For that kind of complaint there is consumer courts ..no ?

Also, the visa issuing authority provides the contracts to BLS which they have to win by Tender method. Indian gov does not control this mechanism directly .If an Indian citizen wants to visit france , its France who issues visa and is using BLS as a service provider and gives the contract . BLS is not dependent on Indian gov that much for Indian visa either since VFS and others already get to bid for those tenders .

Ofcourse, BLS may lose contracts if the service is too lousy or too problematic for visitors..but one would guess that they know just how much they can get away with as does their competitors .

2 Likes

@nav_1996 the site you posted shows this. please dont post links which can cause issues.

5 Likes

Today. Protean’s news shows B2G risk. That is the reason I mentioned that terminal value is at risk when monopoly is granted by govt and service is poor and customers are desperately waiting for an alternative.

3 Likes

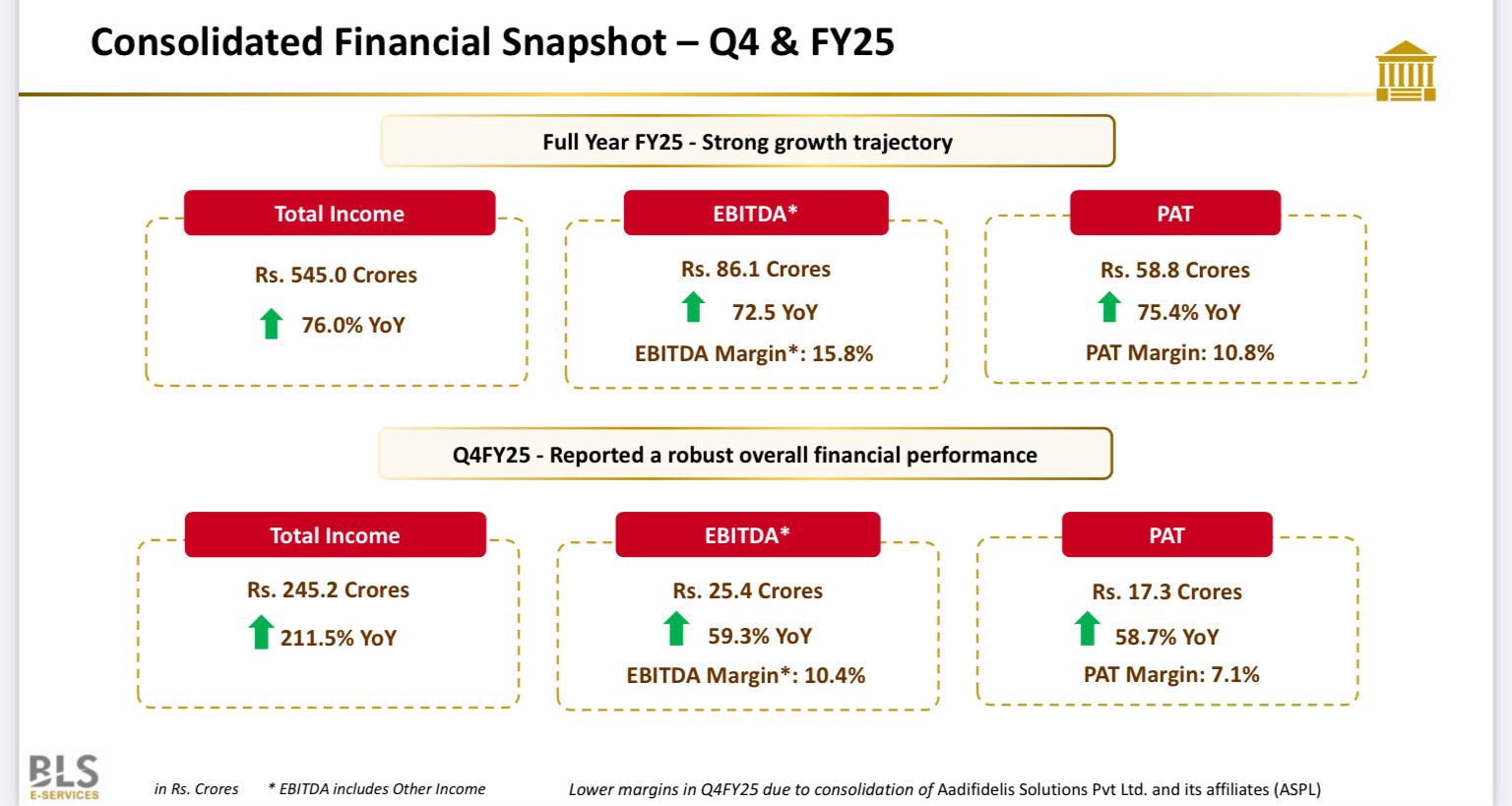

The company’s listed subsidiary BLS E-Services has posted very good results in last quarter

Disclosure: Invested.

5 Likes

I think the company has tie up with other country Gov also so there is no concentration of revenue from India Gov. As per concall, Management is good and also they think about it and act accordingly.

3 Likes

Nuvama’s note on BLS.

The gist:

" BLSIN delivered a solid performance in Q4FY25, exceeding our estimates and achieving its highest-ever quarterly revenue. The outlook for coming quarters appears encouraging due to i) seasonal strength in visa processing volumes and ii) the transition of high-potential geographies from partner-led to self-owned models. Expansion in the visa and consular business is expected to aid margin recovery from a base of Q4FY25. Visa contract wins and expansion of the digital services platform can enhance profitability. The management’s track record of successful strategic acquisitions has expanded its addressable market and strengthened its service offerings. Given its outperformance in Q4FY25 earnings and steady growth momentum guidance, we leave unchanged our estimates and maintain ‘BUY’ with a SoTP-based TP of INR637."

BLS International_Nuvama.pdf (2.1 MB)

12 Likes

Business Line, 02-Jul-25. Link.

Global visa outsourcing market

- $2 billion worth of tenders opening up

- BLS plans to bid for $1 billion in coming months

Outsourced visa market

- $1.7 billion in 2024

- to $3.2 billion by 2029 from.

- Growth: 14% pa

- BLS market share 17%

Global visa market

- $5.4 bn in 2024 [i.e. 31% outsourced]

- to $7.7 billion by 2029 [i.e. 42% outsourced]

- Growth: 7% pa.

Tourist visa segment: 70% by 2029.

Other segments – study visa, business visa and work visa – expected to shrink.

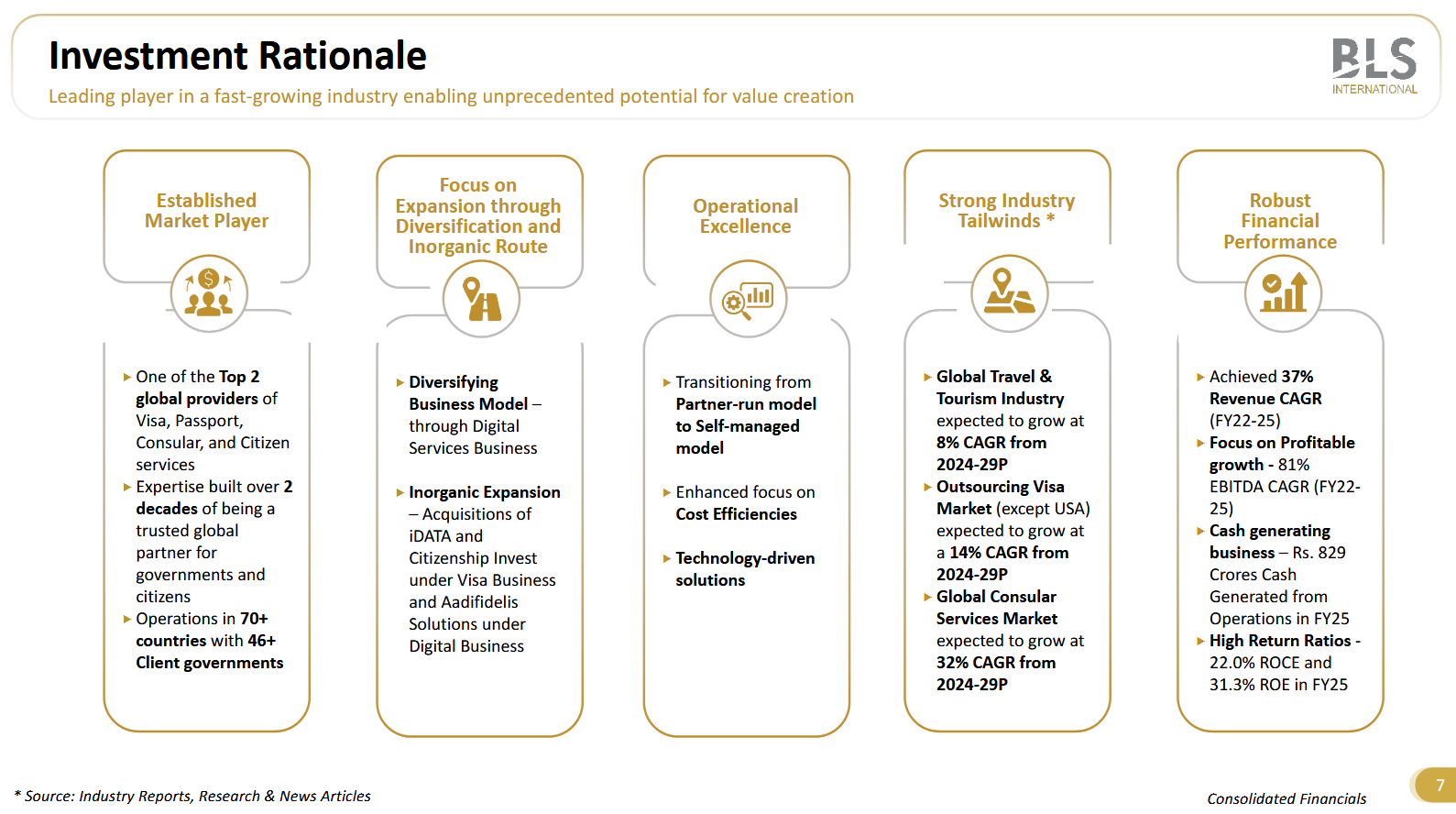

BLS confident of sustaining a 20–30% pa growth in the coming quarters.

Business model is resilient:

- services are essential

- government-authorised

- and user-pay in nature.

Relatively insulated from broader economic cycles and geopolitical headwinds (Disagree. Will be impacted by geopolitics).

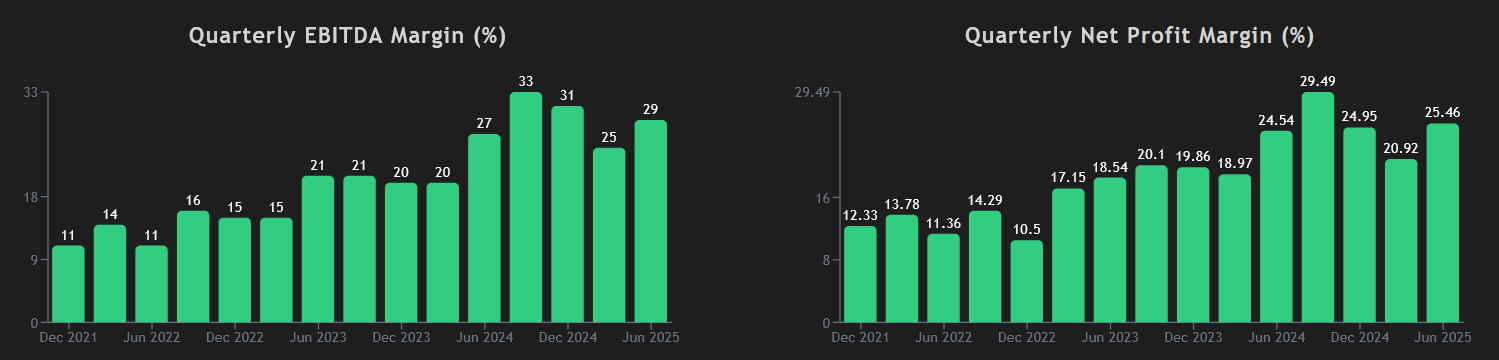

Pre COVID-19 profitability - ₹100 crores.

FY24 - ₹350 crores of net profit.

FY25 - ₹539.6 crore.

₹1,000 crore net cash on books

Pursuing both organic (tech and AI) and inorganic (M&A) growth.

3 Likes

Despite of a good business model and attractive valuation the company is not finding significant institutional buyers.

4 Likes

The growing trend of offering visa on arrival won’t have an impact on it’s business?

https://www.bajajfinserv.in/insurance/visa-on-arrival-for-indians

2 Likes

To elaborate your last line and sync with concall abstracts Page 8 of 15:

Question: we are holding some INR 900-odd crores of cash in our balance sheet. And we have done pretty decent acquisitions in FY '25. So what are our plans of utilizing this cash going forward? How we are planning for that?

Answer: See, if you see last year, we’ve done INR 1,000 crores plus acquisition and we’re also a dividend paying company. This year also we have paid 100% dividend on the face value we have announced. So I mean, this is a cash-generating company. It’s a negative working capital

business.

And as we grow, we generate more amount of cash. We are seeing effective ways of

utilization. Acquisition was one. Dividends we’ve been paying. We are investing on different resources, growth of the company, getting good quality people, spending some on technology,capex, etc. So going forward, I think the growth that we foresee in terms of new contracts coming in, etc.,

some cash will be utilized in that. We are reinvesting in improving our offices, technology, etc. And also, we are again open once the acquisitions that we have done, the synergies properly kick in, we are open to more acquisitions in the future as well.

8 Likes

LIC increases its stake in Q1FY26. Hopefully more institutions to follow and take notice after this set of good results.

7 Likes

Despite of the good result why the stock price is not moving. Am I missing somthing? Or it is because of market not performing well.

1 Like

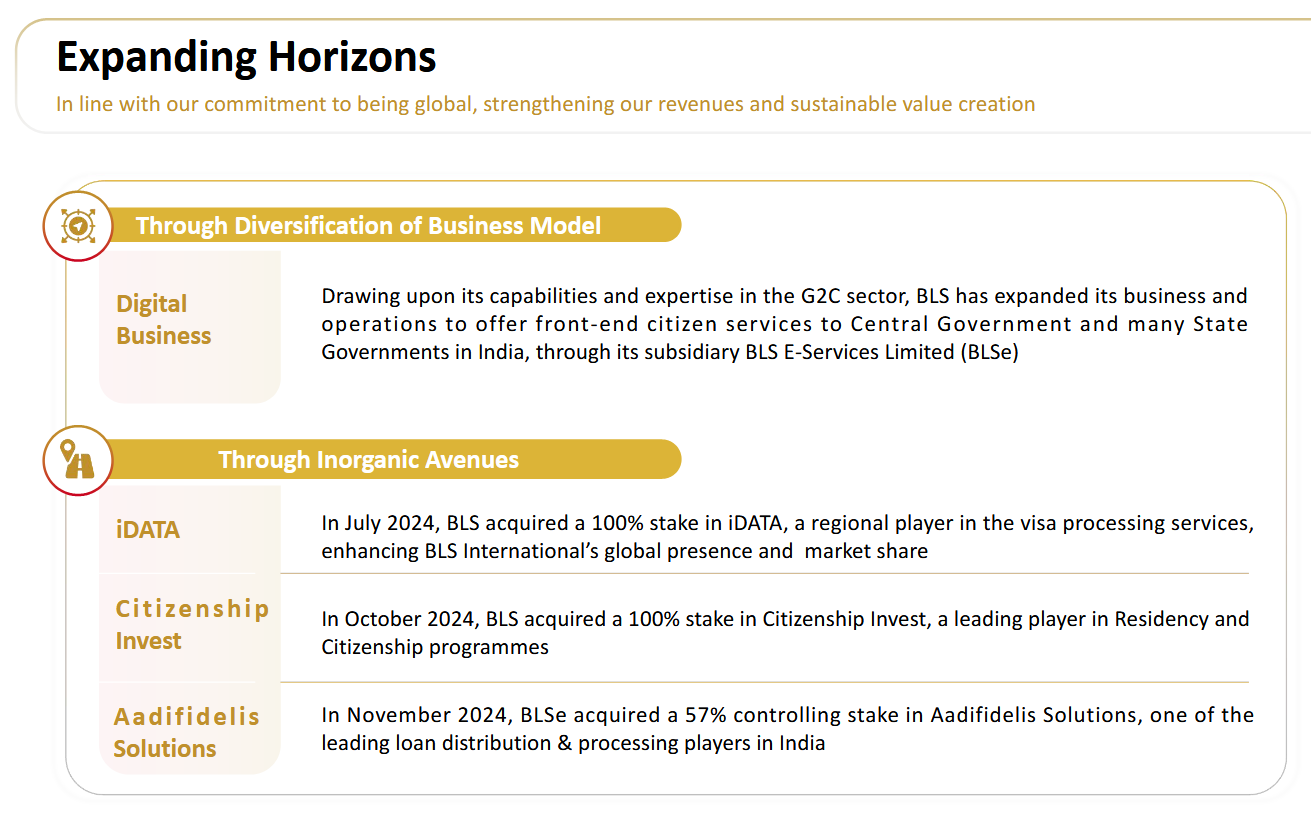

I am not invested but was quite interested, because I couldn’t understand some of their acquistions especially Aadifidelis, felt diworsification. moreover stock doesn’t have any institutional money interest. I feel a good re-rate could happen when they eat share from VFS or VFS listing could potentially trigger a re-rating.

2 Likes

The Aadifidelis acquisition was made through BLS E-Services, which is BLS International’s digital business arm. So, rather than being a diworsification, it actually aligns with their existing secondary business vertical.

In my view, real money is made by identifying opportunities before institutional investors step in. While institutional interest can certainly reinforce conviction, when multiple institutions are already on board, I often see that as a sign that the early, high-upside phase has passed.

Disclaimer: Invested

7 Likes

I agree Shane. Even in the analyst call someone suggested MD to increase PR, attend investor meets to attract flows. I feel thats “Stupid” (Apologies for selection of the word but cant find better substitute ;-) ). Company is in high growth phase. Sit tight and keep accumulating

3 Likes

I read multiple posts above saying institutional investors are not interested/invested in the company. Shareholding pattern has ~11.3% institutional holding already. Are we expecting more institutional holding than this? Or is it about the name of institutes like MFs etc which are missing? Only few foreign based funds and LIC are current owners

1 Like

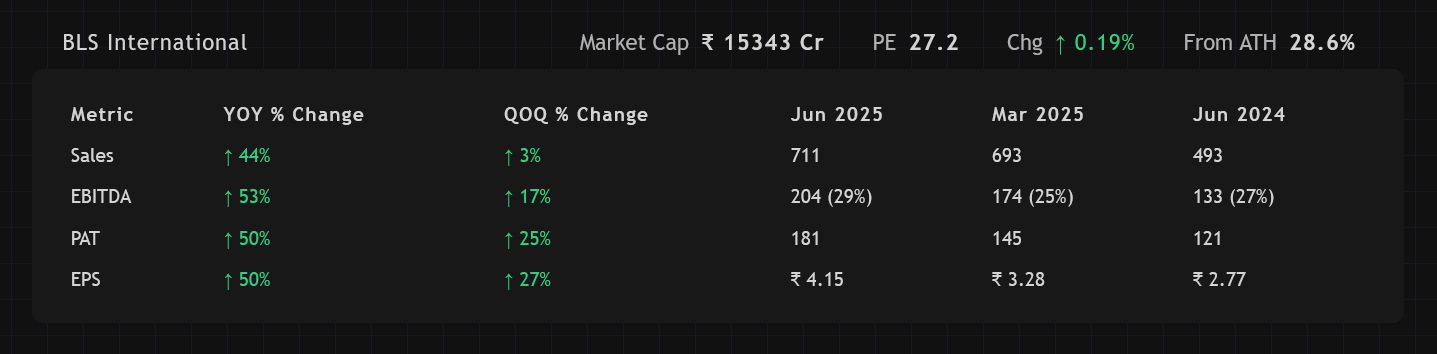

- BLS International reported consolidated revenue of ₹710 crore in Q1 FY26, up 44% YoY from ₹493 crore, driven by visa/consular services (+11%) and digital services (+218%).

- EBITDA grew 53% YoY to ₹204 crore with margin expansion of 171 bps to 28.7%, reflecting improved operational efficiency and cost management.

- Profit after tax (PAT) surged 50% YoY to ₹181 crore from ₹120 crore, with earnings per share (EPS) rising to ₹4.20, a 50% YoY increase.

- Visa applications processed rose 33.6% YoY to 11.40 lakh in Q1 FY26, supporting volume growth in core services.

- Digital services revenue reached ₹250 crore, more than tripling, underscoring strategic focus on diversified service offerings and future growth avenues.

- Company now operates in over 70 countries and serves 46+ client governments, signaling strong global presence.

- Recent acquisition of CSPs (Customer Service Providers) including Citizenship Invest enhances service portfolio and market position.

- Transitioning from partnership to self-managed centers globally, improving margins by eliminating partner commissions but increasing employee/admin costs.

- Strong net cash position of ₹1,100+ crore, with M&A pipeline active but no imminent acquisitions disclosed; focus currently on consolidating previous acquisitions.

- Competitive edge comes from extensive industry experience (15-20 years), proprietary technology platform, delivery track record, and strong client government references.

- Management guides for 20-25% growth over next 2 years, driven by expanding visa/digital services and technology-driven innovation.

- Industry outlook described as transformative over next 5 years with focus on AI, tech upgrades, and expansion into new citizen-centric government services like driving licenses and utilities.

1 Like

Nothing to add about the business, but why the stock isn’t reflecting the growth.. now I think it’s almost 1.5 years the stock is trading in a range.. This might happen to any listed company.. and all of a sudden the market might reward..

But I think in this counter there are lots of trading happening.. always I can see around 10L buy orders which is very high.. and I am closely following the stock for last 6 months..I think this might the hangover of previous performance..but not sure.. just my observation..

6 Likes

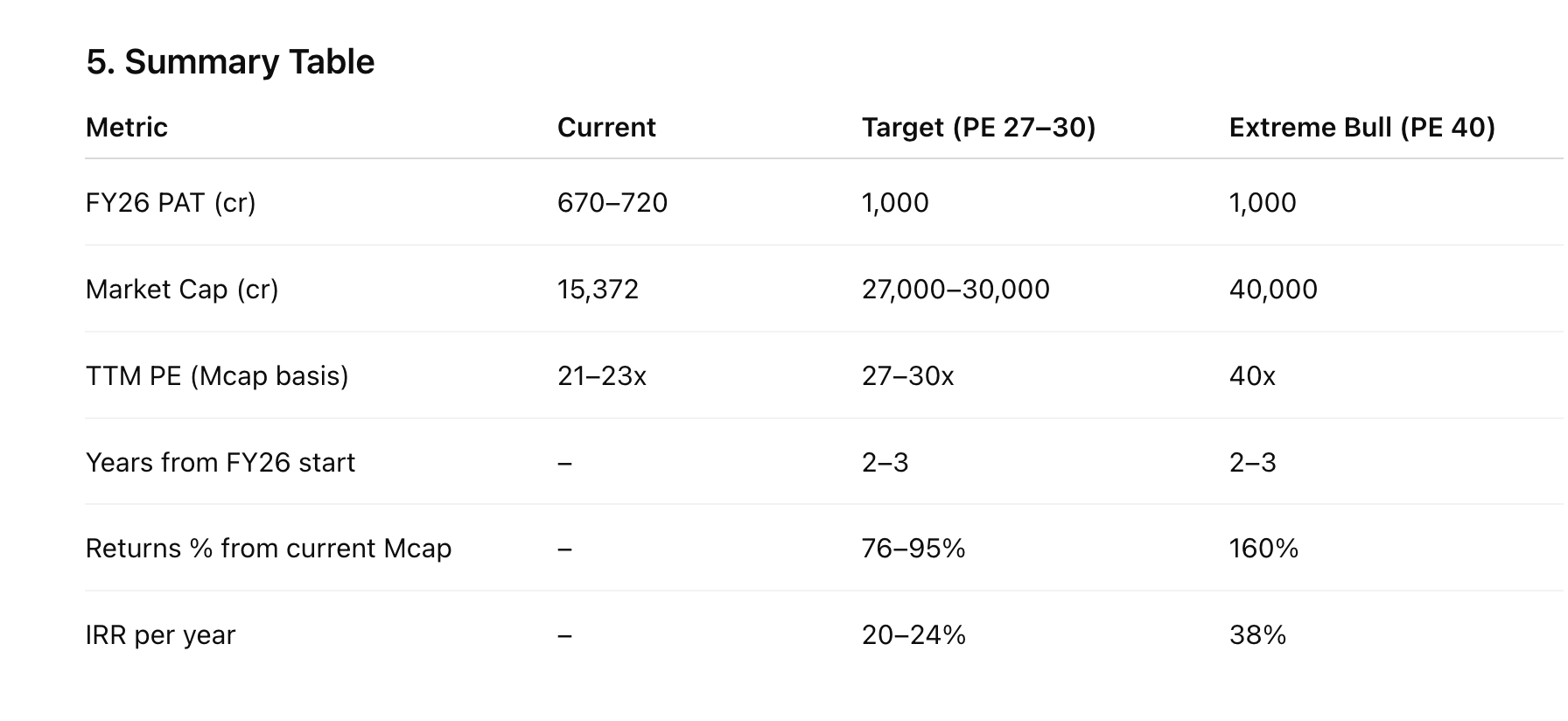

You’re right, it makes complete sense. Previously, I was concerned about peak margins, but they’ve been able to sustain them. After reading more about BLS, I believe that as long as earnings growth continues, the company could reach around ₹1,000 cr PAT by FY28, with a potential PE of 27–30. I’m also attaching my earnings growth and PE estimates based on 20–25% growth for reference.

I would continue to track growth and OPM closely, but it seems like a strong opportunity. Regarding my earlier concerns about the PE re-rate when it eats more from share, as long as earnings remain on track, it could still be a good compounding stock, and any re-rating could create asymmetric upside. also would track acqusitions as well

disc: invested and biased

5 Likes

Q1FY26

Result:

Concall Notes:

- Processed 11.4 lakh applications, a 33.6% YoY growth.

- Visa and Consular segment revenue grew 11% YoY to ₹461 crores, with an EBITDA margin of 40.4%.

- Digital Service segment revenue surged 218% YoY to ₹250 crores.

- Margin Profile:

- Visa & Consular Services: 40.4%

- Digital Services: 7.2%

- Visa segment margins (around 40%) and consolidated margin (~28–29%) will be maintained going forward.

- The Digital segment’s margin is diluted by the Aadifidelis acquisition (4% EBITDA Margin)

- Management views IPO of VFS as positive as it might create more analyst coverage of the space.

- Only 50% of the global visa market is currently outsourced, leaving significant room for growth.

- New tenders are coming up for renewal, and new governments are outsourcing for the first time.

- The company is working with over 40 client governments in more than 70 countries.

- The company has successfully penetrated the Schengen government contracts, working with Italy, Germany, Spain, Czech Republic, Portugal, Poland, and Hungary.

- The company has a net cash position of ₹1,126 crores as of June 30, 2025.

- The company has a dividend policy of paying up to 30% of profits and has been paying dividends since listing.

- The growth strategy involves expanding through key government partnerships and diversifying offerings into citizenship, residency, and entry services.

- A strategic acquisition by subsidiary Zero Mass is underway to acquire CSPs of SBI and HDFC Bank from Sub-K IMPACT Solutions.

- The company is actively bidding on a multi-billion dollar pipeline of new tenders and renewals.

- The business model’s growth is led by both existing business and the full-quarter consolidation of iDATA, Citizenship Invest, and Aadifidelis.

- The transition from a partner-run to a self-managed model is nearly complete, with the last major conversion, China, completed in Q1 FY26.

- The company has achieved a global market share of around 16%-17%, making it the second-largest company globally in this business.

- The business is focused on execution, with a track record of 5x revenue growth and 15x EBITDA growth over the last 5 years.

- All offices are operated on a rental basis; the company does not own property assets.

- The company expects to continue growing at 20%-25% in terms of profitability and revenue over the next 3-4 years.

- 90% of contracts were renewed in the last year, providing clear revenue visibility for the next 4-7 years.

- The global visa outsourcing market is projected to grow at a 14% CAGR and reach USD 8.2 billion by 2028.

- Margin improvement is a result of operational leverage, continuous focus on cost optimization, and the transition of self-managed centers.

- The company deployed ₹1,200 crores last year and is actively looking for more acquisition opportunities.

- Inorganic revenue growth from acquisitions was about 35% YoY. Margin expansion is due to shifting to the self-run model, where the partner’s margin is now captured by BLS.

Shareholding Pattern:

Disclaimer: Invested

8 Likes