Britannia

Product Situation Analysis

They have been experimenting with new products and this may pay dividends in the long term. For example, they have released new variants of cakes, such as brownie and swiss rolls. Another approach is to classify some of the products as being healthy using market terminologies like whole wheat, nutrition enriched, etc. As more and more consumers start looking at health issues, these so called nutritious products may become a high margin and sought after products. Milkshake is another category which has shown to grow rapidly for other brands. Winkin cow is a new range from Britannia which may be released in certain regions to understand consumer preference. A nationwide launch will be a good boost to bottomline if it succeeds.

Two kind of products have worked for Britannia. 1) Nutrition focus and marketing done to make it appear as nutritious. Example is the nutri choice series with the latest being oats based. 2) Premium offerings such as chocolate based (and possibly milkshakes in the future) with a small size packaging. Britannia has already exploited the size of packaging to improve sales and margins. We may have to watch out for the milkshake category and also await any new offerings from the R&D expenses that were incurred in the past years,. While Parle was able to launch namkeens and snacks, Britannia has such opportunities to explore in the future as they have a vision to become a complete food company.

Water segment is fragmented and growth seems inadequate. Glucose biscuit caters to the lower income group while a product like nutri choice is well accepted by higher income group. The demand for cream and jam biscuits is not really big in both lower and middle income groups. Cakes is a good segment but the pricing is fixed at 10 rupees and nobody has pricing power. Britannia does have a lead in most stores. The products such as Nutrichoice, Bourbon, Marie, cake ranges are kept at eye level at most stores. Parle leads with hide and seek but misses out in the nutritional biscuit market.

Competitive Situation Analysis

Parle has been the primary competitor for many years. ITC and Unibic have been busy trying to have a similar product to match. The lower segment of products dominate the sales. The super premium offerings are only 6% of total sales as per Parle. Hence the market growth can be useful to offset the issue of competition. Parle and Britannia have very similar topline. When it comes to snacks, Pepsi, Haldirams have a lead and Parle is the new entrant. Britannia is planning to enter this segment in 2019/20.

Economical Situation Analysis

The overall growth of consumption is certainly increasing due to sheer size of population as well as affordability. The size of US biscuit market is 14 billion as of 2016. However India was at 4 billion. With a population to offset pricing, we certainly have room to grow. The penetration of premium biscuits is very low in rural and tier 2 cities. This will eventually change with rising aspirations of indian middle class in rural area. Hence the bottomline growth is possible along with the topline. The entire market is controlled by a very few organized players and hence growth will certainly flow to Britannia.

Technological situational Analysis

Britannia has started to focus on manufacturing and have moved away from contract manufacturing. This has given them focus on cost efficiency and control on quality. This can aid in increasing margins when fixed cost is offset due to huge volumes.

Demographic situation analysis

The consumption of biscuits have been increasing and there is a distinct shift towards products marketed as being healthy. This will help companies like Britannia sell their products at a higher margins by using health as a marketing tool. Since biscuits are common food that children are encouraged to eat, it has become a very powerful addiction without consumers realising it. These products could be the next big addiction after tobacco. Since these products have better shelf life and are not easily perishable, they are the best source of food for the busy modern world. Since it is an addiction picked up from a young age, it could be consumed across the various age groups. Since India has a demographic profile that favours young population, the growth of this industry may continue for at least 20 years.

Social and cultural situation analysis

Glucose biscuits have been marketed to appear as an aid in being healthy and energetic. Modern health marketing includes use of whole grain, multi grain, oats healthy, etc. These initiatives by the food industry have ensured that the consumer always keeps to snacking and biscuits over a longer term. Fortification of nutrients in biscuits have helped them to be marketed as healthy. These products can gather better margins and help us grow the bottomline.

Political and legal situation analysis

Government may impose regulations on sugar content and may force fortification with vitamins and minerals. These initiatives could further help Britannia market the product as being healthy. Since huge corporations thrive on processed and snack industry, governments may not impose any harmful regulations. Consumer activists are the only risk but they have not shown to focus on this segment.

Environmental situation analysis

Britannia’s growth depends on being able to offer unique products instead of me too products. Being first to the market has shown to help gain a thin moat. The R&D expense and the ability to deliver new products that add to bottomline and topline needs to be monitored. Dairy segment is well protected by players like Amul and hence Britannia may have difficult time to penetrate the market. However they could use unique products like biscuits to get in to chocolate based products. Snacking industry is another interesting place to be in as we have seen haldirams took a lead over pepsico by being relentless in releasing differentiated products.

Supply chain situation analysis

Britannia is now able to reach over 20 lakh outlets. This is still smaller than the overall market. There is room to grow. The hindi belt seems to be growing at 15% or more as per management. The saturation point certainly seems to need over 5 years.

SWOT

Strength:

The size of distribution seems to have a huge impact on topline for this industry. Since Britannia has not grown pan india, they still have scope to grow in the hindi belt. The focus on wide array of products and an Ex-Pepsico being the MD will help. Since the company already has the right ingredients to launch new products in dairy, cakes, and snacking, it is easy for Varun to prioritize growth for the next 10 years.

Weakness:

Britannia has been unable to increase the overall market for cakes even though they had launched new products. Creating a market for croissants may be a time consuming job. Hence the growth from some of these products may be slow although a product like brownie may be easier to sell. The biggest volume has been low margin biscuits where Parle has shown to be stronger than Britannia.

Past products which Britannia dominated, have become a commodity product. Bourbon is one example where company has to use the word ‘original’ to market it. Overtime these products will be commoditized and hence the only saving grace will be the R&D initiative to create new variants and successful products.

Exports have been limited to the gulf region, which is not growing due to slowdown. New business in Nepal and neighboring countries need to be evaluated. This weakness is also an opportunity if they can succeed in diversifying to other countries.

Opportunity:

R&D seems to be the vital tool to bring new products with higher margins or volumes. It was significantly increased from 2016 until 2017. However it was reduced in 2018 and no reason was provided. As expected, the fruits of these expenditure may take some time and the lag time may be up to 1 or 2 years. If we notice significant dips in R&D spends in future years and if it does not add to topline, we may have to reevaluate it as a risk.

Another opportunity is the revenue growth that has been lacking for last few years. Since biscuits are low ticket items, it is easy to grow volumes when economy is enriched to favour consumer spending. Since margins have increased in the last several years, the impact of revenue growth will be much pronounced this time.

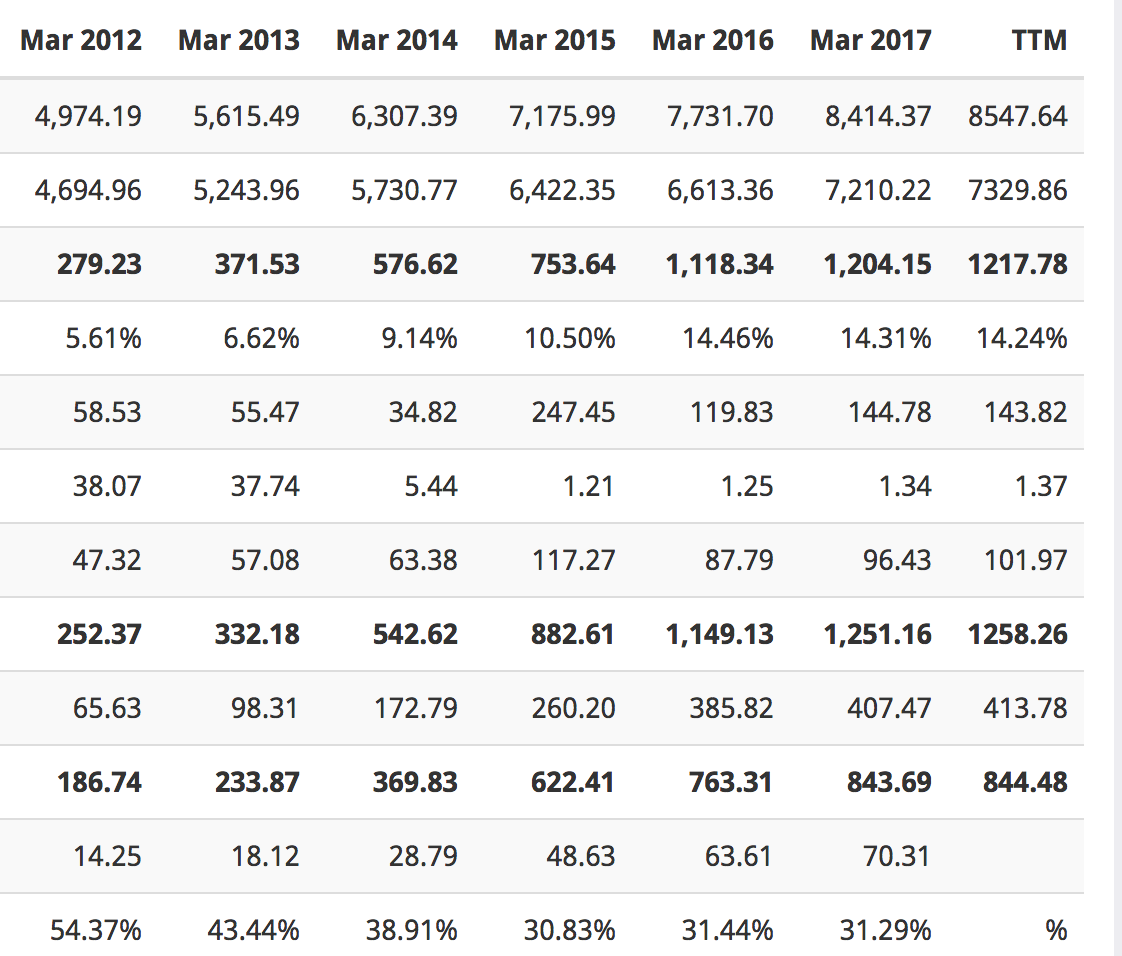

R&D Spends:

| Year |

Expense (crores) |

% of sales |

| 2018 |

28 |

0.31 |

| 2017 |

48 |

0.56 |

| 2016 |

44 |

0.54 |

| 2015 |

17 |

0.23 |

| 2014 |

10 |

0.16 |

| 2013 |

8 |

0.15 |

| 2012 |

6.5 |

0.13 |

Threats:

There is a threat of health conscious movements to stay away from sugar and calories. These are critical ingredients in biscuits and reduction or substitution may alter taste. Most of the awareness programs have failed in the west as seen from Atkins and Keto diets as they are not sustainable. Addiction of sugar has been more powerful than tobacco and this has ensured that substitution or replacement of these products are very slow. These awareness trends may last a short time but sustainability may be very difficult. Unlike tobacco industry which was shown to be harmful in a span of few decades, sugar may be harmful only after a very long time. This can help offset the risk of community activists in pushing governments to initiate regulations. It may be vital to monitor such threats closely to see if they can spearhead like the tobacco movement. Another major threat is commoditization of these products in the long run and constant need for innovation and R&D.

Issues analysis

The management quality is poor in terms of corporate governance. As of 2018, they had given 350 crores to Bombay Dyeing at a rate of 10% to 12%. Bombay Dyeing has very poor quality of earnings and getting 10% rate of interest for the deposit is in very poor taste. This constitutes more than one quarter profit after tax for Britannia. Hence it is significant and one needs to consider this attitude of management when we value this company. Although this is not severe, we may want to consider the risk of future inter corporate transactions which may be against the interest of minority shareholders. We may have to track this on an ongoing basis to see if the unsecured deposits in these poor performing companies are within a certain limit.

Deposit with Bombay Dyeing

| Year |

Amount (cr) |

| 2015 |

175 |

| 2016 |

125 |

| 2017 |

350 |

| 2018 |

350 |

Bombay Dyeing earns less than 35 crores PAT and is being offered a deposit of 350 crores for this company with a market cap of less than 2500 crores shows very poor risk management and corporate governance.

Important items to look for:

- Sales of vital products such as Deuce, winkincow, Nutrichoice range, cake ranges.

- Inter corporate funding and any mis handling of capital allocation.

- Ability to expand outside India

- R&D expense and outcome

Disclosure:

I hold Britannia for a long time and I am adding to it at current levels too.

.jpg)

.jpg)