They are looking for retired officials that can conduct audit at different branches on a contract basis. That is a good news, I guess (about management policies)?

Everybody is sitting tight I guess, hfc bring a stable business, there are very few variables to track and discuss, just sit tight, which is also not easy

A good 45% of my portfolio allocation is to Canfin. Theoretically i know it is very lopsided, however the fact is its worked for me on this pick. I’m certainly long on this.

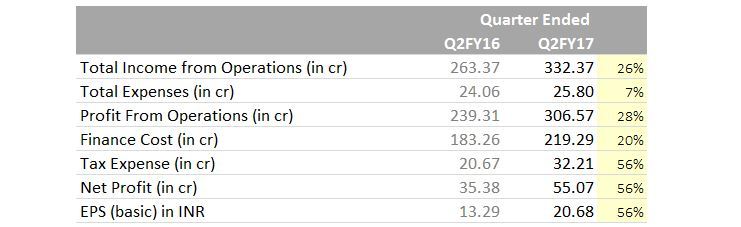

Yes. I was thinking it was just about to hit the target price given by Motilaloswal (Rs.1550) and will re-trace. But it went way past that to touching distance of what Edelweiss had given.

Hsg fin cos to gain from RBI move to deepen bond mkt: Can Fin

Housing finance companies will benefit from the central bank’s move to deepen the bond market which will result in lowering their cost of funds. One of the likely beneficiaries of the move Can Fin Homes expects a cost advantage due to the move.

Additional 5 percent allowed for funds to invest in housing finance companies in the paper will see demand from bond market, SK Hota, Managing Director of Can Fin Homes told CNBC-TV18. There’ll be a cost advantage to companies like ours, he said, adding, that he expects liquidity to increase which will help faster growth in loan book.

Hota acknowledged that competition in the industry has increased but was quick to say that there is no threat from peers on the ground level as Can Fin Homes caters to a niche segment of salaried class customers in middle and lower income segment.

The company saw a 29 percent on-year loan growth in FY16. Hota said the company’s growth rate has stabilised at 28-30 percent since its inception in 2011-12 and he expects the company to maintain the growth rate going ahead.

While analysing CANFIN It came to my notice that out of all the HFC including HDFC only CANFIN has a positive operating CASH FLOW all the other peer companies have negative cash flow.

As I am confused about this , will request fellow learned and experienced knowledgable investors to put their valued inputs about this.

Looking at the key metrics everything in Canfin looks superior to repco but still lower valuations…looks like this re-rating could continue till the valuation gap closes

Can fin performance has been much superior compared to Gruh or Repco which are being value significantly higher than Can fin .This valuation diff for sure is going to get reduced .On PEG ,though not the right valuation for a home finance company ,its trading at a discount to PEG of Nifty !

Repco is a market leader in Tamilnadu and some parts of S India. NIM is the highest in Repco with an impeccable track record hence the valuation gap with Canfin.

Talking about Canfin it is of course an excellent performer but there is a PSU shadow. Gruh has premier valuation due to its parentage and steady predictable boring performance

Just noticed the dividend distribution policy document in the company website. The summary is as below. Can anyone explain the point "20% of paid up equity share capital’? The paid up share capital would be 26.62 Crores, isnt it? Are they saying the dividend amount (excl. tax) will be max of that? But just this year, they declared Rs.10 dividend, which is exactly 26.62 Crores…

“11. SUMMARY:

11.1 The management upon compliance to all the rules, guidelines and regulations as

detailed above in this policy may recommend to the Board of Directors the dividend at a

rate (exclusive of the dividend distribution tax or any other applicable taxes on dividend)

not exceeding the maximum of any of the following:

a) Dividend payout ratio of 20% (excluding taxes)

b) 20% of the paid up Equity share capital

11.2 While recommending such dividend the management will also take into account

dividends declared during the preceding 3 years.”

Shareholding pattern as of 30th Sep’ 2016 is published. Notable changes QOQ

1- Catamaran Management Services Pvt. Ltd. has reduced stake from 3.94% to 1.29%.

2- FIIs have slightly increased stake from .26% to .31%.

3- Total number of shareholders have increased from 30,267 to 33,814. YoY shareholders have increased by 29.75%.

More details http://www.bseindia.com/corporates/shpSecurities.aspx?scripcd=511196&qtrid=91.00&Flag=New

Let’s hope that the dividend distribution policy would be suitably amended to pay higher dividends next year.

Sometimes, I wonder why any mutual funds are not buying shares of Can Fin homes. I understand that the shares are not extremely liquid and large shareholdings are with blockholders like Canara Bank, Chattisgarh Investments, etc. But, Canara Bank declared that they want to sell at least part of their ownership and met many mutual funds and PE funds. Subsequent to this, I expected more institutional interest in CanFin Homes.

Hi Pranav, they have also mentioned “interim dividend” in the policy document. So the max limit conditions may apply per dividend (interim / final). And like you, I too eagerly await canara bank to sell its stake. If it is to a big credible institution, then it will become a long term hold for me.