I searched for these notes referred by you, and having searched them I wanted to make my comments:

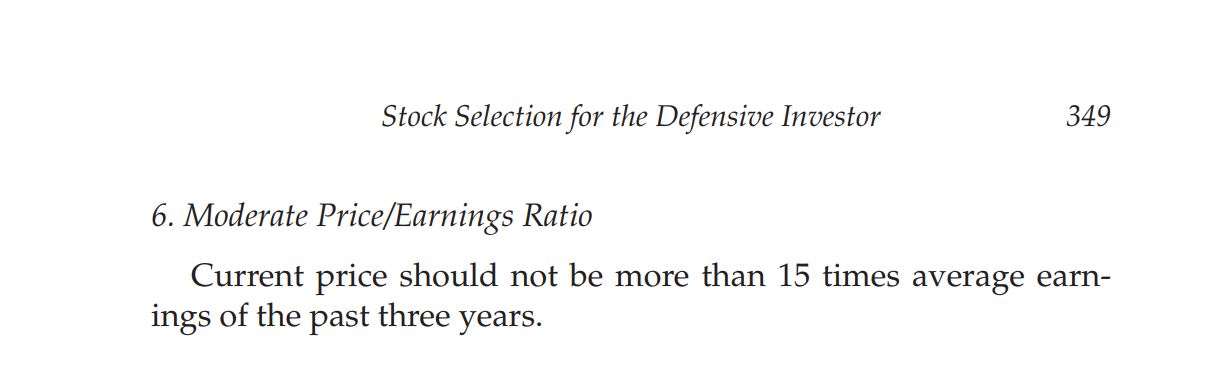

- On page 349 of the revised edition, Ben says the following

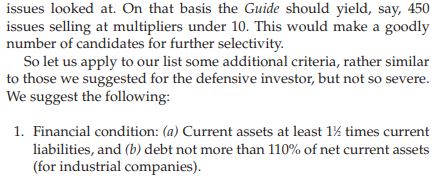

This is among the 7 criteria he lists for a “quantitatively-tested portfolio” for a defensive investor who follows the suggestion of bonds and diversified stocks. This is in lieu of investing in the index.

Thus this PE recommendation is one of the 7 criteria for the defensive investor. This brings us to the question, who does Ben define as the defensive investor?

He defines the investor and his expectations on page 6. He says, "The defensive (or passive) investor will place his chief emphasis on the avoidance of serious mistakes or losses. His second aim will be freedom from effort, annoyance, and the need for making frequent decisions."

In other words there is no returns expectation that Ben sets for the defensive investor. Consequently taking just one aspect of his 7 criteria derived out of a set of standards, for one type of investor who does not have any returns objective, from one edition of a 4 editions book spanning atleast 24 years, and say that Ben was wrong, seems to me highly misguided.

You may say that buying stocks at low PE is not the way to make wealth, even high PE stocks can make wealth etc etc. But to pull Ben Graham into this by quoting his book without context, and question if he was wrong and try proving that, besmirches him and his work.

I am a student of security analysis and have read almost all of Ben Graham’s work (books, lectures, his memoir and his some papers). In my opinion, I find him so brilliant that not only do I collect all his books / writings / speeches, I collect multiple editions of his book Security Analysis spending a bomb, just so that I can get a few additional chapters or thoughts of that brilliant mind. I have also read others but Ben’s writings stand out so brightly that it dims out others. You can say I am almost a beggar for his ideas and thoughts.

In that light I hope you can understand how I feel when you say he is wrong on recommending a certain PE  . I know Charlie Munger said he is wrong (maybe he was but that’s hindsight), I know Ben made more money outside of his advice, but they pale when compared to his overgenerous contribution to the field of finance.

. I know Charlie Munger said he is wrong (maybe he was but that’s hindsight), I know Ben made more money outside of his advice, but they pale when compared to his overgenerous contribution to the field of finance.