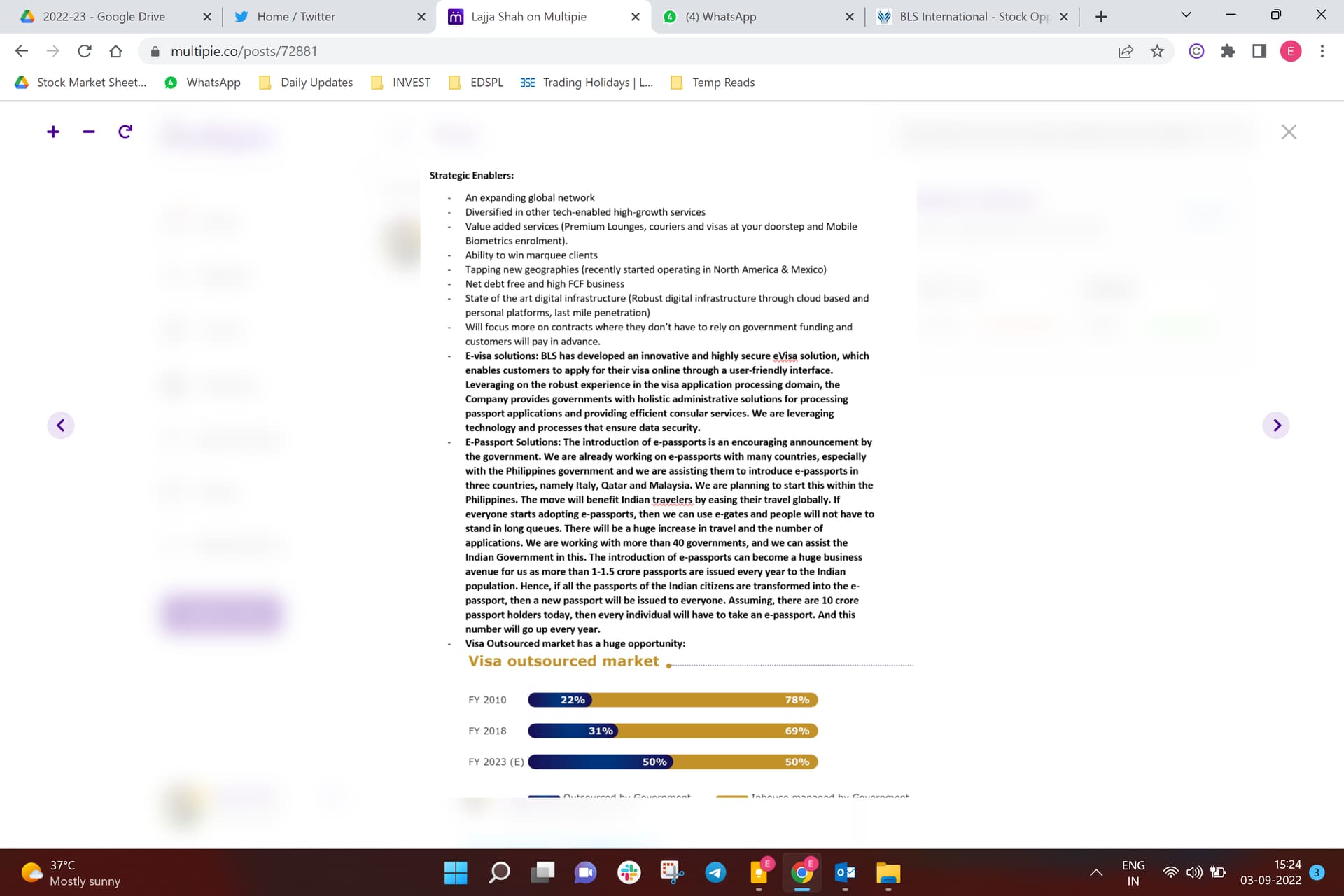

Explained: What Are EPassports And Why Is India Set To Introduce Them Soon? …Will this help bls international to increase there revenue?

1 Like

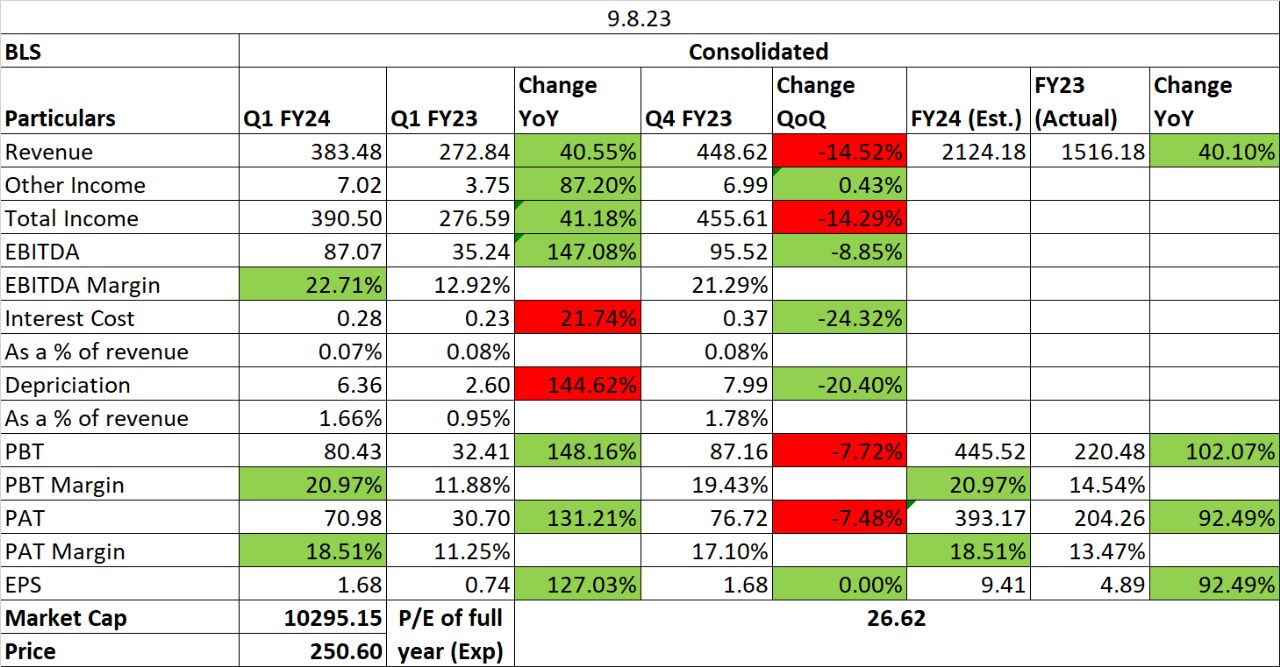

8a550530-17c4-4b8f-abd9-8c9c187711a3.pdf (bseindia.com)

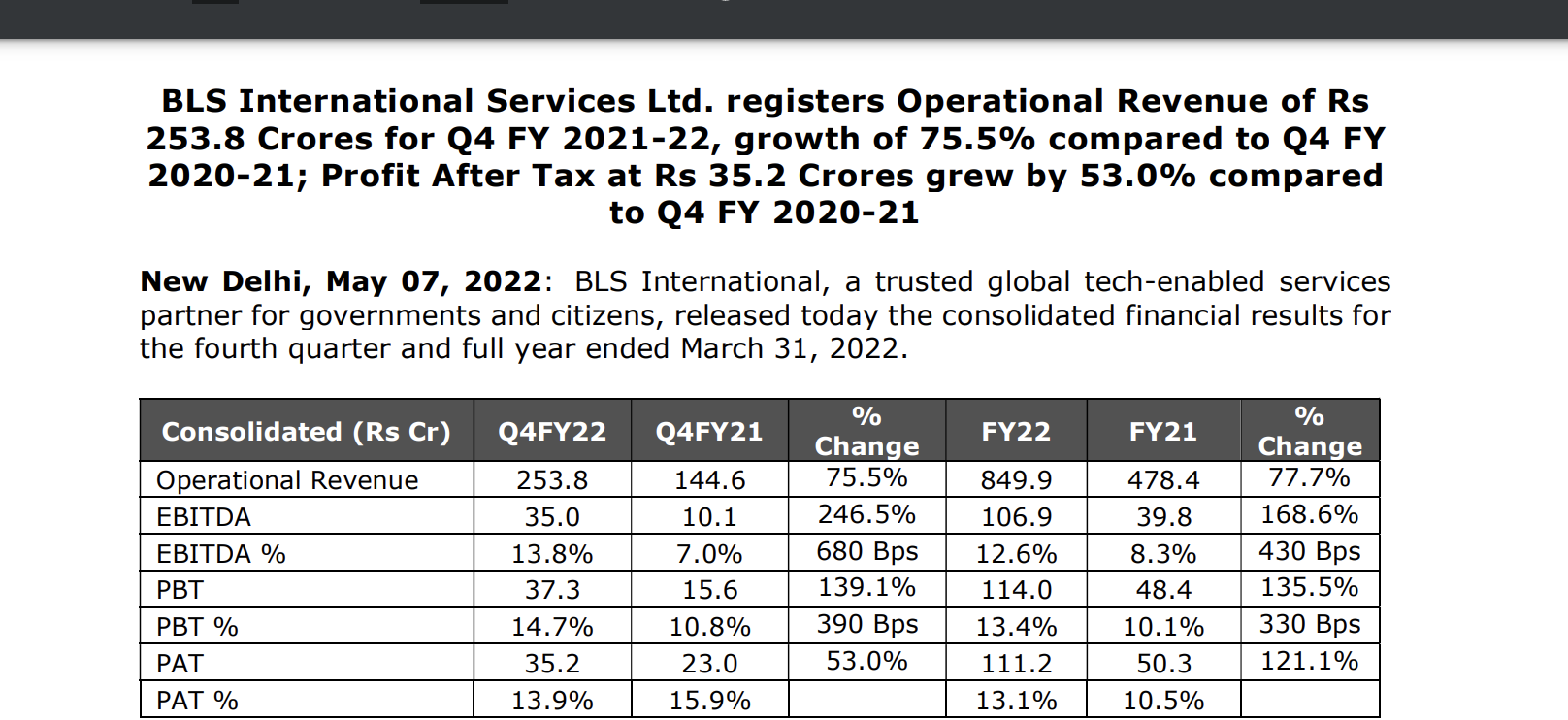

The company announced its results and investor presentation.

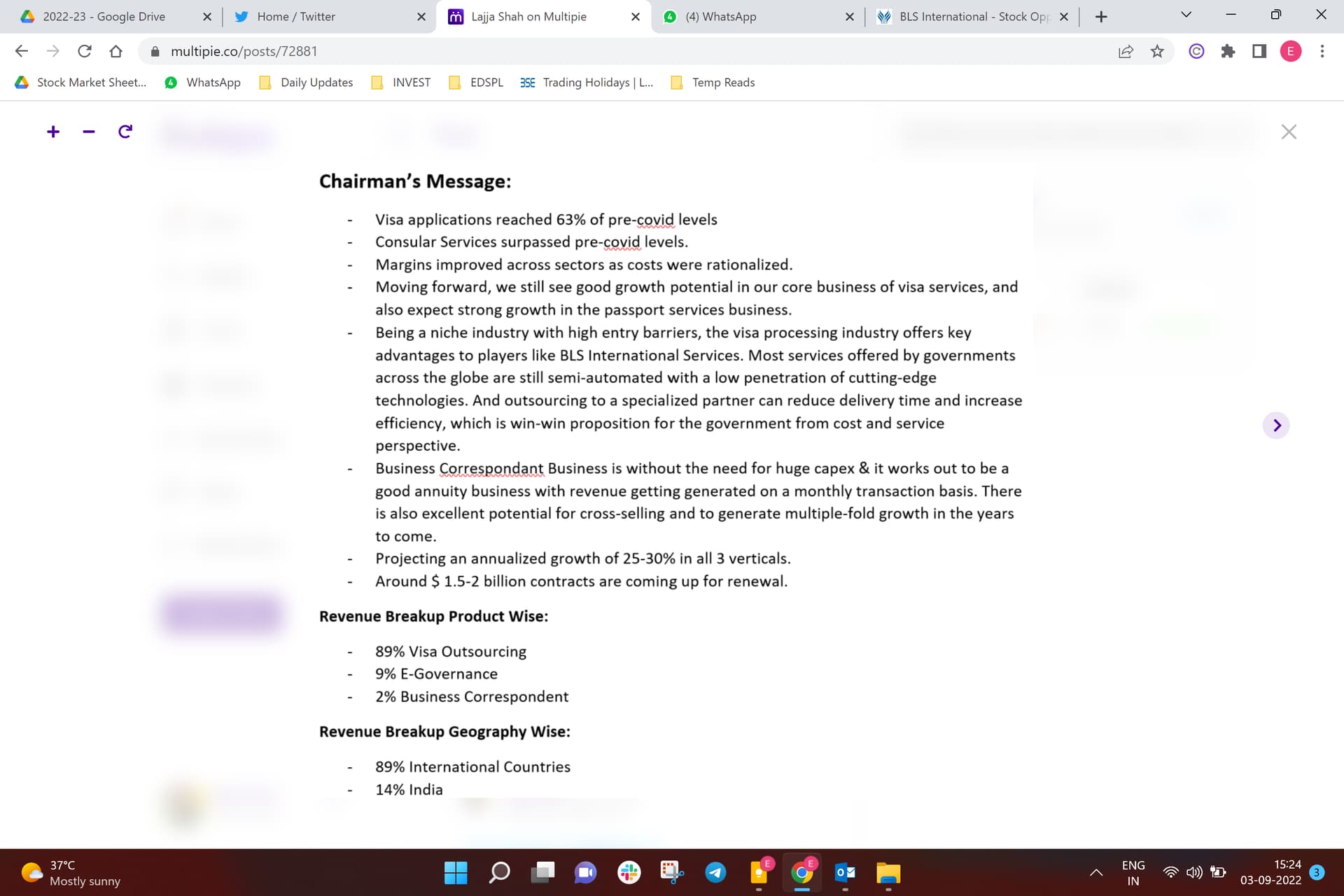

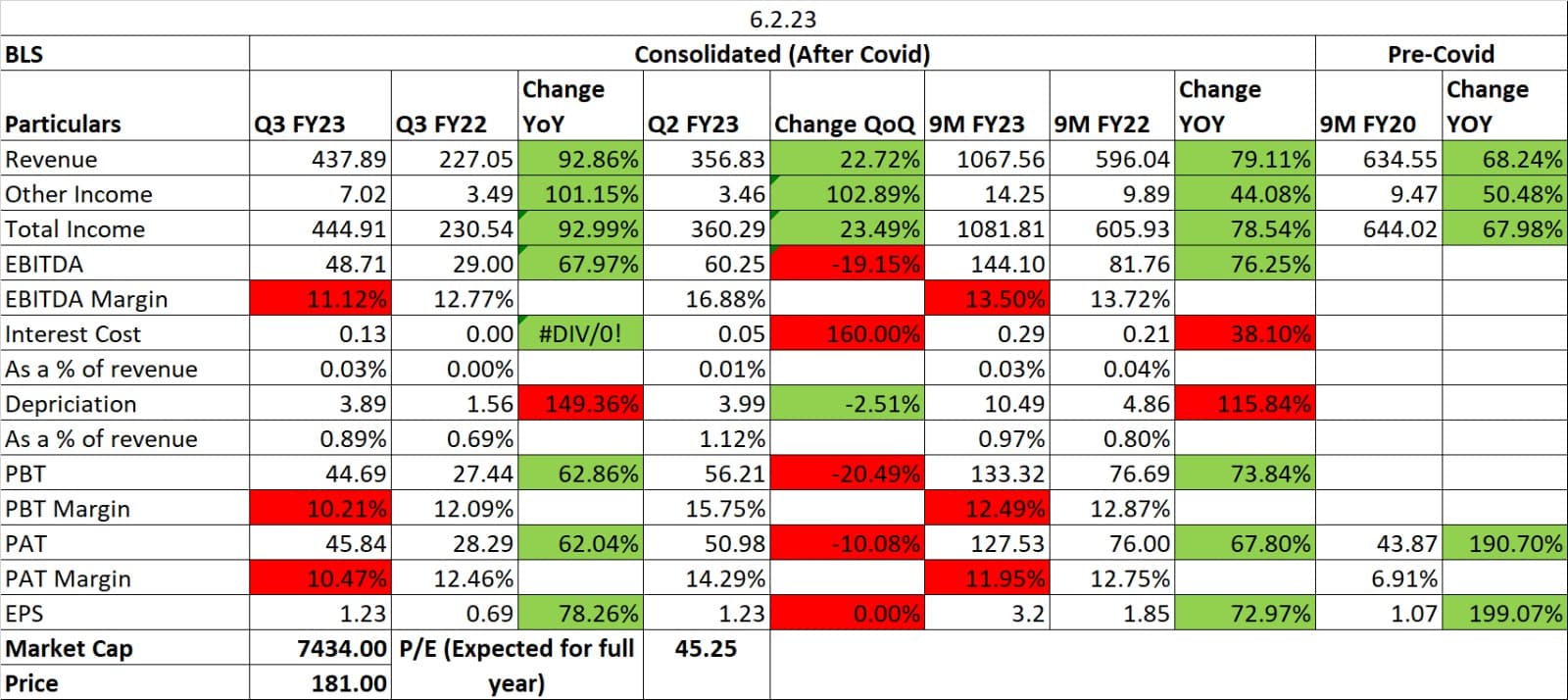

Debt is nil and holds 377 Cr of cash. After 2 bad years, it seems the profitability has returned to pre-Covid levels and that is pricing in the continual slump in visa consular division. Their other divisions have grown well in the meantime. OPM is low at 11% whose expansion should be a priority but hard to see how contractual nature of industry will allow that. Also, Valuation today is not that expensive but also not in any way cheap.

Given the events of past two years, it can be a good proxy to growth in international travel. Add to that there are 1.5 BN USD worth of visa contracts up for tender next 2 years. Getting a small chunk of it can be great for it whose revenues are less than 500 Cr from this division alone. It is now in a better position to win some of those contracts as compared to five years ago.

Visa outsourcing is still 31% of overall market and it should also likely increase as countries try to increase travel applicants to stimulate economy. Europe has a good chunk of population reliant on tourism.

As noted, the business thrives on reputation and reliability. Each year they survive makes them stronger. A few marquee wins can help build credential for other global contracts.

Apart from the Visa division, its E-Governance division has grown well. Given the potential and scope of the business, it is a good optionality to bet on.

Business Updates for this quarter

• Renews contract with Royal Thai Embassy for visa services

• Signs contract with the Embassy of India in Kuwait for Consular, Passport & Visa services Other Businesses

• BLS International’s Starfin empanelled by Punjab National Bank & Central Bank of India for Corporate Business Correspondent

• During Q3 FY22, the company received a full and final settlement with the Punjab government for the old contract, with this old Punjab contract receivables of ₹ 67 crore are completely settled in the books

• Added Afghanistan, Estonia and Nigeria are key wins in addition to last mile connectivity for SBI in addition to Indian states

• The Company now has an extensive network of more than 12,287 centers globally with a robust strength of over 15,000 employees and associates that provide consular, biometric and citizen services. BLS has processed over 52 million applications till date globally

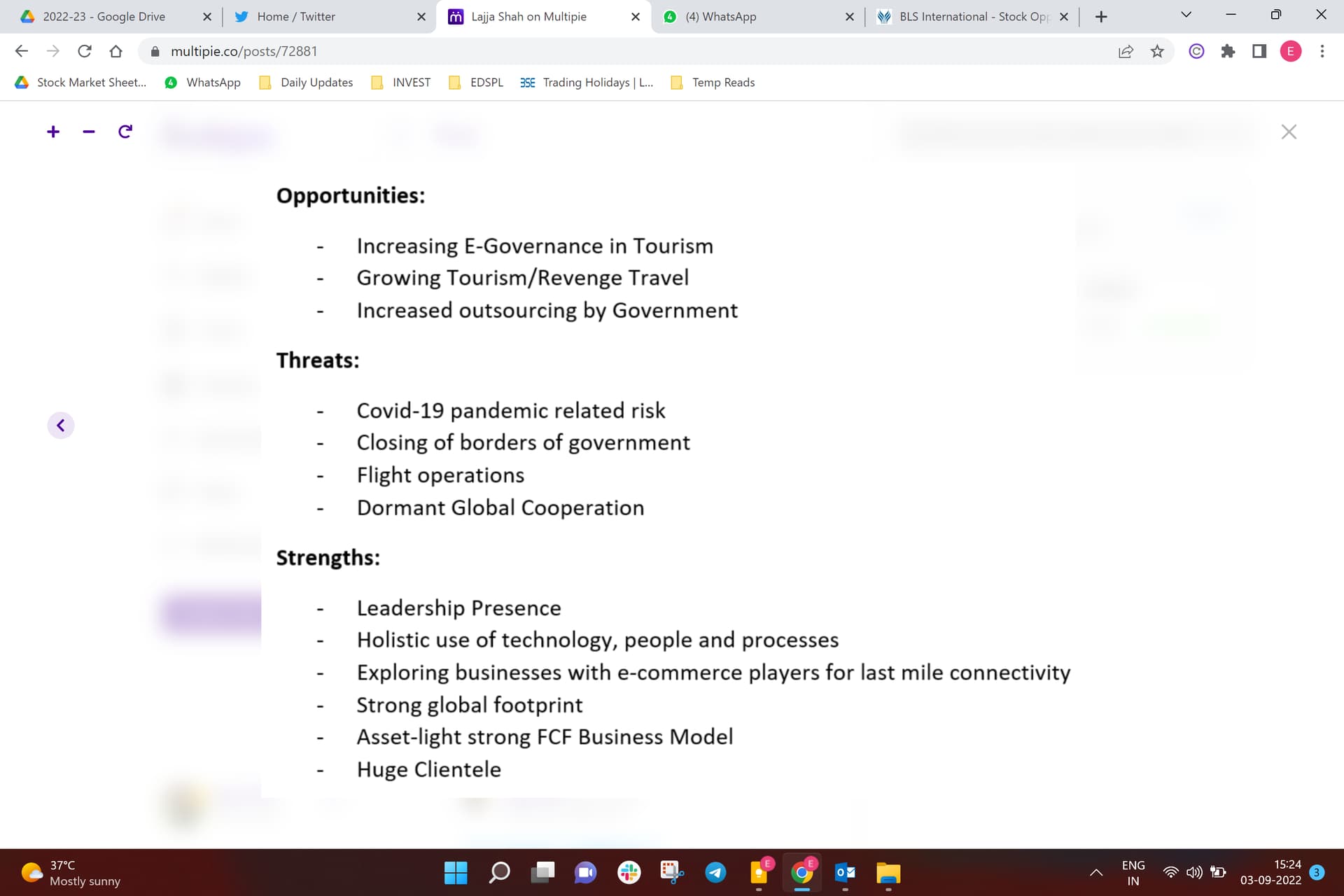

Anti-Thesis pointers

1. There is a huge amount of cash in balance sheet and management is not clear about its effective utilization. (They talked in concall about potential acquisitions)

2. It is still a small fish in a pond where the shark is VFS. But it is slightly making inroads. Will have to look for a couple more years to see where it stands.

3. Any malice or mismanagement at the behest of management is a clear ‘get out’ signal to me as this whole business operates on reputation and trust. Any Black swan risk to reputation will yield a bad body blow to it.

4. E-Visa is a potential risk but in my view, it is hard for most countries to apply that as many developed countries want to check and verify who crosses their borders.

Disclosure: Invested

6 Likes

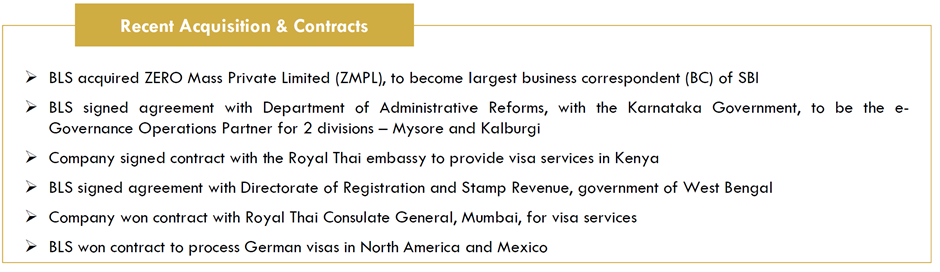

BLS International signs contract to process German visas in North America & Mexico

Share

New Delhi : BLS International on Tuesday announced that it has signed a 7-year contract to process short-term and long-term visas for Germany in North America and Mexico regions. BLS will be starting operations with two centres in Mexico and eight centres in North America in cities including Boston, Chicago, Houston, Los Angeles, Miami, New York, San Francisco and Washington D.C within six months.

The company will be providing visa outsourcing services along with several value-added services like photocopy, translation, courier, insurance for the convenience of applicants.

“We are delighted to initiate this new partnership with the Federal Foreign Office, Germany and committed to provide faster and convenient German visa services to the applicants in North America and Mexico regions. This contract strengthens our visa portfolio with yet another addition of Schengen government. I am confident of a seamless rollout and hope to strengthen this relationship with more such opportunities” Mr. Shikhar Aggarwal, Joint Managing Director, BLS International said.

These centres will provide additional facilities including Premium Lounge (wherein applicant can opt for personalized service) and Prime Time Submission (wherein applicant can submit their application before & after working hours of the centre). The company will also be launching the Mobile Biometric service wherein applicants can choose to submit applications at their convenient place (home or office) at an additional fee

5 Likes

June 2,2022: BLS International signs contract with Royal Thai Consulate-General, Mumbai for visa services.

June 8, 2022: BLS International acquires Zero Mass Private Limited (ZMPL) to become the largest Business Correspondent of State Bank of India.

2 Likes

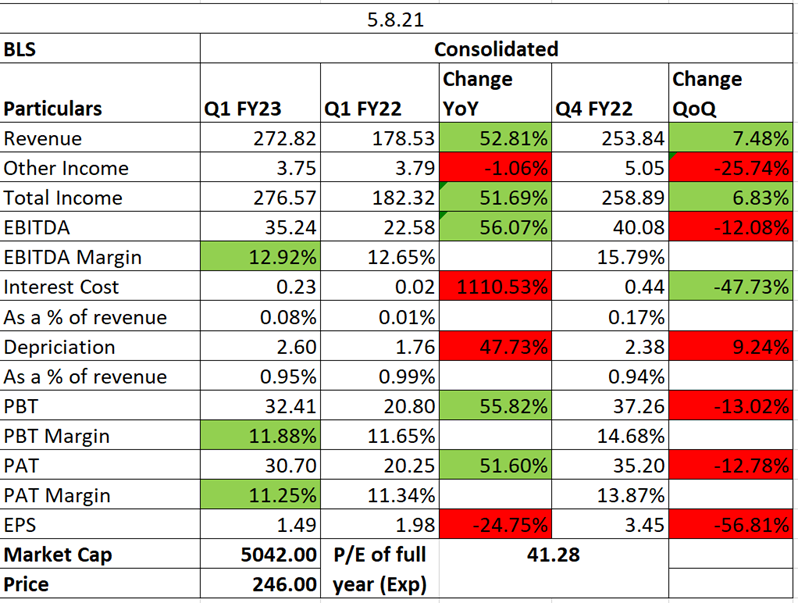

BLS International Q1 FY23 Results! Should be a good long term opportunity…FIIs have also increased stake from 1.36% in Q4 FY22 to 4.32% in Q1 FY23.

4 Likes

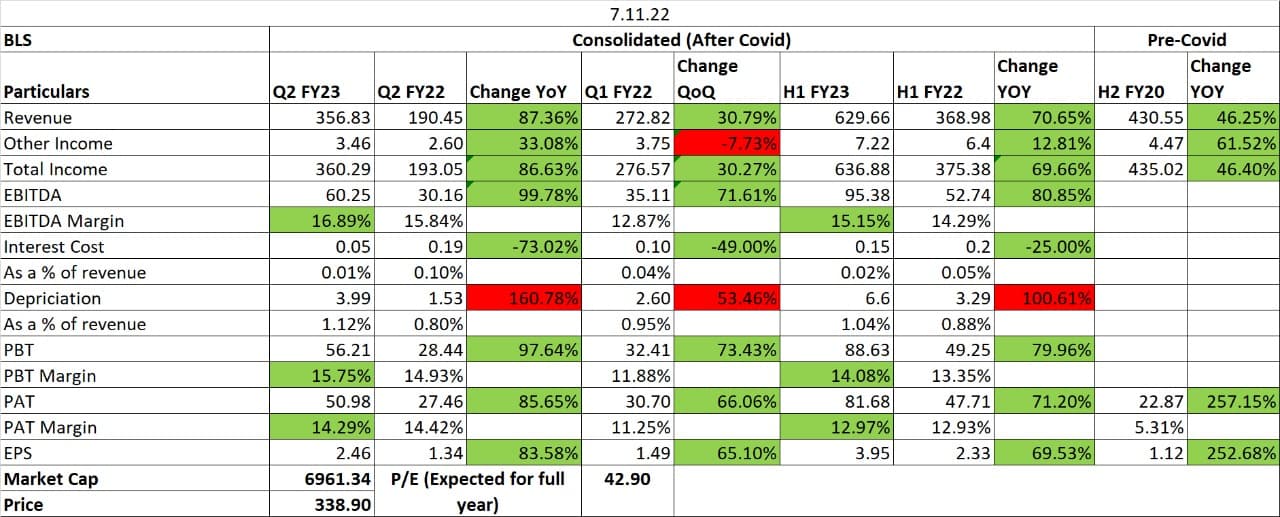

Q2 FY23 Results!!!

Should be a good long term opportunity…

FIIs have also increased stake from 4.32% in Q1 FY23 to 6.67% in Q2 FY23!!

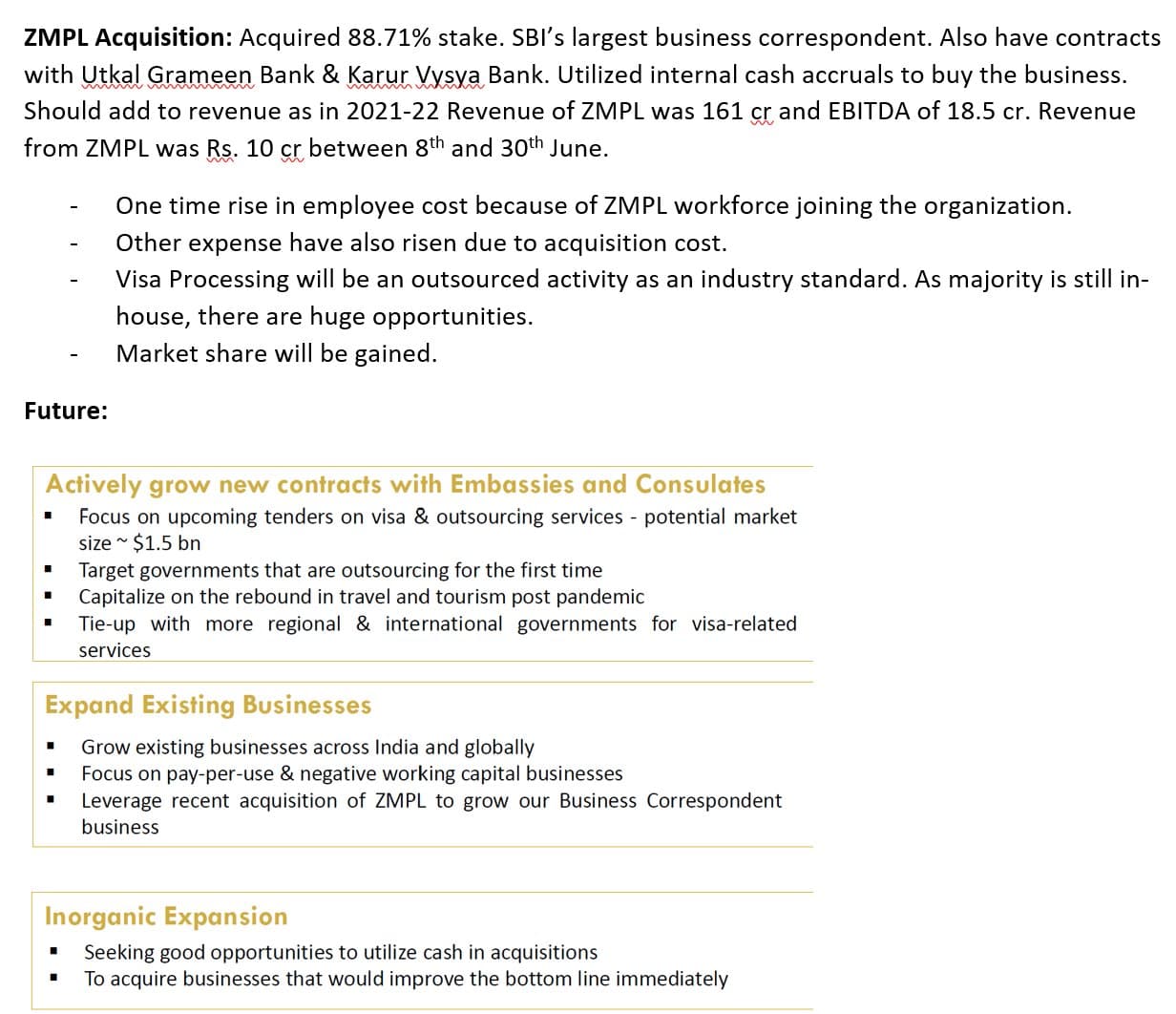

| - | Consolidating business of E-Governance & Citizen Services into Digital services. |

|---|---|

| - | ZMPL acquisition for business correspondent line is growing to require dedicated strategic focus. |

| - | Company will invest in developing infrastructure & manpower for E-Governance & Business Correspondent business. |

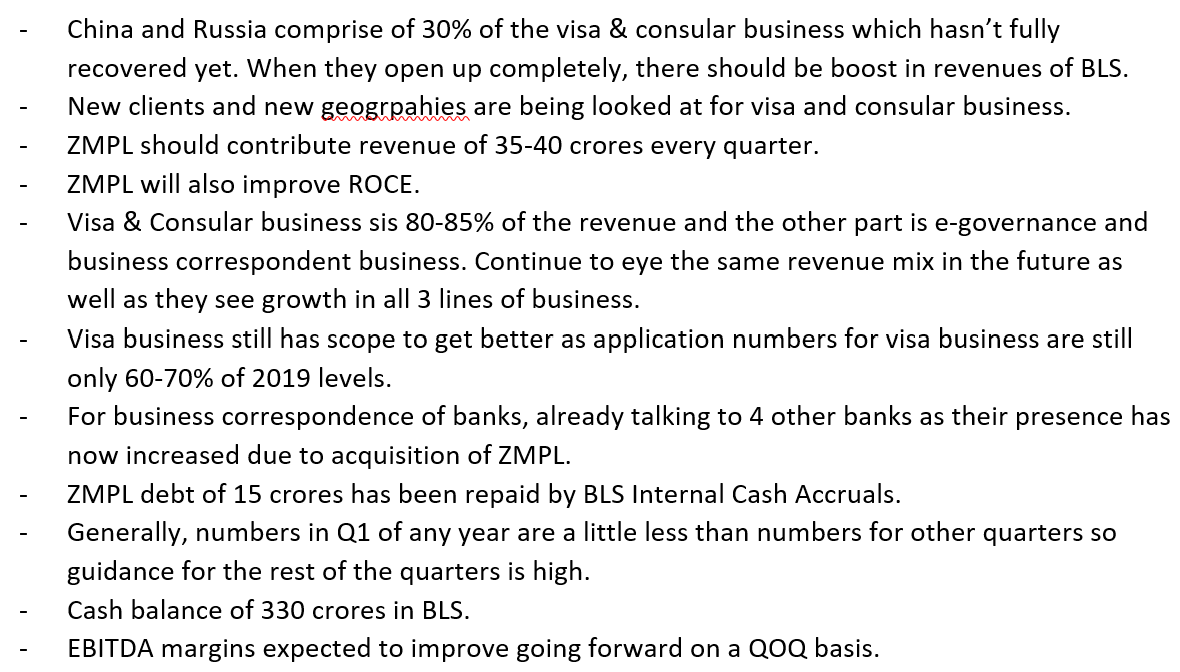

| - | Visa & Consular business saw a strong recovery in business. Certain countries have exceeded their pre-covid levels of business. Some countries are yet to open up fully. China and Russia comprise of 30% of the visa & consular business which hasn’t fully recovered yet. When they open up completely, there should be boost in revenues of BLS. |

| - | ZMPL has started contributing to revenue. In this quarter, 40 crores was the contribution. PAT contribution is 5.5 crores. Management gave guidance that ZMPL will contribute Rs 35-40 crores of revenue which was seen in Q2FY23. |

| - | EBITDA margins improved due to economies of scale and cost optimizations. |

| - | Visa & Consular services contributed 82% of revenue and Digital services contribute 18% to revenue. |

| - | Visa & Consular services contributed 85% of PBT and Digital services contribute 15% to PAT. |

| - | Future Road: Inorganic Expansion, Strong Focus on Digital Services (BC/E-Governance), Embassies and Consulates contracts acquisition as it is gaining recovery. |

| - | Current margins for digital service business are 12.5-15% but will increase going forward. |

| - | SBI is the biggest correspondent in ZMPL. Also, working with PNB, BOB, Central Bank of India & Karur Vysya Bank. Planning to increasing working with banks. |

| - | Reach ROCE target of about 30%. |

4 Likes

BLS Q2 FY23 Result Update:

- Annualized ROE at 28.4%. They wanted to reach the target of 30%. Margin improvements are there due to better asset utilizations and tighter control of operations. Cash generation has been the focus. Have increased touch points for digital services from 80000 to 90000 pan india.

- Has seen high recovery in visa & consular business.

- Zero Mass pvt. Ltd. contributed 42 crore to the top line.

- Invest in technology to further build robust systems and processes, also looking for inorganic opportunities, tapping new geographies and countries.

- Opening up of China will increase volumes. Russia is still an opportunity. 30-35% of the applications come from Russia and China.

- Margins will start to expand from Q4 onwards. This quarter it was subdued was due to investments made in digital businesses.

- Income Tax Rate for FY23 & FY24 should be around 12-15%.

- Same revenue mix is expected for visa-digital services (80-20).

- On a top line basis, they see more opportunities in digital services but margins are much higher of visa business.

- Guidance: Still not operating as per 2019 levels. There is still opportunity for growth in FY24. Only operating at 70-75% of pre-covid application rate. 15-20% growth in revenue expected in FY24.

4 Likes

BLS INTERNATIONAL BLS E-Services a Subsidiary of the Company has acquired additional equity shares of Zero Mass Private Limited ( ZMPL) from the existing shareholder of ZMPL

Post this acquisition, BLS E-Services is holding aggregate of 90.942 % of the paid-up equity share capital of ZMPL

1 Like

[A Stock that gave me 150% Return!!!]

In my last post, I had mentioned about “My First Mistake”, where in I had missed out on a few points of my Checklists which had led me to making a loss.

In this post, I will tell you how these Checklists helped me find the “The Right Stock!”

The stock that I am going to be talking about it BLS International Services Limited.

Since Covid happened, I have been focusing on companies which are related to the travel sector and providing any kinds of services that involve the travel theme. This is when I came across BLS International. BLS is into the business of providing Visa Processing Services (including E-visas), Digital Services like E-Governance & Citizen Services, Consular Services &Value Added Services. They are among the top 3 players in this domain. The company is a preferred partner for Embassies and Governments across the world, having an impeccable reputation for setting benchmarks in the domain of visa, passport, consular, e-governance, attestation, biometric, e-visa and retail services. It also provides citizen services to state and provincial governments across Asia, Africa, Europe, South America, North America & Middle East.

It is a recently listed company (2016) and in 2020, an all-time low of Rs. 8 was made by the stock. Until 2020, the company was doing very well fundamentally that is growing revenue, growing profit, growing EPS, good return ratios, margins also at pretty good levels and positive cash flow generating company. The debt levels increased a little in 2017-18 but then were reduced back until 2020.

That’s when I decided to keep it in my watch list. In 2020-21, the company’s revenues halved and gave the same effect to the profitability of the company. Slowly and steadily the revenues started to get better quarterly and that’s when I decided to enter the stock. I also saw that FII’s were increasing their holding every quarter which was a very huge positive for the company. DII’s also taking up exposure since Sept, 2022.

In CY2022 only, the company gave bonus twice (May & Dec, 2022). I am still holding the stock and already got return of 150% and hoping for a better story in the future. They still have a lot of opportunities to cater to:

-

Only 35% of the total visa market is currently outsourced and only BLS has only 12% market share, which leaves a lot of opportunity. -

Value added services could be a significant margin booster. EBITDA margins are around 15%. VAS accounts for 35-40% of the total contract value which the management expects to take up to 50-60%. Increase in prices of Value Added Services. Customers have started opting for more VAS. -

For strong presence in Banking Correspondent Business, made acquisitions of Starfin and ZMPL. (Largest Banking Correspondent of SBI). -

Still at 70% application levels of 2019. Russia and China opening up now. -

Recent Contract with Poland Govt. Expecting to process 20000 applications annually. -

Revenue per application has also gone up by 35-40%. Has a mix up of pricing increase and customer demand increase. -

BLS Insider Acquisition: Promoter Group/Immediate Relatives have started buying shares from open market. Total Value of Buying is 71.92 lacs. (45880 shares) as of 6th April, 2023.

This is not a recommendation to buy whatsoever.

The stock is currently at Rs. 180 and still I see a better future for the stock.

Happy Investing!!!

2 Likes

I try to experience as a customer of the business I am investing in to go through the process and understand MOAT of the business.

I have had quite bad experiences with BLS, including staff trying to overcharge etc.

The MOAT is that customers may not have any other option but to go through BLS. BLS may not result in happy customers but all the overcharging should result in happy shareholder. ![]()

4 Likes

| - | ROE stands at 25.4%. Company wants to improve asset utilization & cost optimization which leads to margin improvements. Economies of scale and Cost optimizations helped offset higher cost of services and employee costs, leading to better EBITDA margins. Margins are expected to get better. |

|---|---|

| - | Debt free company with cash of 225 crores which is the highest ever cash generation. They still want to improve cash generation metric. |

| - | Strong recovery in visa and consular business and digital services business. Visa & Consular business saw a 67% YOY growth in revenue in FY23 & EBITDA YOY growth of 70%. Digital services saw a 174% YOY growth in revenue in FY23 & EBITDA YOY growth of 6960%. |

| - | Quarterly Developments: Increased stake in Zero Mass Private Limited. Won several new contracts during the period. Signed agreement with Polish Embassy in Manila to provide visa outsourcing services. Signed MoU to accept electronic visa on arrival for seamless travel to Thailand. |

| - | Digital Services Business Future: Investing in infrastructure and manpower to expand digital services segment. Plans to restructure business to make digital service segment a self-funded, growth-oriented, and independent business. |

| - | Guidance: Expects growth of around 20% to 25% in existing business. Potential for an additional 10% to 15% growth from opening of new geographies like China and Russia. Expects growth to continue from existing contracts. Negative working capital cycle and targeting growth rates higher than 20-25% in both visa and consular services and digital services segments. Market share in Visa Consular business estimated to be in the range of 12% to 15%. |

| - | Strategy: BLS International Services looks for countries where there is volume and governments are currently facing processing problems, as well as where future growth markets will come from. |

3 Likes

I am just looking at potential risks. How long is their contracts’ duration? Also do they have cost escalation built in their contracts?

Contracts duration is usually long. More than 5-10 years. Yes cost escalation is there. In one of the management interviews, they said that their realizations per application have exceeded pre-covid levels.

1 Like

BLS Management Meeting (By Edelweiss)/Interview (by CNBC TV-18)

- To drive growth, the company is also expanding its G2C (Government to Citizen services) and banking correspondence (BC) businesses, which are similar to asset light Visa processing and Consular (VC) businesses.

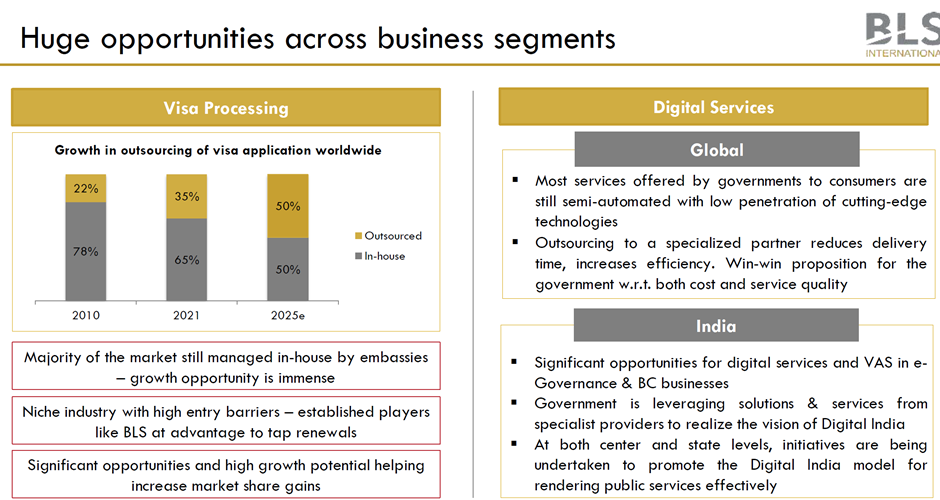

- Only 35% of the total visa market is currently outsourced and only BLS has only 12% market share, which leaves a lot of opportunity.

- Value added services could be a significant margin booster. EBITDA margins are around 15%. VAS accounts for 35-40% of the total contract value which the management expects to take up to 50-60%. Increase in prices of Value Added Services. Customers have started opting for more VAS.

- Significant contracts will be up for renewal in the next 2 years.

- For strong presence in Banking Correspondent Business, made acquisitions of Starfin and ZMPL. (Largest BC of SBI)

- BLS currently operates a high free-cash-generating model in which service fees are collected upfront (in its Visa processing as well as Digital Services). Furthermore, it uses a lease model for the majority of the centres from which it operates, resulting in lower capex requirements. BLS has no debt and has consistently generated positive cash flow from operations over the last five years. It reported a cash balance of INR 340 crore on September 22. Better operating results and improved working capital led to a cumulative FCF of INR 468cr from FY17 to FY22 (i.e. 7% of current market cap). We expect faster EPS growth, driven by a greater contribution from the Digital services segment, business normalisation following CoVID, and Visa & Consular Services segment.

- Still at 70% application levels of 2019. Russia and China opening up now.

- Recent Contract with Poland Govt. Expecting to process 20000 applications annually.

- Revenue per application has also gone up by 35-40%. Has a mix up of pricing increase and customer demand increase.

3 Likes

BLSInternational_10July2023.pdf (1.7 MB)

bls international key takeaways from above report by jefferies—

— among top ~3 globally in visa processing/consular serv. opng in 66 countries

— building niche in govt to citizen digital services & banking correspondence biz in India

— mgmt is of the view that will benefit from opening up of int’l travel, increased visa outsourcing globally, digital India led new IT outsourcing initiatives by Indian state govts, & higher VAS biz

— rise in visa applications bode well for travel & tourism plays

— FY23, company clocked Rs15bn in revenue including ~Rs12bn (80-85%) from global visa and consular service business & ~20% from digital services (largely India focused) incl e-governance services, Banking/business correspondent services

— Globally, 80-85% of visa outsourcing business is controlled by 3 players, with dominant share held by VFS Global (at 50-55%, unlisted Co owned by Blackstone) and*~10-15% share held each by BLS* and TLS (listed in France)

— Mgmt believes that only 50% of visa processing business is outsourced (vs 22% in 2010) by embassies globally, providing runway for Industry growth

— BLS entered Int’l business in 2016, when it won global contract for visa outsourcing by Govt of Spain. Post that, Company has won contracts for different geographies for different govt like in Europe, GCC & ME, South America

— Visa processing business operates on *negative working capital

— Typically, visa contracts are exclusive contracts for 5-7 years. BLS has its tech software for appointment booking and processing applications.

— bls also offers higher margin value-added service(VAS) like SMS, courier services, mobile biometrics, premium lounge, travel insurance

— Mgmt believes that barriers to entry are high for the business with stringent criteria by embassies to participate/win the tender: ; 70% weight is on technical qualifications while only 30% weightage is on pricing

— Mgmt highlighted growth from (1) participation (and wins) from global visa outsourcing contracts worth USD1.5bn, which are under renewal in next 2 years

— (2) capitalize on opening up of travel in economies which are still lagging vs pre covid level; (3) focus on margin expansion on the back of increased VAS and economies of scale as company add new contracts; (4) M&A to strengthen the digital services businesses

— Company focuses on asset light model (visa application centers are leased) with

aspiration of 20% EBITDA margin (FY22/FY23: 13%/15%)

— Margin benefits as revenue per application increases (via higher VAS), and on back of economies of scale

— BLS is debt-free & mgmt said focus on improving cash generation as a key business performance metric

— Mgmt said, BC business has been expanding rapidly spcly after acquisition of Zero Mass Pvt Ltd; increase in touchpoints (incl via inorganic initiatives) would aid topline /margins

— Company targets services offered by govt to consumers (G2C) which are still semi-automated with low tech penetration; currently working with Punjab, UP, Kar, Raj, WB.

— Over past few years, select govts have started outsourcing some citizen services (eHospital, BHIM-UPI, online scholarships, DigiLocker, Umang app, marriage & birth certificates, etc.) to specialized players under digital India initiatives. These G2C services, coupled with Banking correspondence (last mile banking), together form Digital Services

4 Likes

- Annualized ROE stands at 37.3%. Company constantly strives to improve this by better utilization of assets and cost optimization, resulting in improvement of margins.

- The Group continues to remain debt free and have Cash of Rs 642 crores. BLS International plans to utilize its cash for acquisitions, opening offices in new geographies, and expanding existing businesses.

- Company announced IPO for subsidiary BLS E Services to raise funds to support growth strategies for Digital Services (e-Governance and Banking Correspondence) business.

- Cost optimizations and Value Added Services helped offset rise in employee costs, leading to better EBITDA margins.

- Looking for inorganic expansion opportunities in both verticals that is visa and digital services.

- The Ministry of Foreign Affairs, Spain has awarded BLS International the global contract for visa application outsourcing for the second time in a row. The contract covers Europe, the Americas, Latin America, the CIS, Africa, the Middle East, and APAC, amongst other regions. Company also won new contracts with the Italian government, Poland government and other governments.

- The growth is returning to pre covid levels. Company’s prices for both service charges and other services have increased, so company expects to maintain their current growth momentum going forward.

3 Likes

BLS signed a 5 years global visa outsourcing contract with Slovakia.

Disc. Invested

2 Likes