Here is some comparison of housing finance companies that I prepared using data extracted from Capitaline

Size - Can Fin homes is tiny compared to others so growth should be good.

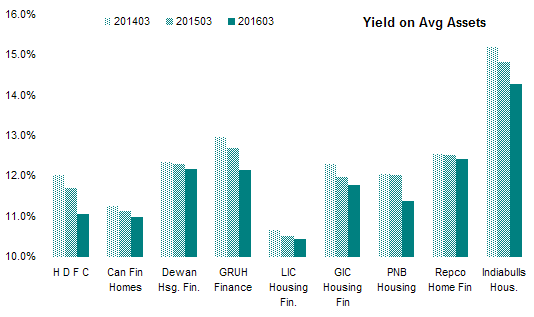

I generally classify HFCs based on the rates they charge as that determines the profile of borrowers and risks. Indiabulls is a sub-prime lender and LIC is safest. HDFC is quiet safe and Canfin is close to the safe lender category. Yields are also dropping across the boards with high interest lenders seeing the biggest drop. IMO is this actually good for the industry as loans becomes affordable and default risks reduces.

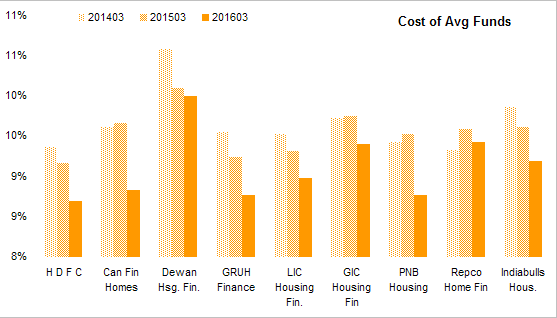

Cost of funds - One of the most important number for an HFC is cost of funds as lower costs helps an HFC offer lower rates and that allows it to attract safe borrowers keeping credit costs low. All bank related HFCs have low cost of funds (HDFC, Canfin, PNB Housing and Gruh) whereas others have higher costs. Cost of funds is dropping over last 3 years which allow lenders to lower their lending rates while protecting their interest margin.

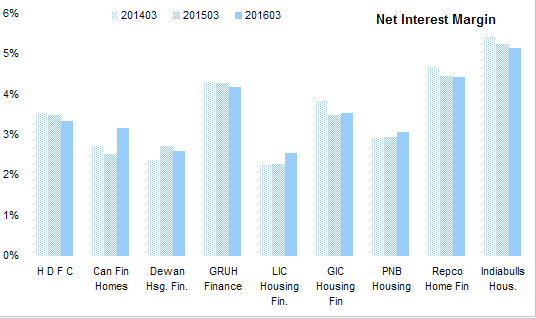

Net Interest Margin - The holy grail of lending business. Despite dropping yields some lenders have been able to maintain or even improve their NIMs. Indiabulls is at the top, Repco and Gruh are close second (due to their high cost loans). LIC is the lowest as it as low yield and high costs. Canfin and PNB are somewhere in between. These numbers are still better than banks and other NBFCs. Only MFIs have higher NIMs.

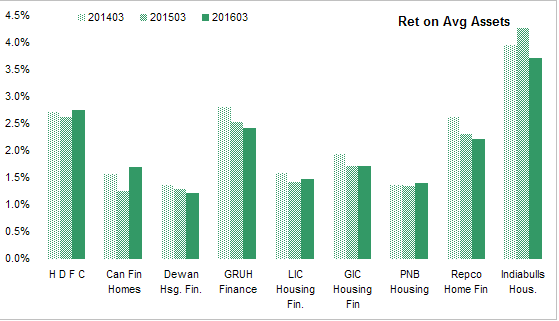

Return on avg assets - IMO this number is more important that NIM as assets are funded by both debt and equity and NIM captures only the debt costs.

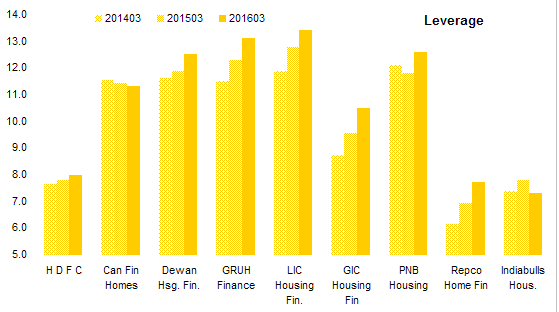

Leverage - Perhaps the most important risk indicator. Indiabulls and Repco has the lowest leverage reflecting it’s risky asset base and LIC has highest as it has safest assets. ratio for PNB is pre-ipo so current ratio is about half. HDFC numbers are standalone.

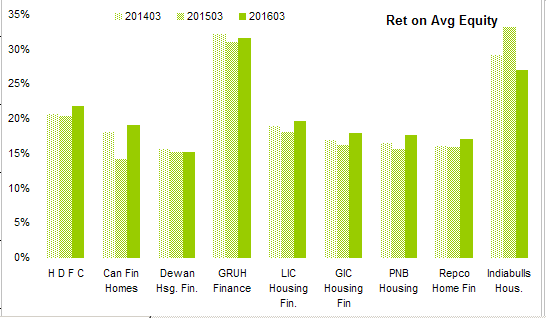

Return on Avg Equity - The most important number from an investor’s perspective. This number sums it all. Gruh is the clear winner with it high interest loans and low cost of funds. Indiabulls is close second as it has managed to earn a high yield assets while keeping interest and credit costs low. What is remarkable is it is able to earn a high ROE without leveraging it’s equity with too much debt. It’s leverage is among the lowest.

Canfin is just about average. Industry as a whole managed an average of 17-18% which I think is good.

Next set of charts compare the cost structures

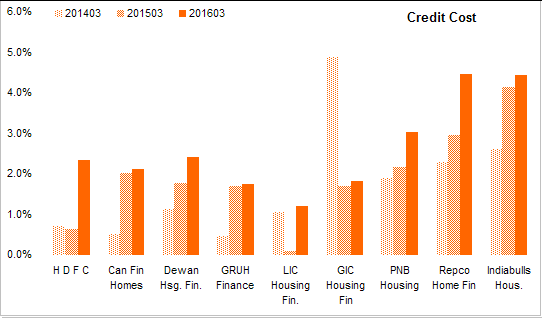

Credit costs - Provisions as % of Total Income. Ability to manage credit costs is IMO most important ability. Indiabulls with it’s risky loans has highest costs while LIC HDFC are lowest. PNB’s credit costs are rising at an alarming rate. They may be loosening credit standards in order to grow.

Spike in HDFC in 2016 is a one time cookie jar provision (using the windfall gains from sale of insurance stake).

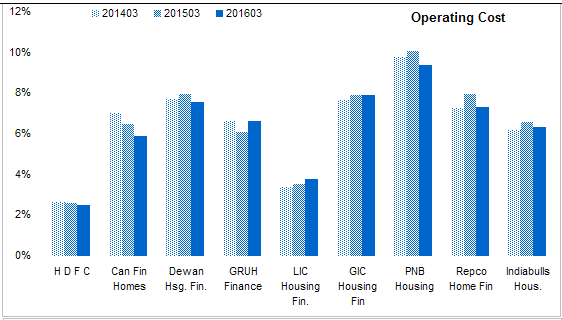

Operating costs - Everything other than provisions, interest and tax as a % of total income… This is the cost of running the business. HDFC LIC clearly has an economics of scale. PNB is growing so costs should come down. Canfin is average.

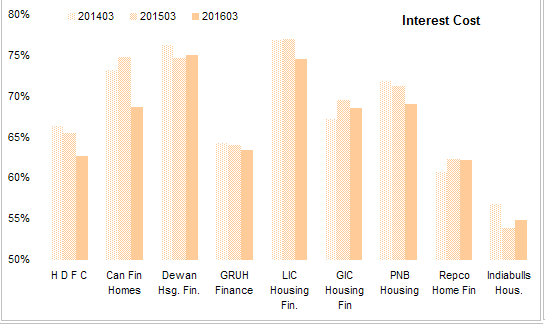

Interest Costs - Interest expense as % of total income. Biggest cost component. LIC has the highest interest costs as it makes low interest loans and is not linked any bank. Indiabulls managed to fund high interest loans with low interest funds. Canfin is somewhat on the higher side but there is big improvement in this metric in recent quarters. IMO this is the single most important driving price of Canfin.

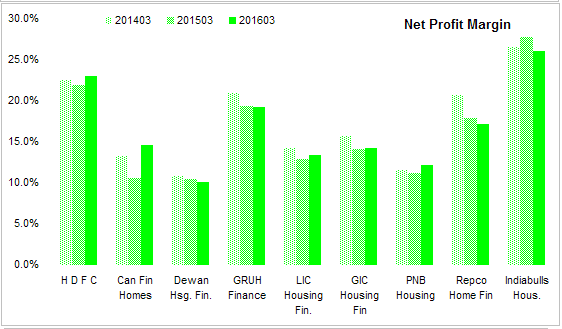

Net Profit Margin - The bottom line. Not as important as ROAA but an important metric. This is what is left after all costs are paid and (sufficient) provisions are made. This number can be easily manipulated by manipulating provisions. Cookie jar provisions are common here. Indiabulls scores here.

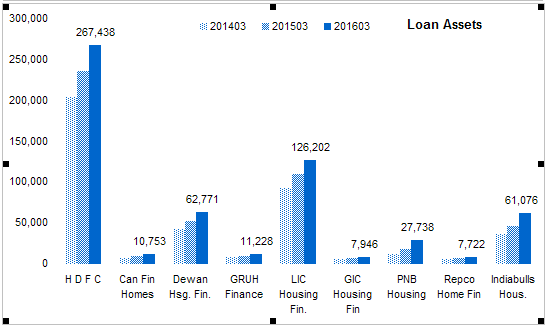

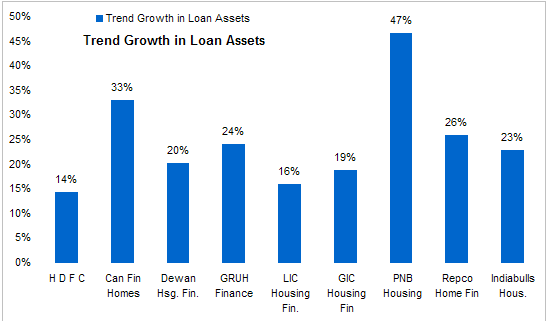

Growth in loan assets - What investors chase. Big ones grow slow, smaller ones are racing. This will continue if the industry is not hit with a wave of defaults.

Overall, I think HDFC GRUH scores good on safety and quality but have low growth rates, LIC is safe but low profitability and low growth, Dewan has bad numbers in most metrics, Canfin and PNB are improving and growing, Repco is on a slippary slope, Indiabulls for not for faint of heart, GIC is a dog.

Disc - Invested in Canfin, PNB and Indiabulls.