds, NCDs and BLR irrespective of outcome.

SEBI is continuously making effort to broaden the BOND market and starting April 2019 they have fresh guidelines on minimum 25% of money for AA and above rated bonds from market.

While rating them AAA, CARE has argued that rating assigned to the Non-Convertible Debentures (NCDs) of WGCL are due to the credit enhancement in the form of a pledge of Optionally Convertible Debentures (OCDs) and Compulsorily Convertible Debentures (CCD) issued by DAIPL and DIL respectively (both being 100% subsidiary of DHFL). Also, an unconditional and irrevocable revolving DSRA (Debt Service Reserve Account) guarantee and an unconditional put option has been issued by DHFL in favor of the debentures.

Care’s AAA ratings are based on guarantees from DHFL’s subsidiary companies. It looks highly likely that the ratings will be revised downwards. Although please note, DHFL has no history of defaults so far.

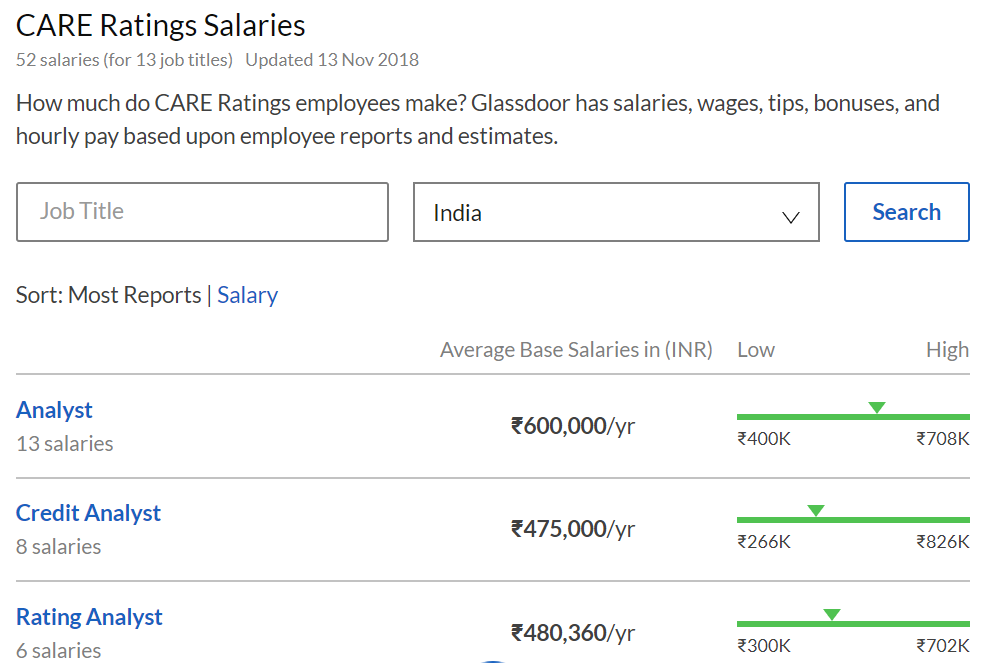

Revenue per employee for any company can be high if it pays less to its employees. The thing to check here should be employee attrition, work culture, etc. I don’t understand why Care employees should stick around for long if their Crisil counterparts earn higher. It would be great if we could use our contacts to get a perspective on how employees of Care and Crisil view their companies respectively.

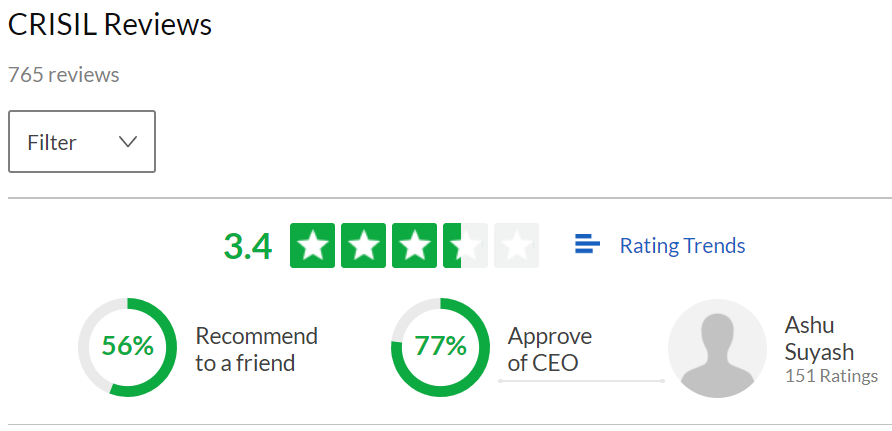

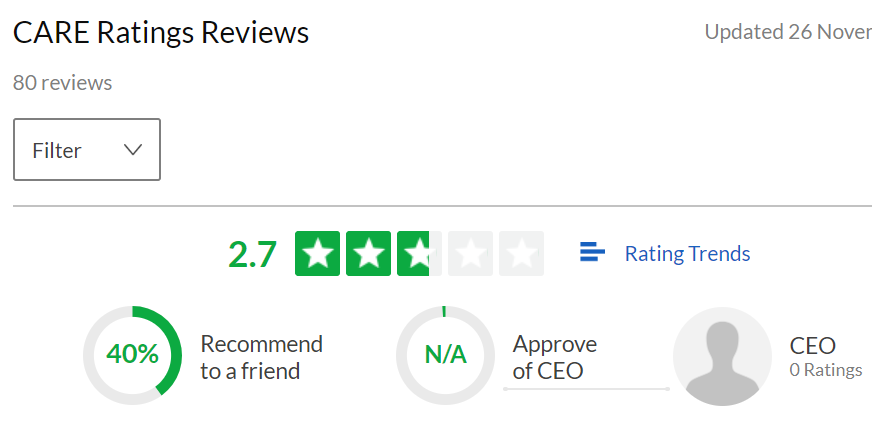

In the mean time, just a high level comparison of Glassdoor ratings and salaries: Crisil: