Q1FY21 CCT Notes

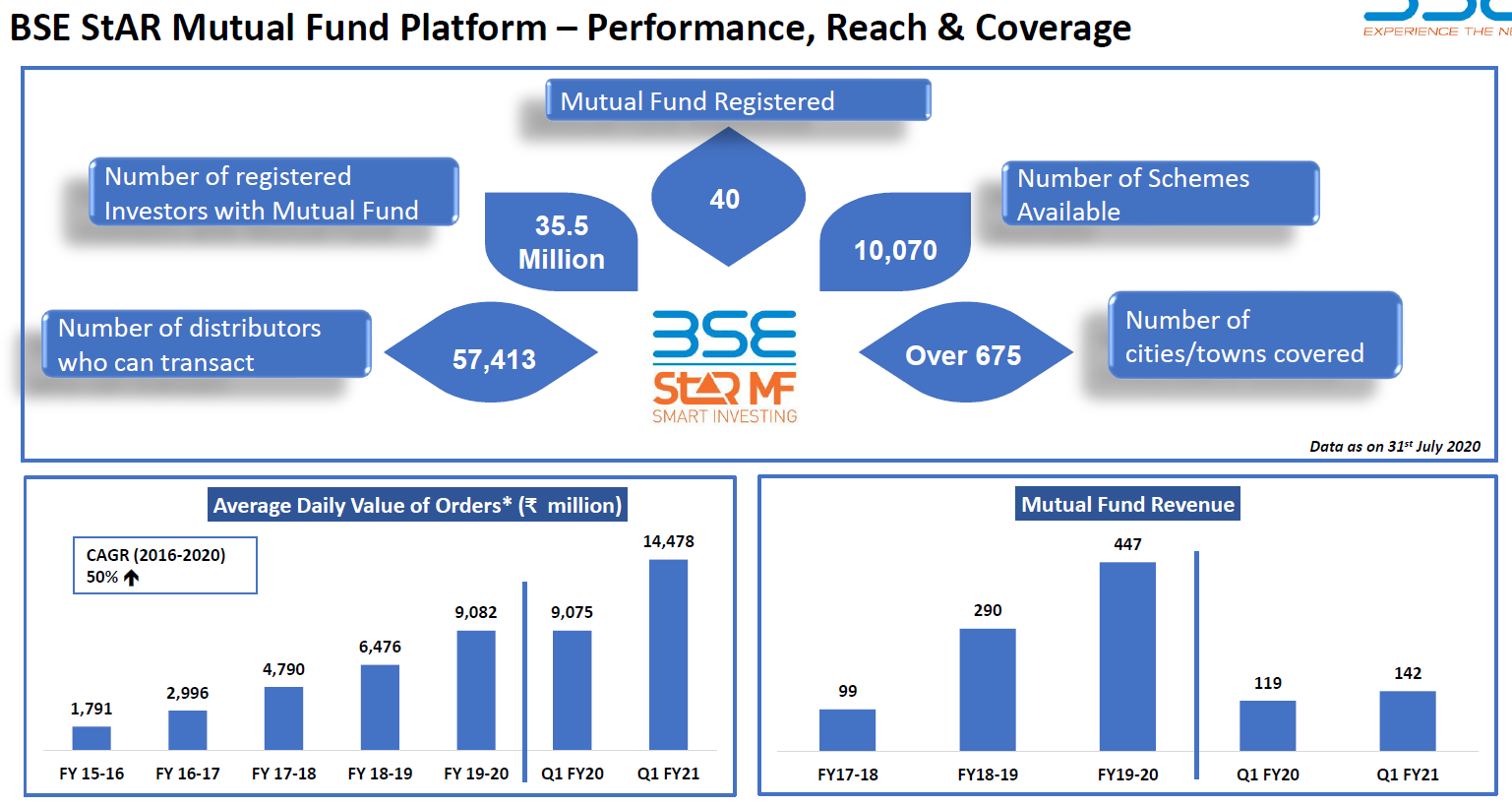

Star MF

52% increase in orders YoY, 186 Lac vs 122. Record 11.56 Lac in one day. SIPs up by 51% to 1.78 Lacs vs 1.18 Lac YoY. X-SIPs at 5.76 Lacs vs 4.67 Lacs YoY. Value of orders up by 57% at 85k Cr vs 54k Cr.

Revenue at 14.19 cr vs 11.9 cr YoY. Revenue share at 17% vs 12% last year. MS at 80%. Realizations per transaction will be lower this year, will be offset by growth and plans to increase revenue via VAS like e-KYC, commission distribution.

Partnered with LIC MF for e-KYC, we will facilitate complete digital customer on boarding.

Board has approved to list Star MF. Too early to comment on the structure of the transaction currently.

Previous concall you said we save 300-400 for the MFs per transaction, so why reduction in price now?

Basically, there is a competitive pressure because NSE earns a lot of money on their other businesses, so they tend to subsidize the newer businesses to a level where it becomes hugely non-competitive for everyone to do those businesses. Although BSE StAR MF is a much larger business compared to what NSE does. Despite that NSE offered very, extremely low amounts of transaction charges to association of mutual funds who together with NSE suggested that we need to match that otherwise they will move over to NSE and because of that, we have to match those rates. We have not reduced the charges because of COVID in fact we continue to the older charges because of COVID. But in future we have agreed due to this competitive pressure and AMFI’s collective pressure on BSE.

Everyone is paying, and they have some of them have dispute on certain other areas for the past. Going forward at least AMFI is committed where they will not have, anyone will not raise this disputes, but AMFI is able to collectively reduce the charges to be paid to us but not able to handle the disputes of their own members as and when they raise. So, it’s a bit of a mixed bag.

Sir just coming to StAR MF. Sir, you already have about 80%, 90% market share in StAR MF in that category. So, you have the market power sir. So why would you go about reducing prices, I am unable to get that part?

This is not a liquidity-based market. This is a distribution-based market and there AMFI and NSE combined to push us into a corner to say that they are all going to move or mass which would have created a disruption overall. That’s why we had to start charging less to match NSE prices.

Sir but my limited understanding is that the distributors actually love your platform. And it would be very hard for a distributor to actually move from say StAR MF to NSE’s platform is my understanding correct sir?

In some way yes, I would also love to believe that and at the same time some large ones may be enticed by other people to also go with them if sort of AMFI decides and things like that right. So, there are more complexities than we think there are. So, life is not so easy.

For the StAR MF to charge we don’t differentiate between whether it is a direct or indirect we allow both and there are now SEBI has allowed like MF utility the large corporates to also trade directly through BSE StAR MF. So that also that service will be launched this quarter. But the numbers are very few there. You can get a lot of volume in terms of value, but we charge on the number, so the numbers are few there but it’s just that we also are going to start that additional service

Software for commission clearing has been tested, we are in the process of launching it this quarter.

EBIX JV

Has 3290 registered POS. Total POS 7000+. Premium collected till July end is 78.77 lac. 1901 policies issued. Started motor, health, life. MF and insurance distribution will complement each other.

BSE holds 40% in JV through BSE investments LTD.

In a way Policybazaar is a pure web play, ours is a little bit of a physical play because distributor point of sale person is actually selling by showing the different aspects of the policies to the customer. So, there are a lot of differentiation between the two. Policybazaar doesn’t help you in finally executing the transaction because they take you to the website of the respective company. While as our person is able to also not only take you to the company, but also pay and give you the policy in your hand and within a few minutes or within few seconds. So, it’s a different thing.

Yes, insurance agent which they are called POSP, point of sale persons but good thing about is any layman can become also our point of sale person if he satisfies some criteria. So, if people are unemployed or want to have additional income, they may be able to become literally point of sale persons on BSE at no extra cost to themselves, and then they can sell the insurance to everyone in any area not only in life, but general, health, auto and everything.

It’s a distribution model, it’s not an exchange framework. So, it will get money as a distributor and then naturally people who are selling will get the maximum out of it, some small portion will be kept by the company.

In our case, our fees what we call point of sale person model, theirs is a web model, there are different models by the regulators. So, this does not allow a direct connectivity to the customer. So, currently, I don’t think it is possible for us to allow directly. Of course, we have a broker license. So, we can also go to the person directly as a company not through POSP, but currently we do not have people to do that. We are currently focusing only on making life easier for the agents to become agents of multiple companies in multiple areas, not only say life insurance only particular company No, not that way, they are trying to give you everything under in the same computer and you can compare and show it to your clients and give them the best service. So that’s, there are CRM systems involved in everything which is given in that it’s a webbased platform. It’s a browser-based platform, but it’s not for direct customers.

Commission he will be getting from BSE Ebix which he does get today also every month.

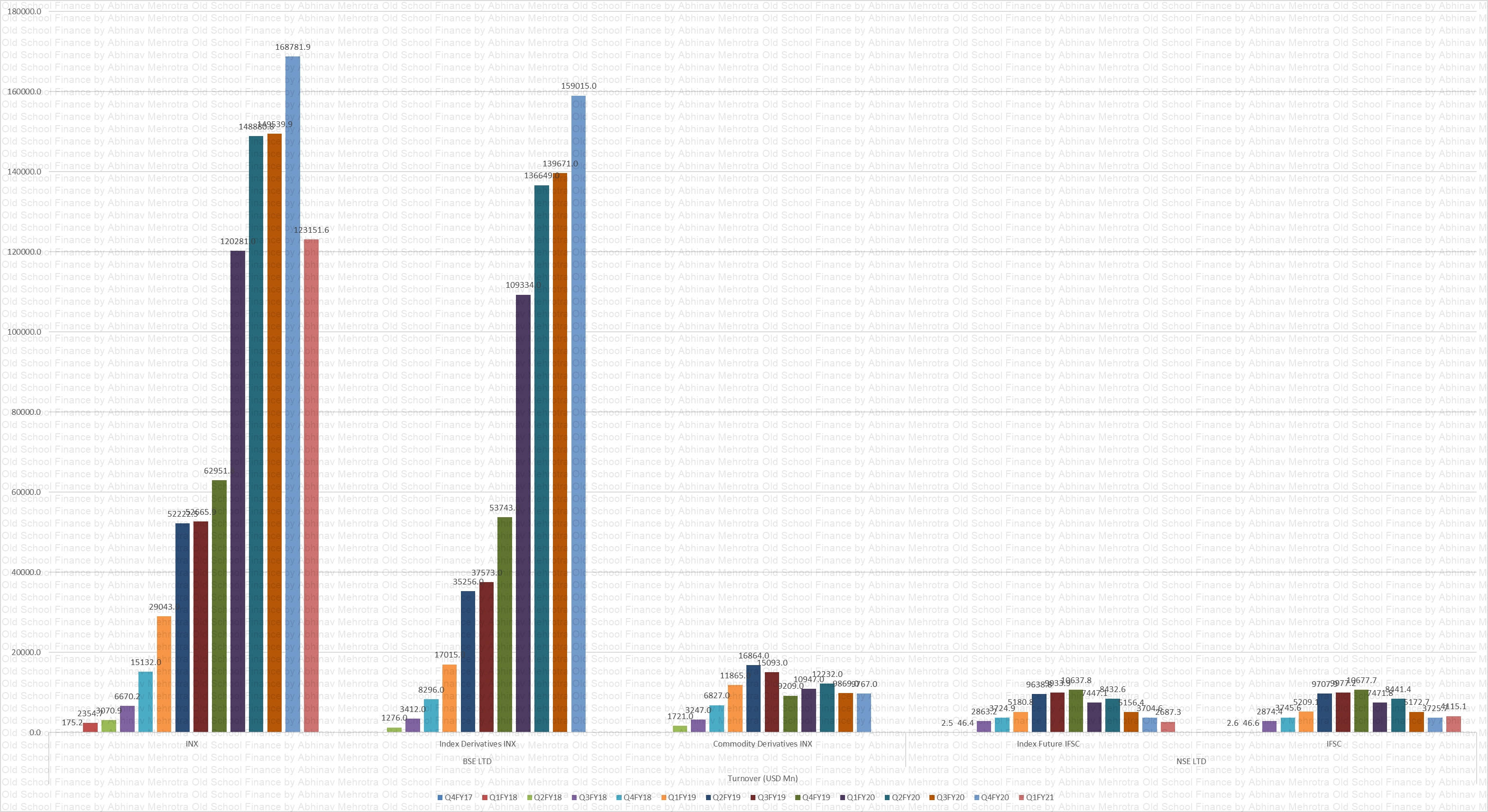

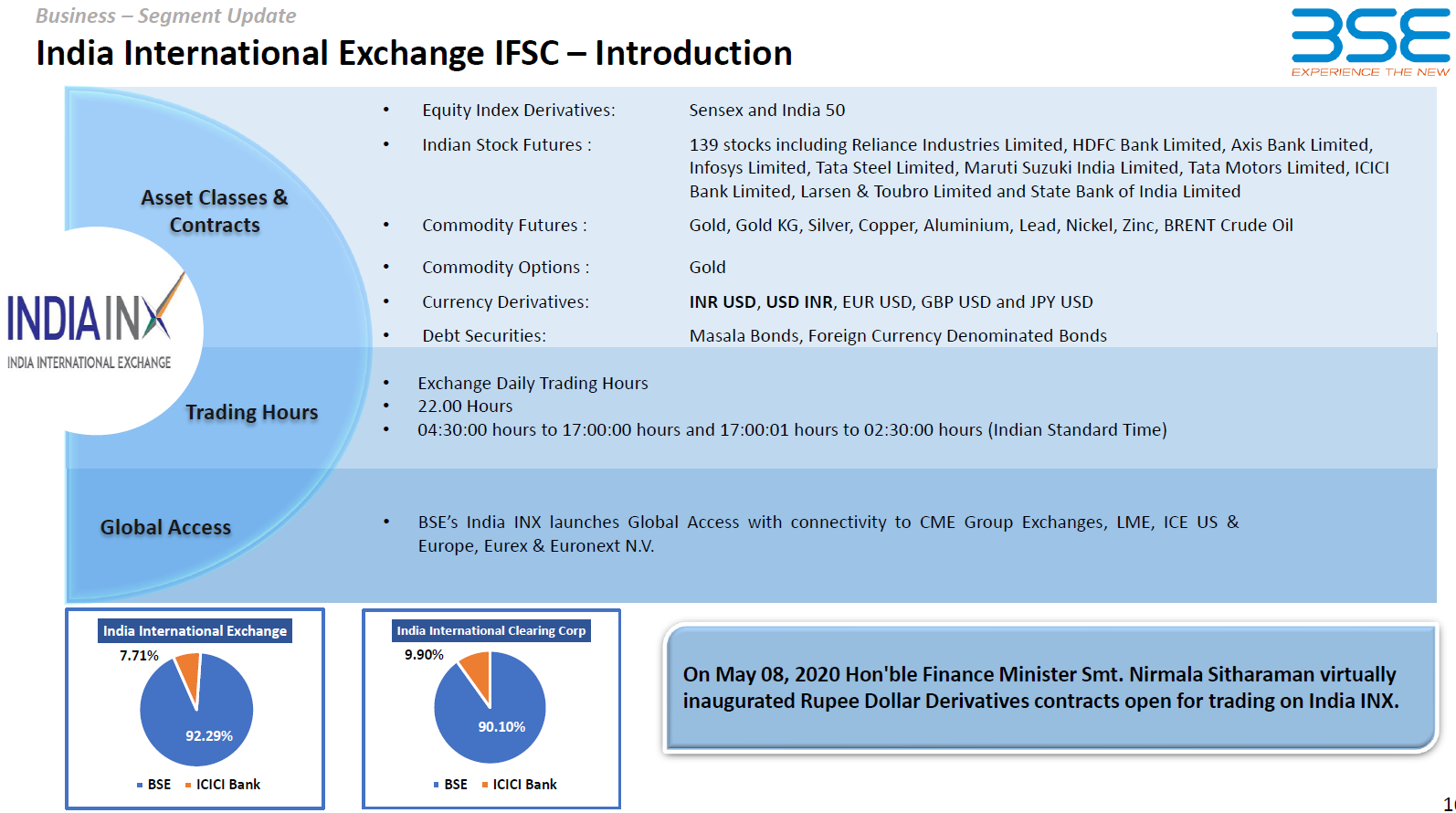

INX

Significant contribution from Equity derivatives 85% to total ADTV. 91% MS in derivatives. 31% MS in currency derivatives.

Indian international exchange has the same issue, is that the NSE’s own exchange called NSE IFSC is charging zero. In fact, they are also paying for the order flow. And that’s where we also have to pay for the order flow and till the time, they are able to subsidize, and nobody stops them from being so anticompetitive. This will continue and that’s why basically, in certain areas where we become large like in StAR MF, we started charging when NSE was not charging. And there also they’re still acting anti-competitive. So, we have many areas in which we have gained success in terms of market share, but we have not able to, we have not been able to gain the monetary aspect of it because of the NSE’s anti-competitive activity in all these areas. And that is where basically, we have in a way this quarter we are also hoping to take up with the regulator requesting them to look into the issues and ensure that fairness prevails going forward. And once that happens probably, we’ll see how the charging in different markets including in the India International Exchange can happen.

So, premature charging may actually end up bringing away liquidity. So, what you’re saying to some extent is your experience or what I call success buyers, that monopolies are able to do that. Once the BSE become monopoly it might be able to do that, till the time we will have to basically keep on struggling, on the. First it becomes monopoly and becomes so large that other people cannot even come closer, then it may be able to charge some things so that’s why you’re sort of asked your suggestions are most welcome. But in some ways, they are a little out of way.

SME

MS in listing is 61%.

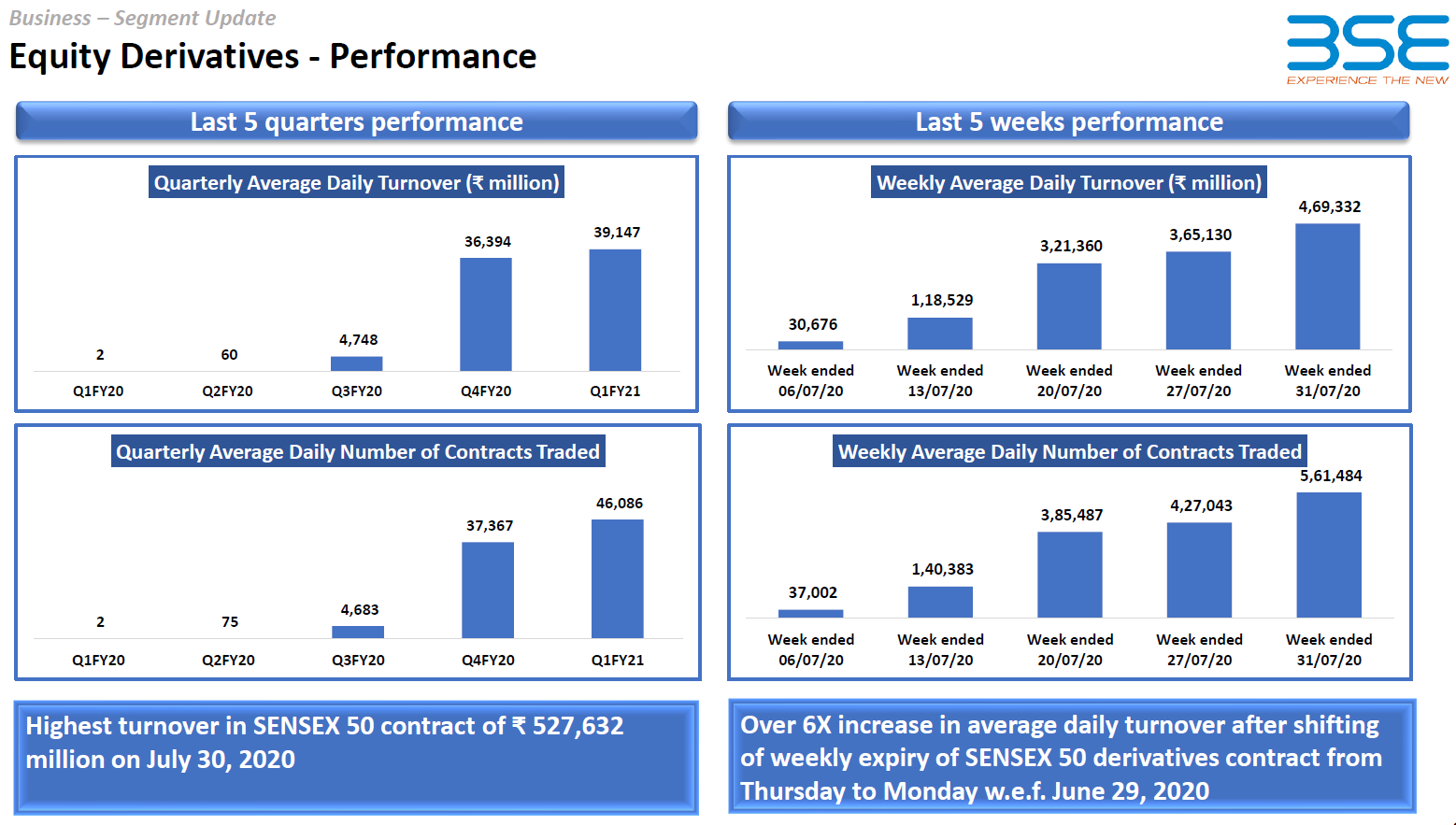

Equity Derivatives

Default preference by brokers has been removed in favor of best price. Should help in growth. Change weekly expiry to Monday from Thursday. Has lead to transformational increase in ADTV. ADTV has increased to 26196 cr in July. ADTV for Q1 was 3724 cr.

Basically, there are several aspects to this. One is, earlier also we had some liquidity enhancement schemes but not much volumes were there. The current scheme is also not significantly different in terms of monetary payout vis-à-vis what earlier was there. Only thing is that we change the index to Sensex 50, which is closer to Nifty 50 by 200 -300 points. The difference is not very high and co-efficient of co-correlation also is very, very good. So, because of that probably and second is that we have changed the expiry, weekly contract expiry to Monday instead of Thursday, which was basically both were ‘me-too’ contracts in a way, this will become slightly off sited contracts. And these two reasons might be the reason but one never knows how this thing happens in terms of if we reduce or if we take away the liquidity enhancement scheme will this volumes continue it remains to be seen but there are other ways to monetize once the volumes pick up and more and more people come to BSE for trading on derivatives.

It’s largely it’s almost the entire things is index options and the income are zero because we don’t charge in the sense, we also pay for order flow. So, before you, the person asked question on the liquidity enhancement scheme that is basically payment for the order flow and so it’s a little bit of investment we are making, in making people give two way course in market that is another thing and that’s where basically we are not currently earning anything from the equity derivatives market.

In a way Sensex 50 has as a pretty much similar number as Nifty. And that’s why probably people are also using it to move from one settlement to another because NSE has a Friday to Thursday settlements, and BSE has like Tuesday to Monday settlements. So, because of that people take position in one and go into another when the settlement comes in, so on and so forth. So, that seems to be happening and that’s why BSE’s volumes in Sensex 50 have increased pretty much today also it costs Rs.60,000 crore in notional value. So, it looks as if that seems to be the case, but you never know what is happening.

So, we appreciate your reasons and all and we’ll take up with Zerodha also. And sometimes what happens is, the parents have a lot of hope on one child which is very bright, but the second child who is ignored starts doing well and parents still keeps on putting a lot of money into the brighter child who may not be able to earn much. So that’s instead happened with us, Sensex we have spent a lot of time, but Sensex 50 we didn’t spent and suddenly it has become successful. So, sometimes on our expectations are on one person and the other person starts doing well all these things happen, life as it comes. Of course, we must put money into the brighter child also which will continue to do. But if Sensex 50 is also becoming successful, we shouldn’t try to stop it from being successful. So, we’ll take up with Zerodha and other brokers to allow you to trade there also on Sensex 50.

Power Exchange

BSE stake is 41.08% through BSE investments LTD. Have to reduce to 25% post receipt of license.

Basically, CERC has an approval process by which they allow people to raise objections and the competition in this field, Indian Energy Exchange and Power Exchange of India Limited. Both had raised their objections which were being heard over last two years almost. And now, the CERC has given a framework by which we have to comply with the regulation for shareholding within max eight weeks by which, after which they will again take up the matter.

Yes, electricity futures is what I think you mean. And as and when the regulations are framed by SEBI certainly BSE would try to also be in that market

SGF

Interoperability among clearing corporations was implemented from June 2019. After implementation of interoperability, the members have the option to choose the clearing corporation to clear their trades. Based on their selection, the trades of BSE are cleared by respective clearing corporations. As per Regulatory requirements, BSE needs to contribute to Core SGFs of all the Clearing corporations through which its trades are cleared. BSE has already contributed ₹ 153 crore to Indian Clearing Corporation Ltd., which is in excess by ₹ 123 crore as compared to the requirement, as of 30th June, 2020, of the above mentioned circular relating to Core SGF. Based on the transactions executed on BSE and which are cleared by other Clearing Corporations, BSE’s requirement to contribute to Core SGF is ₹ 18 crore as on 30th June, 2020. The Board of the Company has represented SEBI to allow utilisation of excess contribution by BSE lying with ICCL to the requirement of Core SGF contribution to other clearing corporations. The Company have also represented to SEBI that the contribution by exchanges towards Core SGF of clearing corporations may be allowed to be contributed in the form of Bank Fixed Deposit / Government Securities. The Company is awaiting approval from SEBI in this regard. In view of the above, no contribution has been made to other clearing corporations and the Company has not taken any charge for the contribution to Core SGF in the current quarter’s statement of profit and loss.

As on 31st July, 2020, the total balance lying in Settlement Guarantee Fund maintained by Indian Clearing Corporation Ltd is Rs. 441 crore of which, as mentioned above, Rs. 153 crore has been contributed by BSE.

And as far as CORE SGF is concerned, we have not contributed anything for standalone in this current quarter. However, ICCL has contributed about 6 crores from their standalone books towards SGF.

DEBT

So, do you think this, the debt platform the BSE bond, the commercial paper, and all the platforms together are the next closest to being monetized among all the optionality’s that are there in BSE right now?

In a way Yes. But what we have observed also is that NSE is able to basically cut the prices where they are losing, especially new markets, and also spoil the monetization opportunities for other people also. So somewhere on the line where cross subsidization is basically hurting the entire market everywhere. And so, it remains to be seen how we are able to basically monetize despite very, very strong, anti-competitive, what I call unreasonable competition, and the complete emulation of prices by the sort of incumbent in other businesses.

Commodity Derivatives

So basically, in commodity derivatives contrary to your perception now we are the second largest commodity exchange in the country. And the third largest exchange is around 25% of our volume or less. Second, basically what had happened is recently SEBI allowed options in goods. Earlier, the options were allowed on the futures, now they’re allowed on the straightaway, the underlying like gold and silver and all. We have launched those contracts and we have seen quite a lot of traction. Even if you see overall the STT options is pretty much around on a notional basis around 1 or 2% of the future. So, people prefer a trading in options in even securities market and we believe that because the differentiator in the CTT is also equally bad. And that’s why people may finally move towards commodity options and not futures. And that’s where currently we are the largest marketplace for commodities options in India and the second largest overall for the notional value. So, this is just basically for your understanding that your perception was wrong.

Sir also to give a perspective about the options on goods contract launched on the BSE and the gold mini there is a 100 grams contract today, at this point of time month-onmonth BSE has 58.8% market share as far as the Gold mini contracts are concerned.

Yes so, for the commodities today at this point of time BSE is 7.42% as-far-as the entire commodity market share is concerned and it is the second largest exchange for commodities, it is grown as the second largest exchange with commodities. In fact, this is I am talking about the overall commodity basket but if you specifically see after the product in the gold itself at the entire product basket gold it is 22% and for the gold mini which we have launched the gold mini options on goods contracts where we have surpassed the competitive exchange also, we are 58% there.

DMA

It remains to be seen whether it will be allowed or not, but if it has allowed them BSE has a much better system to handle all that.

Misc.

Cash is 1400 cr. No buyback proposal currently. Have already returned 1277 cr in last 4 years. Consolidated net cash will be Rs.1600 crores

So, Pritesh when you say other operating income it is basically the income which is with respect to certain ancillary support services in consolidated it would mean some amount received towards MTPL income from our IT subsidiary, then certain training income from our education subsidiary BSE institute and which are basically subsidiary income and not related to exchange, but they are operating because they’re consolidated.

In this quarter, the income which we have booked that is on the equity segment turnover, in last quarter we had few transactions in physical settlement where our charges are high. When we do physical settlement, and our transaction charges were high, and our income was more than Rs.6 crore last year. SEBI said to stop physical settlement and there should be only Demat settlement so after that the physical settlement was stopped. And if you remove the Rs.6 crore of last quarter then you will see the difference and this quarter also has increased by 30%.