However not able to get the URL of their e-commerce site at all, no matter how much I search. If there is an e-commerce site and they are running it, there should be some mention of the word Caplin right? If anybody is able to find, please let me know

Can you please also share the source where we can find “Marcellus Little Champions portfolio”? it might be a good place where individual investors like us might be able to find new investment ideas to do our own research.

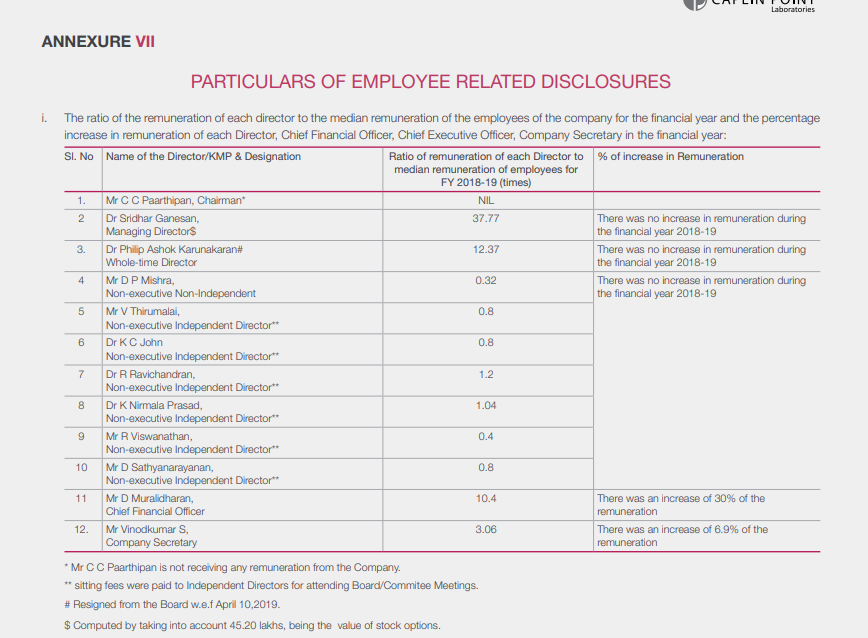

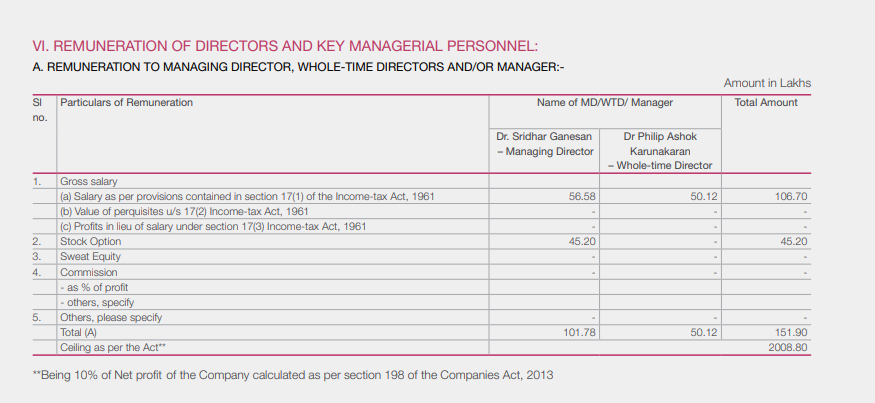

This company has operations in so many countries/continents. One can only assume that you need to run a very tight ship - both financially and operationally. It generated 200 crores of PAT. Then why is CFO paid only 25L, and CS only 8L? Not market rate at all. (as per FY19 annual report).

Thanks.

Agree with r13k.

Caplin point cash flow from operations is increasing constantly

Narration

Jun-10

Jun-11

Jun-12

Jun-13

Jun-14

Jun-15

Mar-16

Mar-17

Mar-18

Mar-19

Cash from Operating Activity (CFO)

0

13

24

33

60

50

44

55

23

107

87% of 10 year PAT cumulative has been converted to cash by Caplin Point

Periods

0

1

2

3

4

5

6

7

8

9

cPAT

3

10

18

32

58

99

144

215

317

465

cCFO

0

13

37

70

129

179

223

279

301

409

cCFO/cPAT

0.081081081

1.295845998

2.031007752

2.150139018

2.230132736

1.80798383

1.547477128

1.298974837

0.950963996

0.878795046

I do not see any red flags in Free cash flow change YoY either

Free Cash Flow

7.4

7.5

-12.3

13.3

24.6

36.2

30.0

-25.8

124.7

FCF Change?

0.1

-19.8

25.5

11.4

11.6

-6.1

-55.9

150.5

CFO Change?

11.4

9.0

26.9

-10.2

-5.2

11.1

-32.9

84.7

FCF to Sales

9%

7%

-10%

8%

10%

16%

9%

-6%

23%

FCF to Market Cap

110%

96%

-86%

20%

9%

12%

1%

-1%

4%

I don’t about GMM Pfaudler as I see that it is quite richly valued. But Caplin is available at a very good earnings yield of 6% which is like the Government bond.

No problems in cash flows of Caplin from above. Can you please elaborate?

Just one limited point, now that mar’20 results have been declared we should endeavour to include those in your table to get a more updated picture. For example, the cash flow from operations fell in FY20 compared to FY19.

Some are saying caplin point is financial shenanigan, when they are asked to prove they run away. Few points which help me to take contrary view to their claim

Promoter frankly accepted caplin went bankrupt in 2000 and they went to angola and saved it by selling generics

Promoter also guided that they are taking govt. tender and receivables are going to increase

They have not raised capital/ taken debt since 2000

Lot of valupickr member met promoter and asked lot of questions

So business is a cash generating one. I cant find a non-cash generating business which can cheat/cook books for 20 yrs.

Only way promoter can cheat us is by siphoning off money (like sun pharma). I dont think he will do by watching his interview [(https://www.youtube.com/watch?v=kDLe-zmaYjU&t=2002s) sorry, its in tamil] and approval for injectables by USFDA again reaffirming management quality. [After preliminary number checks(cash flow, thrid party transactions etc etc), I personally believe promoter honesty is lot more subjective than numbers (he can cheat us in thousand ways, no number check can confirm)].

@atulastra I went through the whole thread, I really admire you that you are holding this stock for 15-20 yrs inspite of lot of negative comments about this company

Disclosure: Invested recently. Felt bad that I ignored 6 months back that this is a financial shenanigans since it was trading far below thier industry P/E

Open to accept my ignorance if anyone proves its a financial shenanigan.

China has increased the API price by 25%. Given the present standoff between India and China, It will be difficult to assess how the business will be impacted. Any idea about this.

A conflict between India and China should not be a cause of concern for the company as it does not import any goods from China to India, and only exports the formulations from China to various markets overseas directly through its JV partner Jointown (China).

@Inimitable_Investor would it be possible for you to please request the experienced investors you have talked to to comment on the specifics of the financial shenanigans you’re talking about?

Actually I spoke to them recently as well. As they are not there in this forum they aren’t too comfortable their names being used here. One of the points they spoke about was spike in debtor days and poor wc management. When I countered them that Caplin was moving into different geographies and that’s why the change in the model, I was told it’s more complicated than that. Also, the success of the company in Latam can be attributed to their so called “Distribution network” in those countries where the governance practices are questionable. Can they replicate the same in other geographies while maintaining the margins? That’s a question I don’t have an answer for. Even experienced folks from VP during their visit to the company claim that the top management struggled to answer fundamental questions on the nature of the business. These are experienced folks who’ve spoken with so many Managements and this is the only company afaik that they have red flagged. They haven’t given out the reasons explicitly in this thread but they have given us a direction and I take their word. People can mock at me for not giving them straight answer but the fact is I don’t have a clear cut answer.

I am a newbie in the investment world and therefore prefer to err on the side of caution. But those who are confident of their research can invest in this stock. Afterall, much revered Marcellus have invested in the company.

@Inimitable_Investor I for one surely appreciate your views a lot, and am always happy to hear and learn from everyone’s views, specially those who have views opposite to my own.

I add my own comments on some of the management commentary explicitly in few places.

[Annual Topline]: Revenue up ~36% YoY to Rs. 904 Cr

[Annual Bottomline] PAT up 22% to Rs 215cr

[Q4] On quarterly basis, revenue was +24%, PBT +7%, PAT -2%

[US business] The subsidiary Caplin Steriles Ltd (CSL), operating in the Regulated markets (US), injectable business delivered a Strong 3.5x revenue growth during its first full year of commercial operations, contributing 8% to the operating revenues for the year: Operating Revenue at Rs. 65 Cr in FY 20 Vs Rs. 18.7 Cr last year.

[US business] Company has received approvals for 9 out of 17 ANDAs filed (6 in Caplin Steriles name). 4 products have been launched, with the next 5 to be launched within Aug 2020.

[US business] Total addressable market size of Caplin’s ANDAs approved and under approval - US$ 670 million.

[Sahil]: If caplin can capture 10% of this market, that would enable 500cr additional revenue every year. That is a 50% potential increase.

[US business] Company working on an overall pipeline of 15 ANDAs to be filed within the next 24 months, with an addressable market size of: US$ 1.95 Billion.

[Margin] Margin was lower on 2 accounts:

[Margin] A bunch of medicines were given with 0 margin on humanitarian grounds for covid-19 treatments.

[Margin] Inventory with acquired LatAm channel partners was sold at low margins.

[R&D spend]: R&D Opex increased by 90%+ YOY from Rs 28.2 Cr in FY 19 to Rs.53 Cr in FY20.

[R&D spend] Group’s R&D strength increased by more than 40% to 360+ Scientists in current year

[Cash position] Cash & Cash equivalents at Rs. 284Cr in FY20, an increase of Rs 61 Cr over previous year’s balance of Rs 223 Cr. This has since increased to around Rs. 343 Cr as on June 17th, 2020.

[Trade receivables]: Trade receivables grew from 160cr in FY19 to 229cr in FY20. Out of the Rs. 229 Cr of receivables as on March 31st 2020, 70% has since been collected as on June 17th, 2020.

[Backward integration]: R&D activity completed for 22 APIs, to be used for backward integration for both US and Emerging markets. This will help company’s competitiveness in entering larger tenders in Latin America and also on continuity of supply for US ANDAs.

Note that I (sahil) would expect this to improve margins as well.

[Acquisitions]: Acquisition of 4 Channel partners in Latin America helps Company with significant control on marketing, distribution and supply chain advantage

[Sahil]: One of the key moats for Caplin is the deep cultural relations they have established in these LatAm countries, enabling them to skip multiple levels of hierarchy which are generally there in these Pharma supply chains. For a general pharma company, the chain looks like: Company (caplin) => Importer (in some LatAm country) => Distributor => Retailer/Pharmacy => Customer. For caplin, this is starting to look more like: Company (Caplin) => Pharmacy => Customer.

[E-commerce website]: Company recently launched e-commerce website as part of proprietary 10X Healthcare portal, catering to independent pharmacies who are not visited by salesmen due to Covid-19 situation. This has helped company convert certain traditional credit-sales into Cash Sales, enhancing Cashflow and better inventory rotation. Company’s cash reserves enhanced by around Rs.60Cr during Covid-19 months of March to June.

[Sahil]: shows willingness to innovate on the part of the management. Along with their healthcare analytics, this portal should see them increase sales, possibly (purely speculation from me) making use of techniques like MBA (market basket analysis) to proactively recommend medicines for independent pharmacies to buy from them.

Key Risks

The company might find it difficult to sustain the same profit margins from their US operations due to the lack of the geographical generalization of their direct to pharmacy moat. IMO If (and that is a BIG if) they are able to do this it would be a true value unlocking event

For the injectables the company is preparing to supply, it is by no means the sole supplier. If the company is not careful about the type of injectables it chooses (this is to some extent dependent on luck) then it could find itself in an overcrowded market with a large capex already done and margins falling due to competition and downward price pressure.

While it looks cheap on a price/earnings kind of an evaluation, on a MarketCap/Sales basis it looks quite overvalued. This is mostly because of their amazing current margins. If margins reduce, it would become expensive even on P/E style valuations.

Would invite others to comment on the Q4/FY20 results, specially on the risks side.

No mention of what products they sell on their website. I find this very odd - as any company will tell their products. Mentioning the product names has got nothing to do with their IP

Most of business in LATAM - so there is geographical risk.

However, I got comfort when I checked and found that they are really doing business in LATAM and the elder son of the promoter is married to a Guatemalan and is in South America running that business.

Everything about the metrics like Sales/OPM/PBT/PAT CAGR and ROCEs indicate goodness for a long time. Don’t know if it is possible to fudge so well for so many years. They have no borrowings also - so ROCE=ROE and the solvency risk is minimal.

To some of Sahil’s points:

Net Margins are at 27% with the capital turnover ratio dropping to 1.2 from 1.5 The capital turnover ratio has been falling over the years from 2.6 to 1.2. This is basically Sales/Capital Employed - so Capital employed is growing at a faster pace than Sales! That is mostly because of retained earnings increasing. So you have a company whose sales is not increasing as fast as the retained earnings

They definitely are employing a lot of people. I got more than 1000 results for employees on linkedin. So was looking at profiles in Caplin Point to see what type of people they are hiring. I could find that they have some PhD scientists But 1000+ employees is comforting

Some people like their deputy CFO have worked at Asian Paints in the past which is comforting https://www.linkedin.com/in/m-sathya-narayanan-aa909634/

I don’t understand why the salaries are so way below market salaries unless they are getting compensation in stock

Is there information about acquisition cost of the channel partners? Because acquisitions are one way to fill holes in the balance sheet. If they are acquiring so many channel partners, how are they paying for them? If by cash, why has cash on the balance sheet increased? If they are paying by stock, why the amounts are not disclosed?

Why is Cash flow from financing high? What are they financing?

Cash on company’s bank accounts that is not returned to shareholders or invested in business is usually suspect - as we saw in the case of Satyam. Why only 40 paise per share as dividend when there is so much cash that can be returned to investors?

Company has fixed assets addition of 75 Cr last year which is very less and also the total net fixed assets is only 236 CR. Not sure if this is lot or less in pharma space as pharma is not my circle of competence

So there are a few items that need further attention. I have been invested holding about 300 shares at 338 INR purchase price

Honestly, it seems that there is a lot of uncertainty going forward. Decreasing RoE and increasing receivables are a concern coupled with the difficulties of doing business in US as compared to Latin America.

I’m not saying that the company will necessarily do badly, I’m just saying that there seems to be much more risk associated with the stock that I had earlier expected.

I’m currently booking profits and exiting completely. This company will be on my watchlist. I will re-enter when there is some price correction or I see good uptake in the US business.

Looks like Sridhar Ganesan took a salary of 1Crore and his remuneration is 38 times median. So median salary is around 3 lakhs - which seems okay for pharma

CFO and company secreatary salaries are 26 lakhs and 7 lakhs. For a company with such a huge market cap, this seems low

ESOPs are granted only to Dr Sridhar Ganesan. Given that R&D is such a competitive space, how can company attract top talent with these salaries?

I saw few mismatches between consolidated cash flow statement and balance sheet in FY20

In the consolidated cash flow statement, they have mentioned trade receivables increased by 23066.67 lakh but in balance sheet current assets are FY20 22896.49 lakhs and FY19 15980.60 lakhs so difference between these two is 6916. I can’t understand the disparity between two figures.

Likewise for inventories, current assets ballooned from 3744 to 23823 lakhs (increase in inventories of 20079). But in cash flow statement they have mentioned increase of 703 lakhs.

I know that they have purchased trade channel partner in LATAM even that I cant find in cash flow statement (Purchase of fixed asset 7673 lakh and sale of investment 988.5 lakh).

I attended their conference call and another person asked the same question. Sridhar sir tried to answer but he couldn’t get it and myself also didn’t. Chairman Paarthipan sir asked to send personal mail if he is not satisfied with reply.

I am getting the eerie feeling that they are using acquisitions for opex.

Many disparities or things to ponder about

How come they acquired 4 LATAM partners and it is not in Cash flow from investing at all. What is this cash flow from financing increase? Why is it so large? What are they financing?

Their joint venture in China seems to be with hainan Jointown pharma that is based in Wuhan (of all places). Seems like some rigged company. If you are doing a joint venture, why would you want to do with an unknown company and not a market leader in China? funnily, the jointown pharma website is also not opening

Also they seeming started e-commerce sales in LATAM but the website could not be traced. Does anyone have the link to the e-commerce site?

Could it be possible that the company that an ace investor referred to in South India, where the promoter’s son is abroad and bills invoices to the dad is this one?

Looks like low P/E has most of the junk in the market.

I am starting to get an eerie feeling about this company now. Planning to exit. Thanks to the forum for helping in diving deeper