The journey of this company (CAPLIN Point, henceforth referred to as CAPLIN) has been very different from most of its Indian peers. The company’s major business (90% of sales) is selling formulations in frontier markets of Latin America which are collectively referred to as Central America. The region includes small countries such as Guatemala, Nicaragua, Ecuador, El Salvador, Honduras, and the Dominican Republic. Collectively, this region has a population about the population of the state of Tamil Nadu (~65mn people). The first-generation promoter and founder, CC Paarthipan, started his journey in these markets after realizing that they were underserved with hardly any presence of large, organized pharma companies. These markets were serviced by large importers and distributors who imported from other countries and sold locally at higher prices, constraining access. This also led to a high element of counterfeit and poor-quality drugs being sold.

CAPLIN slowly built this business by supplying quality and essential medicines (90% of what they supplied in the early years were on the WHO list) and at the lowest possible prices (build volumes at low margins initially). The business model was to first aggregate and asses the demand for the key therapies and products in these markets. Basis this, CAPLIN worked with suppliers in China and India to get these products manufactured for them at scale. These were then sold down to exclusive appointed distributors in these markets who in turn supplied to the last mile pharmacy network and hospitals. Most of these drugs/formulations were long off-patent generics and thus could be easily procured from suppliers in China and India. Besides, these frontier markets had low regulatory requirements for drug approvals.

CAPLIN today is a dominant supplier in these markets in terms of market share with superior scale economics and market access. Over time, they have also built direct coverage of pharmacies (akin to FMCG companies building direct retail reach) which fetches better margins and real-time feed on market demand dynamics. CAPLIN’s distributors pay upfront cash for its supplies while CAPLIN can take some time before it pays off its suppliers. This makes this business light on working capital. Given CAPLIN outsources a substantial part of manufacturing and procures formulations directly, the business is asset light as well. This results in high 60%+ ROCEs with very high free cash flow generation. This operation thus resembles a sales, marketing, and distribution set up than a traditional pharma-based manufacturing one. Over time, the share of branded generics has increased to one-fourth of the overall pie fetching higher margins for CAPLIN.

Over the last few years, CAPLIN has started participating in large government tender-based projects from larger Latin American countries such as Mexico, Chile, and Peru. This leg of the business comes with somewhat lower margins and a reasonably large receivables cycle but is a large opportunity as there are few large competitors in these markets. The tender business today is about 15% of sales for CAPLIN and has thus far not seen any bad debts with hardly any visible impact on the overall margin profile of CAPLIN. Receivable days spiked up to 90 in FY19 but have remained steady with no further deterioration. In my estimate, tender business ROCEs are 20-25% which while lower than those generated by the base B2C business (working capital free), is still a good way to deploy surplus cash. The tender business potentially paves way for building a B2C formulations franchise in some of the new larger markets of South America. These include countries such as Chile, Peru, Mexico, etc. where CAPLIN is still to make a meaningful dent.

Prima facie, one would imagine that CAPLIN’s target market would be small and with lower margins given most of these countries are lower income with volatile economic environments. CAPLIN’s numbers tell an entirely different story. Starting with sales of Rs125cr in FY13, it has compounded sales at 29% since then and quite consistently. Even as the base has become larger, growth has sustained at good levels – last five-year sales CAGR of 25%. This is easily the top tier of the pharma universe not just in India but perhaps globally. Granted, their sales base is still much smaller (US$170mn) versus the larger peers (Cipla: US$2.75bn). But note that they have substantially outperformed most of their mid-cap and small-cap peers too.

Prima facie, one would imagine that CAPLIN’s target market would be small and with lower margins given most of these countries are lower income with volatile economic environments. CAPLIN’s numbers tell an entirely different story. Starting with sales of Rs125cr in FY13, it has compounded sales at 29% since then and quite consistently. Even as the base has become larger, growth has sustained at good levels – last five-year sales CAGR of 25%. This is easily the top tier of the pharma universe not just in India but perhaps globally. Granted, their sales base is still much smaller (US$170mn) versus the larger peers (Cipla: US$2.75bn). But note that they have substantially outperformed most of their mid-cap and small-cap peers too.

The base Latin American business we discussed above throws out a lot of cash. For context, for every incremental US$100 in sales, the business generates US$20 worth of free net cash even post taking care of all investments for growth. This calculation also includes the small tender-based business with its higher working capital requirement. Given this high cash generation, CAPLIN mgmt. could either return cash to shareholders or look for new investment avenues to grow the company.

They decided on the latter and have chosen to invest heavily in high-margin areas with limited competition such as sterile injectables, oncology, and ophthalmology. Admittedly, this was a strange pivot as this meant getting into an entirely different business with limited overlap with their Latin America business (except arguably the management grit). These products are primarily intended for regulated markets (the US being the key market) and need US FDA-approved manufacturing facilities in place. Moreover, the regulated markets need approved ANDAs and those need a large R&D operation able to build a pipeline in place. Sterile injectables as a space have lower competition and shortages in end markets partly because it is a hard one to crack with complicated manufacturing and a stringent approval process. Yet CAPLIN has taken this bet and one needs to wait to see in what measure this pays off. Notably, CAPLIN has refused to participate in the commoditized oral dosage formulations which is going through extreme competition and pricing pressure last few years.

Over the last five years, CAPLIN has invested a cumulative of Rs350cr as capex in this business and another Rs350cr as R&D spends (capex plus opex). They now have 5 R&D facilities and a team of 340 people versus virtually no R&D presence ten years ago. The next three years are likely to see another Rs450cr in capex. The capex is further picking up with a rising number of ANDA approvals by the US FDA and a rich 55-plus ANDA pipeline. This past and future capex have been spent on areas such as 1) sterile injectables manufacturing capacity expansion 2) ophthalmology and oncology OSD and injectables 3) API manufacturing capability for 70% of the final formulations (crucial to winning business in the US in the current era). 4) substantial investment in R&D infrastructure.

Their execution so far has been impressive. This became evident as I read through the last several years of annual reports. They invested in their first sterile manufacturing line in 2014 and gradually got approvals from regulated markets such as Europe and Brazil. In 2016, they also go the coveted US FDA approval which is very hard to get in the sterile injectables category.

In 2019, Fidelity invested Rs218cr in this sterile injectables business for a 25% stake at a valuation of ~Rs900cr. Note that this was even before revenues had started to trickle in for the US business. This shows Fidelity’s confidence in the space of sterile injectables and the management capabilities of CAPLIN.

Their US FDA regulatory inspection track record has been clean with minor observations if at all. To be able to pull this off in a complex space like sterile injectables is creditable. Parallelly, the company has been able to build a product pipeline with currently 18 product approvals in place. Out of these, 15 products are already commercialized reflected in the current quarterly revenue run-rate of Rs45cr and an order book of Rs175cr (as of June 22). The company has a pipeline of 55 ANDAs under work with a potential market opportunity of US$4.9bn versus the current US$670 market opportunity basis their current approvals.

The key point here is that skeptical as people may have been on this drastic new business entry by CAPLIN, early results seem impressive to say the least. Most importantly, this has been done while keeping the overall balance sheet healthy and not jeopardizing the overall profitability of the company.

Forecasting business prospects for this company comes down to taking a medium to long-term view of the two disparate businesses - Latin America and the newly incubated regulated markets business.

First, the Latin American business seems to be holding up well and grew by 20% CAGR basis even through COVID (FY20-22) with resilient margins. The opportunity set remains large as thus far, CAPLIN was present in the central American smaller countries but is now making headway into the larger markets such as Brazil, Mexico, Chile, and Peru. Some of these larger markets have a similar market structure to the smaller markets so Caplin can leverage on its prior experience. However, these are also semi-regulated and need approvals or bio-equivalence studies before launches. To address this, Caplin is using its recently scaled-up R&D infrastructure and knowledge base. The company has started a CRO with an investment of Rs30cr to conduct clinical trials for these markets. The CRO can be used for its use as well as do outsourced work in the future. It will be reasonable to expect CAPLIN to grow its Latin American business at a 17-18% CAGR for the foreseeable future. This is not a maturing cash cow but one which itself has a decent growth runway.

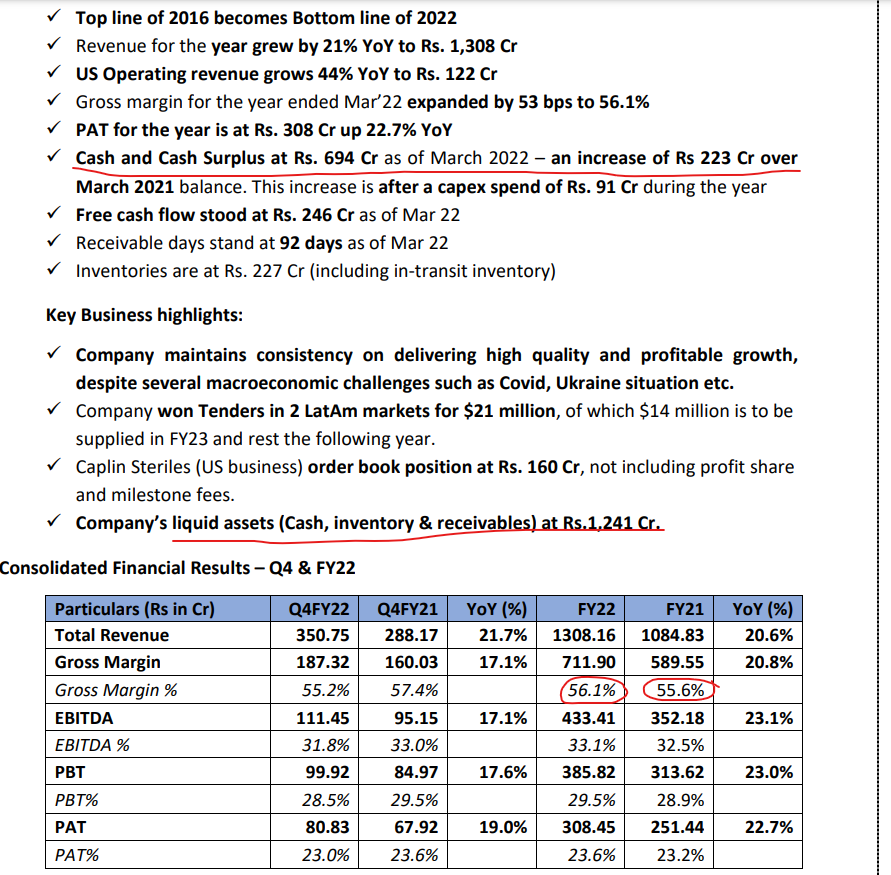

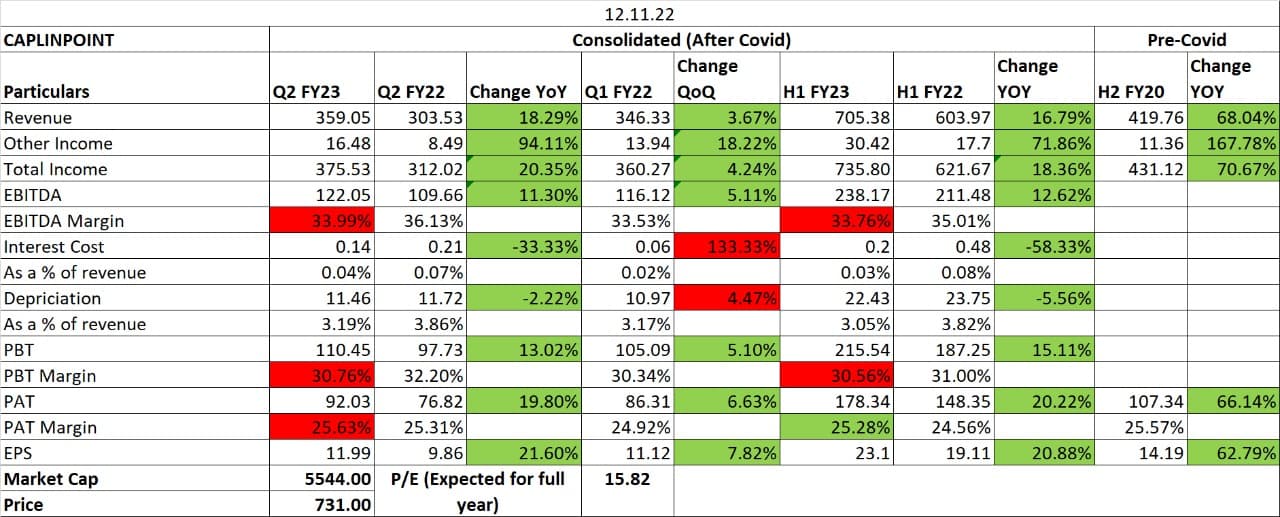

The second, and the most crucial piece is the regulated markets business which did Rs125cr (45% growth) or 10% of overall company sales in FY22. This should like to grow another 45% in FY23 (1QFY23 sales grew 60% YoY) and CAPLIN management reckons this should be a US$100mn business by FY26 (in my base case I have assumed US$55mn). This can go wrong, and plans do not always work out, but this is a management with a solid execution track record. For example, in FY16, they said that by FY22, their FY16 top line with become the bottom line of FY22 and that did happen. This is despite general fortunes in the pharma sector taking a nosedive. Their current guidance is that they will generate a cash surplus of Rs1000-1500cr by FY27. The US business achieved breakeven in FY22 excluding R&D spends (completely expensed and nothing is capitalized) and should turn green at the EBITDA level in FY23. The one variable to watch out for is pricing pressures in oral formulations spilling into other areas like sterile injectables.

The stock is trading at 16x TTM earnings which are in line with their 5/10-year averages. However, the stock was at nearly 50x between 2015 and 2017. While earnings have grown 6-7x since FY15, the PE multiple of derated 65% led to a 3x higher stock price change since then. However, the 3x move us upfronted with stock being broadly flat last five years although it is up 2x versus pre-COVID levels.

The likely reason for the de-rating is the entire pharma sector going out of favor due to the worsening US generics business. Pharma sector valuations have corrected 35% since 2015. Even though Caplin did not suffer from a poor US generics business, it seems a case of a small-cap stock suffering due to it being a part of the same pharma basket.

Basis FY24, the stock trades at 13x and this seems very reasonable to me with a high margin of safety given their growth prospects and consistent execution. I expect Caplin should grow sales and earnings at a 20% CAGR over FY22-25. Assuming an undemanding 15x exit multiple on FY26 estimated earnings, potential IRRs can be ~25%. My hunch is that exit multiples will likely be much higher if 1) the pharma cycle and valuations will turn/ mean revert at some point and 2) the market will take cognizance of the consistent progress by the company. If we assume a 20x exit multiple, IRRs can be more rewarding at 30-35%.