If anything,small shareholders should be glad with the deal since there was no reason for stock to be at CMP if not for CGC buying them out.

2 Likes

As per the filing, the tendering period was to open on Apr 13, 2022 . I could not find the relevant tendering option in hdfc securities. Anyone facing similar issues while tendering?

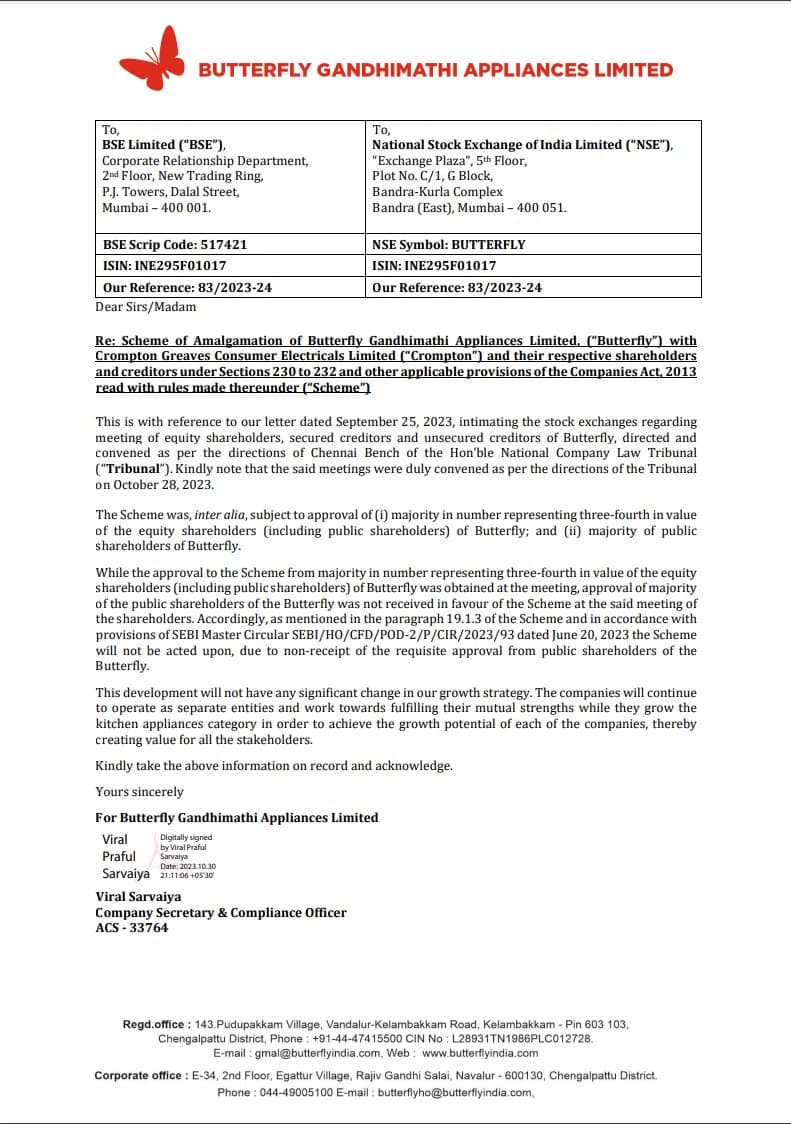

A proposed merger (amalgamation) between two companies, Butterfly Gandhimathi Appliances Limited and Crompton Greaves Consumer Electricals Limited did not work out.

Context:

The companies wanted to merge with the approval of their shareholders and creditors.

Outcome:

The majority of Butterfly’s equity shareholders, including the public shareholders, approved the merger. However, the majority of the public shareholders of Butterfly did not approve the merger.

As a result, according to SEBI regulations, the merger will not happen because it didn’t receive the necessary approval from Butterfly’s public shareholders.

Impact:

- Butterfly and Crompton will continue to operate as separate companies.

- They will focus on their respective strengths and continue working to grow their kitchen appliances businesses.

1 Like

Basic Question about the process of Merger Can someone throw more light on what happened here?

- Majority(3/4)th in value approved while

- 3/4th in number of shareholders did not approve…

Since retail shareholders would constitute the majority here, it seems we the retail investors did not approve, i wonder why?

I did not vote, and may not be wrong in assuming majority of the public/retail investors would not have voted… neither for nor against the motion of merger… And if its a SEBI mandate, i wonder how do mergers actually go through…

My investment thesis in butterfly was the near 10% arbitrage with CGConsumer, which now is dead! So have to reassess the growth potential specially given the new shareholding pattern.

On one hand CG Consumer on board should definitely be a plus but on the other the old owner promotors being out would that be negative?

Quick glance at ROCE and valuations comparison with TTK Prestige suggests, it is trading not too expensive, but growth has been weak in general for both!

Appreciate any inputs…

Seems a case of no promotor stake hurting the firm!

CG Consumer earlier with the Thapars was acquired by PE firms, Advent International and Temasek Holdings in 2015. However both PE firms exited in 2019 end, make 100% return in 4 years.

since then the growth was not great, which might have forced the management to go for acquisition of Butterfly. however the acqiuring multiples paid and the overall price paid was huge. Butterfly has corrected more than 50% since.

Strange but I bought Butterfly for the reason that it was trading cheaper to its merger ratio determined price and i wanted to take advantage of this arbitrage; and how post the shareholders of Butterfly refused to merge with CG Consumer, I took that also as a positive that they feel, their firm should hold better value and hence did not agree to merge… Shows my inability to change direction and starting to fall in love with your stock.

2 Likes