Is someone still tracking BHEL. They did loose on the arbritation case against Suvarna Power as the liquidation process had already started. I couldn’t find an update on this whether the liquidation process got resolved

I am unable to understand broker calls here. BHEL’s receivables position appears to have improved a lot, they have had a pretty good quarter operationally and the reported loss is mainly due to the large provisions they have done on some outstanding receivables as per their clarification. Shouldn’t it do better going forward? Why are the broker price targets so low?

Calling for experts on #Bhel , According to Elliotwaves this is ready for upmove again.

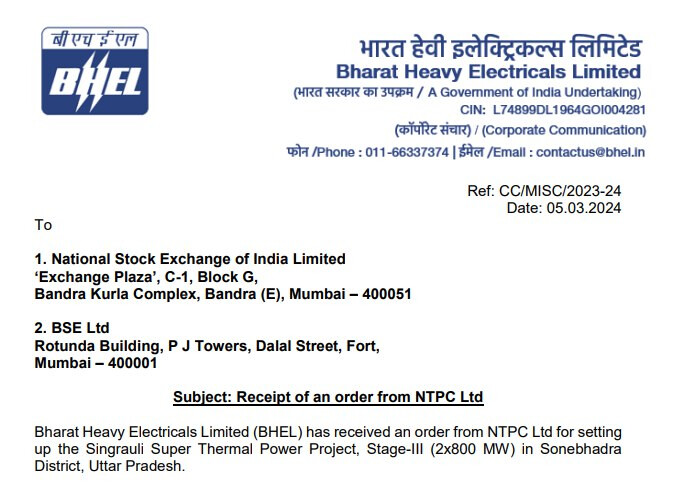

BHEL secures order for 2x660 MW Talcher Thermal Power Project Stage-III.

BHEL has received a prestigious order for setting up the 2x660 MW Talcher Thermal Power Project Stage-III on EPC (Engineering, Procurement & Construction) basis from NTPC Ltd. NTPC is investing Rs 11,843.75 crore for this 1,320 MW Talcher Thermal Power Project, Stage-III.

BHEL Management Interview: (CNBC TV-18)

- Margin reduction was due to execution of older orders which were at low costs. As and when new orders are executed this problem will start resolving. Order intake for Q2 FY23 is 12000 crores.

- Total order book of Rs. 106376 crores.

- Gross Margins are expected to rise but not on the older levels of around 40%. They will increase but not to the older levels. Will take 2-3 years for margins to substantially increase.

- Coal Gasification is a very major area for the company as well as the country. Plans are in place to implement the same and construction will start soon.

- Targeting revenues of around Rs. 40000 crores by FY27 with double digit margins.

- Have always remained cash positive as receivables are in a good position.

https://twitter.com/cnbctv18news/status/1602162676633067520?s=48&t=K-2-3DJAd9HNRWVnnZ32GA

https://twitter.com/cnbctv18news/status/1602162973945917440?s=48&t=K-2-3DJAd9HNRWVnnZ32GA

with respect to recent activities, results and concalls, do experts in the group see a potential in BHEL over the next 5-10 years?

Recent call transcripts https://www.bhel.com/sites/default/files/BHEL-Q4FY23%20concall%20transcript-26May2023.pdf talk about good prospects and also productivity improvement etc?

Any potential risks/constraints due to Govt ownership ?

In the concall there is a mention of Contract assets of INR 29740 Crores. Can someone explain what is contract assets and what’s the significance?

Any expert views helpful.

Thanks

Disc - Small holding for tracking

BHEL - Investment case

- Company Overview - BHEL

- BHEL - PSU is India’s dominant producer of power & industrial machinery since 1964

- 200 GW+ installed capacity (70% power generation in India from BHEL Installed capacity in India)

- Key beneficiary - Aim to achieve 50% market share from non power segment (30% presently)

- Attractively placed for capacity addition of high growth sectors – Decarbonization, Green Hydrogen, Transportation, Aerospace & Defense with impetus on “Make in India” & “Atmanirbhar Bharat”

- Market Cap – INR 88k Crs, Revenue INR 24K Crs, P/B – 3.4x

- Order book - 1.2 lac Crs

- 503 patents filed in FY23 - Total IP - 5,443

- Selling shovels during a gold rush

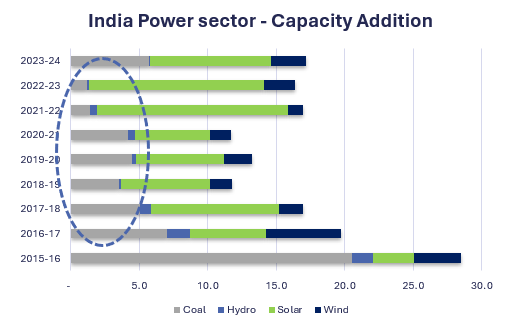

- Minimal Thermal capex investment for during 2017-24 period (<5 GW pa)

- Leading to deficit in 2024-27 period

- Focus on capacity addition – Thermal, Solar, Wind

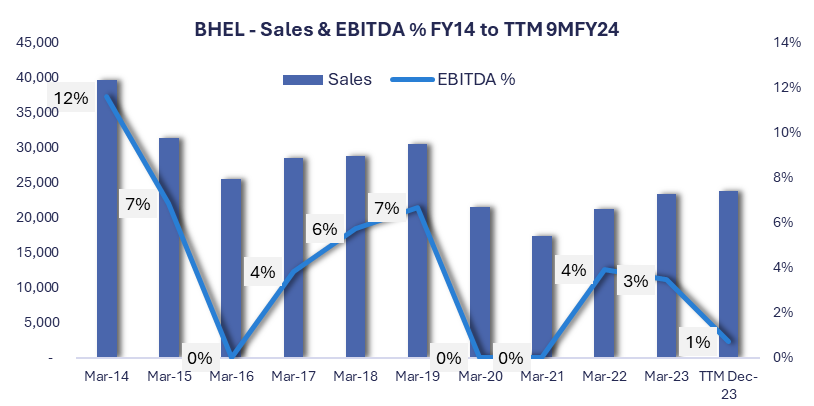

- At the bottom cycle from financials, upward cycle has begun

- Investment case

Good

- Uptick in thermal capacity addition due to strong electricity demand, uptick in spot market prices and no major capacity addition in next 3 years

- No major presence of Chinese / International BTG supplier – major beneficiary last time

- Strong order inflow from Central, State & Private sector utilities

- Improvement in order terms – commodity cost pass-through – learning from last upcycle

- Reduction in manpower – 50k to 30k

- 30% order book in non power sector & management focus on developing non power sector order book – Target 50%

- Decrease in competitive intensity will lead to better margins

Better

- Decarbonization opportunities – FGD, Green Hydrogen, Renewable generation

- Defense & Aerospace opportunities – Cryogenic component, Batteries and other components for Chandrayan -3, indigenization of imported parts

- Transport opportunities – Railways & Urban Transportation - 80 Vande Bharat trains Kavach etc.

Best

- Efficient capital management from shareholder perspective

- Improvement in efficiency at part with best global OEMs

- Improvement in execution capabilities

- Recovery and resolution of sticky receivables through mutual agreement, arbitration & other mechanisms

- Ability to make significant break-through in decarbonization and green hydrogen sectors

- Technical analysis

Price uptrend continuation with all time high volumes

- Risk

- Being an PSU, majority shareholder may influence business decision, capital allocation strategy

- Historically faced with sub par execution skills and delay in delivery, may not scale up due to such issues

- Profitability may be impacted, or receivables may not come through due to any reasons, as seen in last cycle

Disclaimer: Education purpose only, Not an Investment advice or recommendation.

3 Likes

What is the rationale in investing in BHEL. They have had a huge order book since many years and margins are completely deteriorated.

Their revenue, profit is stagnant and has declined over 5 years.

The valuation is also so high.

1 Like