Just to revisit the story on how it is playing out after going through the latest concall transcript

Pros -

-

The latest quarter result is good. However, there is a cyclicality element as it is linked to the current bull market and/or corporate services like IPO,rights issues etc

-

The equity derivatives market share is hovering around 7% now. Thanks to expiry date of SENSEX50 to Monday as against expiry date of NIFTY50 on Thursday. This tactical move played out well. Eventually, it can result in moving equity cash segment market share upwards

-

Interoperability & Best Price Execution - Mr. Chauhan says he is trying and attributed some of the rise in the equity cash segment market share to interoperability in the recent concall transcript. He also mentioned about the “white lie” brokers were telling about adhering to the SEBI norms which eventually got exposed during NSE shutdown in February 2021.

-

CDSL turned into a great subsidiary and attracted the market. CDSL will have another opportunity waiting in GIFT City when India INX opens gates to global equities.

-

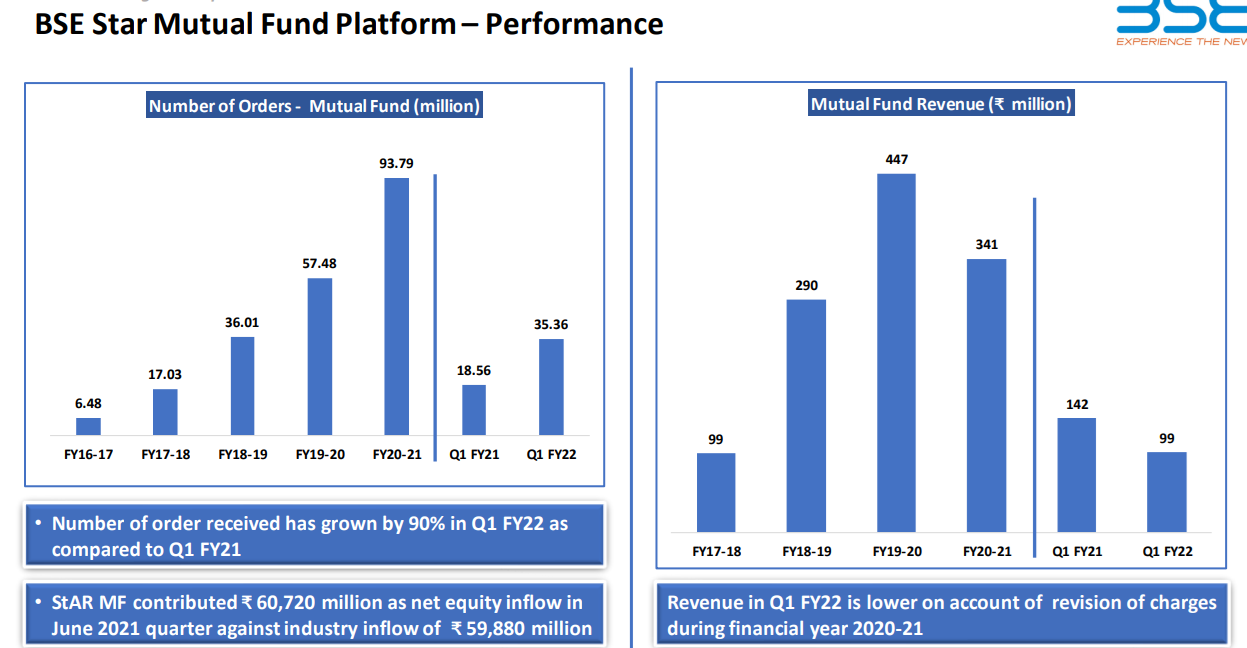

BSE Star MF continuous to grow. 90% YoY transactions growth. For now, it is getting inflows higher than industry inflows. In the recent concall, the CEO says, it has potential like CDSL. However, the pricing power is yet to be determined, as so far with increase in the transactions, there is also a lesser price negotiated with AMFI and Mutual Funds. The blended rate per transaction is 3.4 Rupees. For now, financial planners seem to be happy with BSE Star MF. Have to see whether it will emerge as a real moat.

- India INX is growing exponentially. 15 Billion dollars of trading is happening in the derivatives per day. There is a recent update about bullion exchange in GIFT city however, no clarity on how much India INX is going to benefit here.

In the below video, India INX CEO explains how they would like to position themselves as platform for all international broking firms/local broking firms/network service providers like TNS similar to a toll gate. Regarding the pricing, he explains that currently the brokers are charging around 2 to 5% transaction fee and India INX negotiated the pricing as 50 to 90% discount to the existing transaction fees.So, we can say this can help in finding true value of India INX.

-

Zerodha holdings currently have around 4% stake in BSE Limited as its only investment above 1% in shares. The discount broker increased the stake in past few quarters regularly.

-

Cash Balance of 2200 crores including its subsidiaries.

Cons

-

Have to reduce stake in CDSL from 20% to 15% by October 2021. At the moment, no clarity on how they are going to use the proceeds better compared to having stake in CDSL.

-

India INX CEO says, the global securities will be bought at the end exchange and so there is no difference in liquidity while accessing from say Exchange A in US and accessing it from India INX. So, if India INX ties up with NSE of US, it will be a network effect moat or else if it ties up with BSE of US, there will no liquidity advantage. This also leaves us with the doubt about how NSE IFSC is going to have the contracts with the global exchanges. At the moment, NSE is cash rich, it can afford to have some years of losses and can continue to play the unreasonable competitor.

-

BSE has always tried to increase the liquidity in its exchanges by using proprietary trading. We never really know how much is the real trading (without proprietary) in its market share of equity cash and equity derivatives. Especially, I don’t see SENSEX50 derivatives that popular.

-

In the words of Mr. Chauhan, it takes many years of losses to build monopolies. Here, in this context, we can read it about BSE Star MF and India INX. Not all can be CDSL. As the revenue from BSE Star MF decreased due to subsidized pricing, it can command less value as part of its monetization.

Overall, the story played out on expected lines. The market has so far rewarded most probably due to its stake in CDSL. It can throw a significant upside in case if any of these optionality plays out -

1)Increase of Equity derivates market share without proprietary trading

2)BSE Star MF getting good value discovery as part of its monetization. In the recent concall, it is clarified by the CFO that BSE Star MF is generating 10 cr operating profit(not revenue) per quarter where the lowest blended rate per transaction is considered. Considering that operating profit is 35% of net revenue in this case as per the call, the net revenue per year is coming to ~120 crores.

3)India INX taking charge as the gateway to access global equities and may one day route all the NRI investments to India. There is clearly a push to make GIFT city attractive.

Valuation

Cash - 2200 Cr

CDSL Stake - 1250 Cr (50% discount to current market cap)

BSE Star MF - 8 X 120 cr(Considering EBITDA as revenue and conservative industry multiple) 960 Cr

BSE building cost - 800 cr (mentioned by CEO in one of the concalls)

Current Market Cap - 5210 Cr

So, in short, all the other businesses are valued at 0.

Disclosure - Invested and biased

Portfolio - Southern_Cross's Portfolio - #22 by Southern_Cross