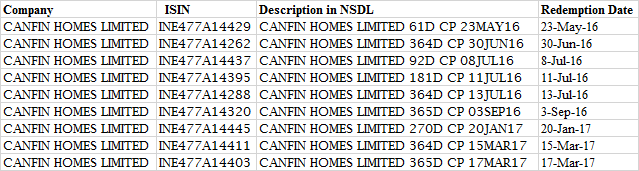

Pulled this info from couple of sources… looks like they have exhausted their entire debt limit of 2500 crs. see the snip attached. The cost of recent issuance of 3 yr bond is 8.37% (Apr 2016), compared to 8.69% in Apr 2015. Regarding the question of tax free bond - to my knowledge recent issuance was by HUDCO in Mar 16 - 7.29% for 10 year bond and Canfin is majorly issuing in 3 yr tenor. (hope this data helps, i am new to this forum and this is my first post)

Just want to add that Canfin also started issuing Commercial Paper (CP’s), this may further bring down their interest cost as cost of CP’s is lower than bonds (maximums tenor for CP’s is one year and brought by MF’s mostly). I got the data on outstanding CP’s from NSDL, could not find the amount though. They can raise upto Rs.2500 crs in CP’s also (pl see the link) in addition to Rs.2500 crs of bonds.

@venkat.reddy - thanks for compiling this data. This is pretty useful. In today’s time there are multiple sources which can be used to extract the needed information…kudos to you guys!

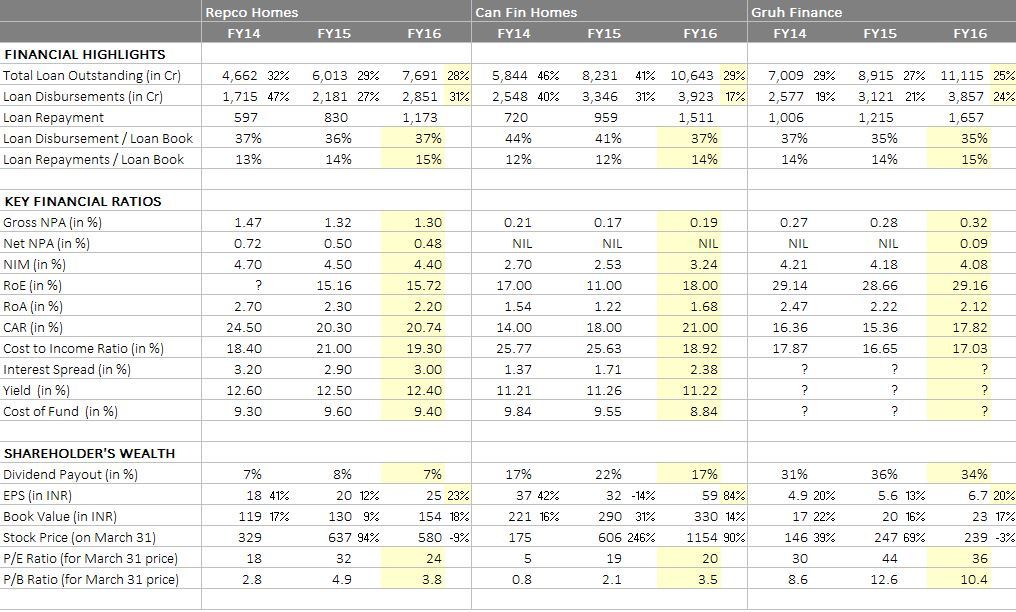

It is quite apparent that loan growth parameters have been slowing down. One can argue that the loan outstanding growth in 2013 was 111% and hence not sustainable, and hence it is come down to 29% in 2016. However, the slowdown is starker if one looks growth in approvals and disbursements (these have already been calculated in the excel file).

Repayments are happening faster than disbursements (see repayment to disbursement ratio below). Also Repayments as a % of increase in loan outstanding has also been increasing.

I agree, these are just different numbers giving same conclusion, that is, growth has been slowing down compared to earlier years. Just that these ratios take out the base effect (of high 2012/13 growth) to some extent, and focus on what has incrementally happened during the particular year. Clearly, disbursements have not been able to keep pace with repayments. I welcome views on this.

As a disclosure, I must add that I had invested at 160-170 levels and exited at around 400. I was not able to see how growth rate could be maintained because Canfin operated in the same space as other banks (unlike Gruh/Repco, where I am invested). Plus I did not quite believe the NPA numbers (still dont). The keyman risk was too high for my comfort levels, being a PSU. My fear (perhaps irrational) was that if someone else comes in place of Mr Illango and finds several cockroaches in the kitchen, which were just hidden, then the picture could turn nasty. I have no basis for this, except for some similar instances in PSU Banks. These were just my biases,and I have been proven wrong by the stock price movement since then. But no regret.

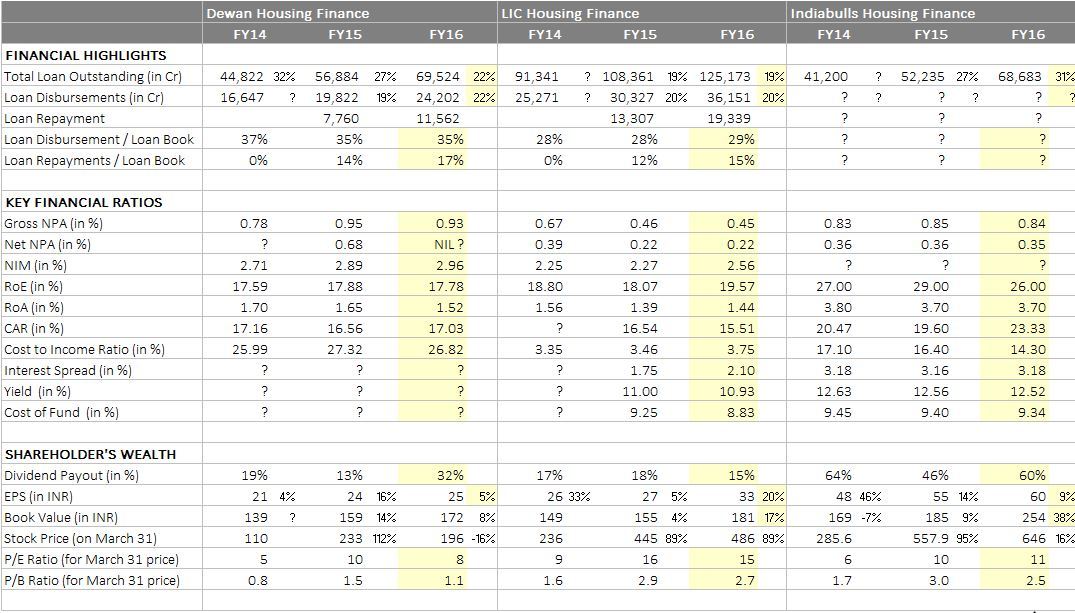

I think diwan has more exposure to builder loan portfolio means they are directly funding real estate. This is my view and I can’t remember but may be read somewhere otherwise it’s also a good company.

I suggest do a google search with “customer grievances/complaints against DHFL/India Bulls”. Do that for other HFC’s as well. I was looking for LAP and applied at Punjab National Bank. The loan was sanctioned subject to co-owners giving an NOC. I did not get an NOC. The PNB person interacting with me said “koi baat nahin kahin aur se kara denge…” and he mentioned DHFL and India Bulls specifically. It was then that I googled. This was in Dec '14.

Hi Sammy11, You mention that you don’t trust the numbers from Canfin as its parent, Canara bank is a PSU. But you are also invested in Repco Home Finance, whose parent in Repco Bank, which is a co-operative bank, still coming under government control. How do you compare them both w.r.t transparency, management credibility?

Mr Ilango was instrumental in what Can Fin is able to achieve so far in terms of growth.

His good work will continue to show up in the bottom line numbers for FY17.

Interesting thing would be to watch the balance sheet growth in Q2 of FY17. This will be a good indicator of the approach taken by the new manager. If balance sheet growth dips, the valuations might come down.

Why so much pessimism abt new MD? He has been associated with bank since 1990, served across the country and worked as a DGM of recovery wing. As of now, housing finance is a low risk business in India. Lets hope for the best and observ his performance.

I see this as a good development as shareholder. In banking and finance system, you should rotate people or even give compulsory leaves to key people. This help you in finding the impact of person and many times unearths scams. I think Canfin should have well defined processes in place, where the growth / NPA does not impact due to change of MD. I can think that system may be more effective under old MD, but it should not have been achieved by compromising the quality.

I will be worried If NPA increases in next quarter . I am fine if NPA remains same with some taper in growth.