As mentioned in the thread, I too think their advertising style is quite different.

8 Likes

Well the long wait is over and ultimately it’s coming …

2 Likes

Good observation.

Do we have any info on how the royalties are used by the receiver?

Are they ploughed back in some way back to the burger king india eco-system ( eg finance assistance in setting up a restaurant)?

how does this fixed cost compare to say a Westlife or a Jublilant foodworks ?

1 Like

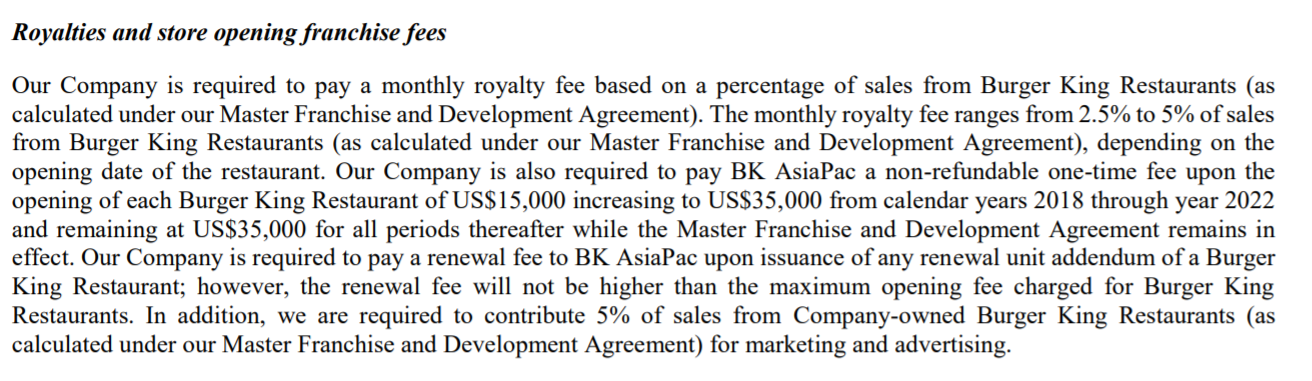

Royalty is generally a percent of sales…2.5 to 5 percent in this case. Ideally, it should be a percent of profits. Imagine a growing company not making a single penny as profit having to shell out MoM increasing royalty for decades on its growing sales. The criteria of opening a target of restaurants every year… something about 700 by 2025 approx in this case is another case of excellent arrangement for parent where it’s visibility grows, market grows, sales grows and hence the royalty…with the growth of profits or rather making of profits being the sole responsibility and headache of Indian subsidiary, management and investors.

Having said that, same is case with every west oriented chains like McDonald, jubilant etc. …not sure about percent though. Also, Starbucks maybe a bit different as 50% ownership is directly by parent and 50% by indian company, shareholders…so royalty should ideally not come into picture in case of Starbucks…would be good if anyone has more details on that.

Bottomline, there is a price to be paid for brand name even before you make a penny in profits. It’s a shame but as opportunity runway and growth is so huge, we cannot ignore considering this negative arrangements…the management competence and vision of Indian subsidiary hence becomes very important here.

For me, the right question should be not only comparing the arrangements with parent for each but also questioning the ownership structure, indian management competence, vision and ethics as well…as only if that is top notch can they ensure growing profits out of any arrangements with parent, not to mention that they will then also ensure a most competitive arrangement…thoughts welcome…

Disc. Invested in Tata Starbucks via TCP and tracking position in Westlife. Interested in BK and will apply in the upcoming IPO as runway of business is huge and want to participate in the consumption story.

Above are just my thoughts and I may be completely wrong in my assessments. Not a recommendation to buy/sell.

5 Likes

Regarding ownership structure here, I understand BK is owned by a PE and PE typical think short to medium term and look for exits quickly…see the case of Mphasis as Blackstone looking to exit.

How can we get answer on indian promoter quality and vision in this case as PE will look for exit at every opportunity.

Secondly the criteria of 700 restaurants by 2025 is something I am not able to understand if it’s for the good or otherwise for indian subsidiary. Definitely good for parent but should store growth not be driven by business performance rather than a pre written agreement? Is there any such agreement in case of Jubilant, Westlife? It’s certainly not there incase of Tata Starbucks where they keep recalibrating their growth and store number targets based on business environment rather than just to increase sales for parent…

What is the history of this PE incase of other food franchisee it holds like for example dominoes in Indonesia…for how long it keeps and and then looks for exit? A promoter which has an exit in mind in day one may be bothered about arrangements with parent till time of its exit or affecting its exit. In short should we as investors think long term in a company where the promoter itself has an exit in mind?

Pls note above is just from a general perception about PE who typically exit in 3-7 years or whenever they get decent XIRR. Not that the promoter of BK are looking for any exit at present.

Would be great if someone can provide more insights on this aspect. Thanks

5 Likes

First day application numbers for BK India IPO :

- QIB : 4.04 crores (16% subscribed; applications received for 0.64 crore shares)

- NII : 2.04 crores (70% subscribed; applications received for 1.43 crore shares)

- Retail : 1.36 crores (15.5x subscribed; applications received for 21.08 crore shares)

Total : 7.44 crores (~3.1x oversubscribed; applications received for 23.15 crore shares)

Another 6 crore shares have already been fully allotted to Anchor investors on Tuesday for ~₹364 crores.

As SEBI guidelines say retail investors must be allotted at least one lot (i.e 250 shares), around 54K people will get allotted (1.35 crores/250).

Is it possible that if QIB/NII portions remain undersubscribed, their shares will be added to retail kitty? Do rules allow this?

Application numbers and stats are from the ipocentral website.

Does anyone know what is the per store unit economics of this business (ie break even, number of loss making stores etc) ?

I didn’t find this information in the RHP or any finance blogs.

Any views would be helpful.

Thanks

Hi everyone,

Can anyone share insight about the promoters. How is the corporate governance of the company.

Can the profitability of the company improve in a big way for shareholders to benefit?

If due to work from home, people shift from urban cities to their hometown, are the promoters ready to open the stores accordingly. Can they achieve operational profitability the way jubilant foodwork has ?

What was the intention of the company to come out with an ipo such low valuation despite bull market

2 Likes

The valuation is not low. Only the price of the stock is optically low.Burger King India Ltd - IPO Note_Dec’2020.pdf (1.3 MB)

4 Likes

I don’t get the IPO but bought a small portion today @122 … to me this price is bit high so I would suggest avoid any kind of euphoria. Although the long term view intact but at current level this price is very high as low margin product likes them should be traded at a low premium than this.

2 Likes

I guess it is very difficult to figure out whether Burger King would be profitable in a big way. No doubt, the stores count will increase due to their mandate but I feel Jubilant is a better bet due to higher margins, less of owned stores and more of franchise, higher margins in PIZZA compared , very high store network and excellent delivery based model.

2 Likes

I don’t feel Burger king is going to be profitable till at least 2026 mid half as they have to open some 700 stores whether they are profitable or not. But again, if the management is wise and can give a tough competition to McDonalds at least , this story can be a good bet. As per my experience, me and most of my friends think of burger names like McVeggie / other happy meals and not even once , have we thought of burger king product names. They will seriously need to up their brand game or the story can turn out to be real bad(increasing debt and net losses) if they don’t take away market share .

Disc: Invested post IPO.

3 Likes

Basant maheshwari wealth management has bought around 27cr worth shares today @ 122

Same can be checked in bulk deals data today

Disclosure : Not invested. Considering.

2 Likes

listing ceremony BK

INTERVIEW WITH MD

AT BLOOMBERG

1 Like

Hi guys I have been researching this company since two years now and when I have written this thread I said it is the most awaited IPO and will have a very good listing but currently at least as per my analysis the price run up very high with less than 5 year track record of execution we must wait till some revenue traction happen before jumping into the stock. And specially Everstone has a history of exiting their position whenever they made high gain this is a major problem with any PE backed company. So please be very cautious about investing in this stock at this price. The business is undoubtedly good and long term prospect is very intact but price is too much exorbitant. .

16 Likes

How do you say that long term prospect is intact, the cost involved in opening store is very high + the competition they face from McDonald and unorganized market. Margins are less in burger compared to Pizza.

Revenue growth is not a problem but consistently growing profit is a big challenge.

1 Like

I had this risk in mind but seems market is not much bothered about it. Collective wisdom seems to say that PE backed company is not much of a risk but a better corporate governance than family owned franchisees. (Westlife Vs Burger King valuations keeping in mind execution so far).

What are your and others thoughts on a PE backed company’s risk profile? Exit would obviously remain an overhang but is it an actual RISK to business strategy and execution? Thanks

2 Likes