Really great result by oldest exhange in Asia.

But real mettle will be tested in bear market. Let’s see how it plays out.

Really great result by oldest exhange in Asia.

But real mettle will be tested in bear market. Let’s see how it plays out.

Anyone has the pdf of earning call ?

some analysis details here:

if listing fee is 40% of the total operational income, then during bear phase or even in an average market, can we expect the company to result in loss.

Market will face both bull and bear phases and BSE is adequately capitalized to ride the tide. Personally you should also have a view of the market and any investment should be done after adequate due diligence, evaluation of your own risk appetite and maintaining strict hedge/ stop loss.

I believe that BSE is here to stay and will eventually capture more market share(both organically and inorganically) as our market grows and matures - this is an ultra long term story.

Views are strictly personal.

Disclosure: Invested in BSE.

AJ

Companies will stop paying listing fee when their stock isn’t doing well?

The only concern is 45%+ revenue contribution comes from equity transaction wherein it has low Mks . If NSE tries to be aggressive , BSE will have problem retaining his revenue .

DIsc : Invested

Provided they go bankrupt!

I was under the impression that listing fee is one time fee. Is it annually paid to BSE?

My question was that only in bull market, new listing happens. Between 2008 and 2014, there were negligible listings. So BSE income from listing gets affected in such a case.

Listing fee is paid yearly, It depends on Mcap though, there are different slabs.

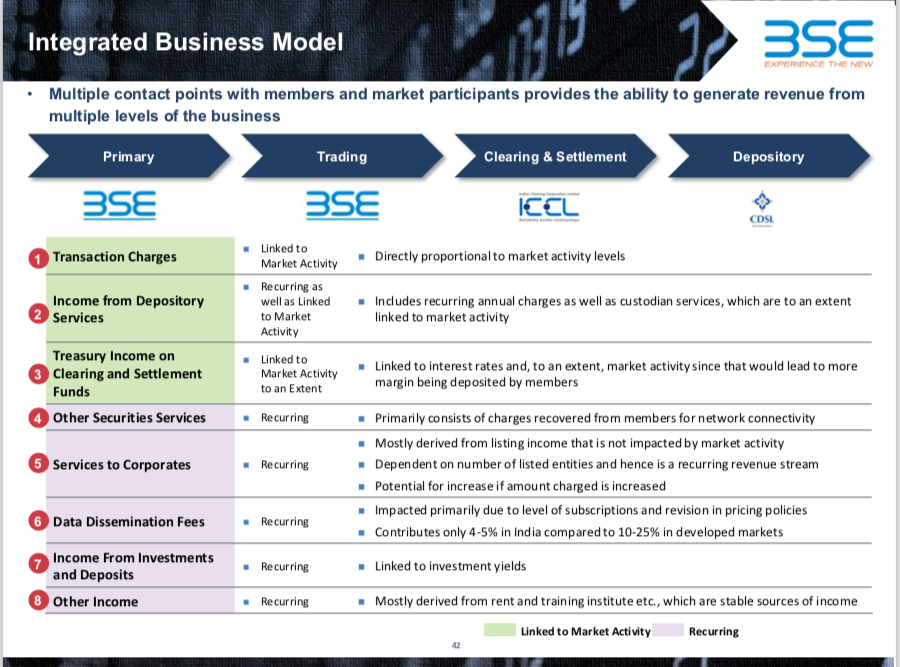

Would recommend you to go through this slide and connect with the management to understand what portion of this is recurring and what is cyclical?

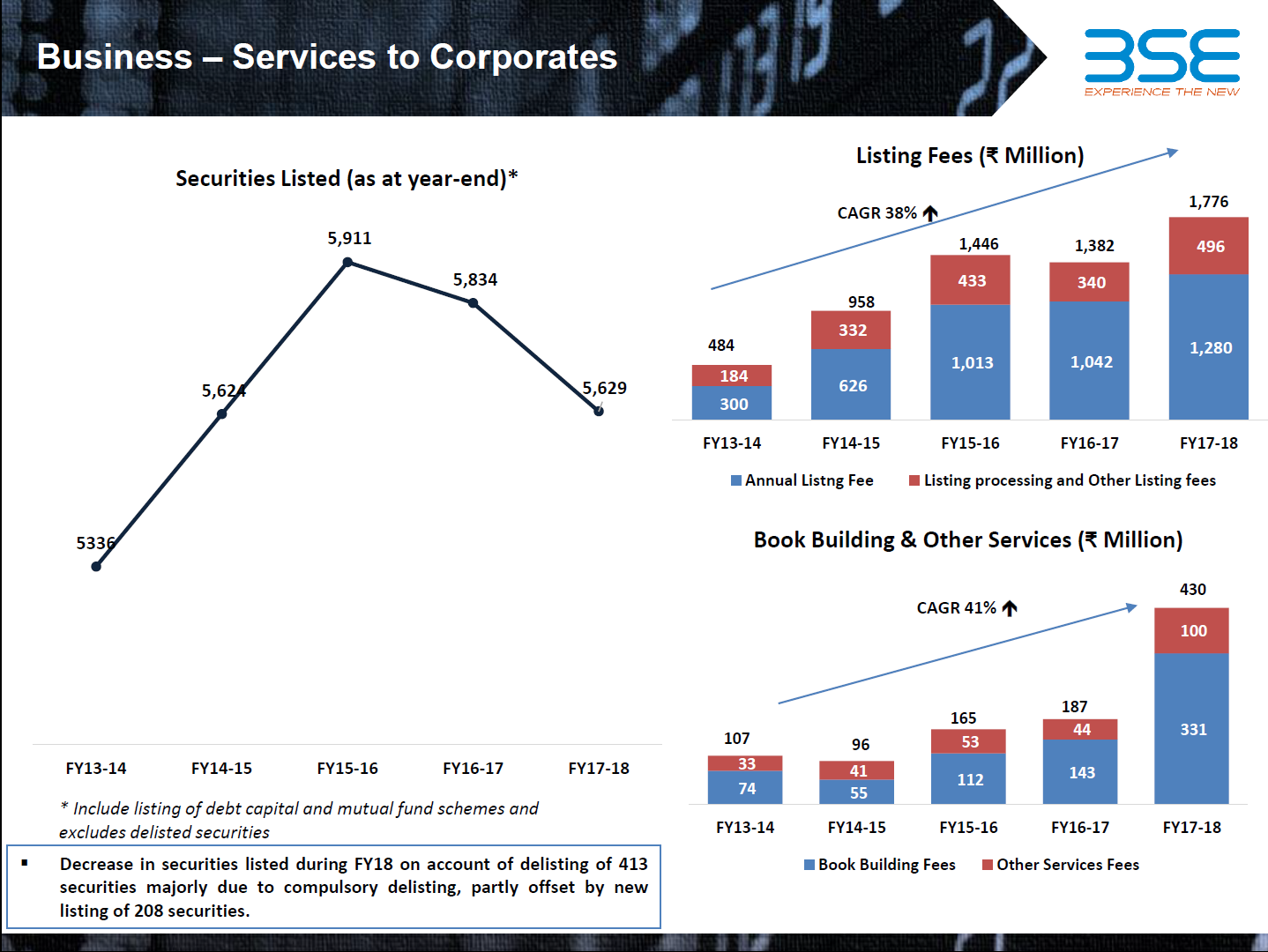

My take on this is that Income from corporate services has almost quadrupled from 59 cr in FY14 to 220 cr in FY18. 100 cr of this increase came from Annual fees which were hiked in the said period if I am not mistaken. The rest of the increase of 31 cr is from Listing Processing, 26 cr is from Book Building and 6 cr is from other services.

So the majority of the 160 cr increase is from recurring annual listing, the listing and book building fee has a cyclical component and could potentially revert back by the same increase we have seen in the current market, in a bear phase. This number could potentially be 57 cr but we don’t know where it would settle down. A longer look back into BSE’s revenue segmentation would reveal where these components settle down in a bear market.

Problem is we know IPO listing is linked to market activity which comes under services to corporate but management classifies it as recurring.

read it again on the right side of it …

Here linked to market activity means it is more related to trading volumes . Services to corporate is more linked to general economic activity

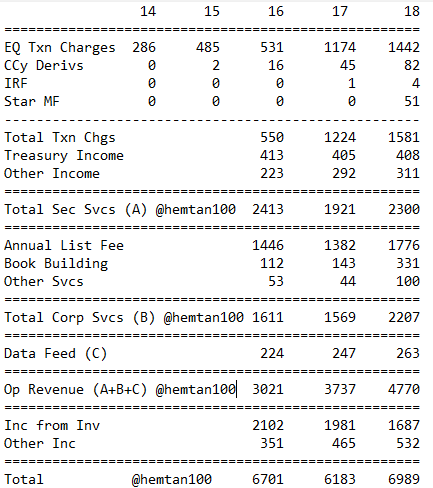

BSE - quality of earnings improving significantly

Recurring annual listing fees now at 25% of total income.

Income from investments decelerating due to significant div and buyback payouts.

Three triggers

a. Significant op leverage at play if Star and Ccy derivs continue exponential growth

b. NSE listing whenever that happens

c. Treasury and investment income should get better yields in a rising rate scenario

While each of these three play out, patient LT holders get compensated in the form of 5% div yield. Any buyback on top of that is a bonus

BSE first Indian exchange to be designated as DOSM by US SEC

Does this hold good potential for BSE?

Think so. BSE will interface all the international transactions, hence bagging the fee on the transactions