Could not get a thread on Bharti Infratel, hence started it.

I. About Bharti Infratel (as mentioned in their website)

A leading provider of tower and related infrastructure. One of the largest tower infrastructure providers in India with more than 39000+ Towers, based on the number of towers that Bharti Infratel owns and operates and the number of towers owned or operated by Indus, that are represented by Bharti Infratel’s 42% equity interest in Indus.

They are also pioneers in the concept of environment friendly Towers or ‘GreenTowers’ and energy efficient methods for maintenance of these towers.

II. Services : Establishing, operating and maintaining mobile towers.

a) Tower Infra Solutions

b) Tower Operations Center : Managing Day to day operations of Towers.

c) Infratel Enterprise Suite : Online ERP platform, where the user can raise and manage their respective business requests on an end-to-end basis. The entire process of requesting a new cell site or a cabinet expansion can now be administered through this smooth, transparent and efficient mechanism.

III. Key Differentiators

Undisputed benefits of scale and experience – leading to cost and operational efficiencies

Proven O&M, and uptime capabilities for large scale operations

State-of-the-art fully automated Tower Operations Center – to monitor alarms and SLA delivery - leading to superior customer satisfaction

Business Performance centric processes, technologies and IT systems – including Customer Portal and CIT

Commitment to Green energy and energy efficient technologies – we have the largest Tower Infrastructure installation of solar powered Towers in the world

Went through the complete annual report, some interesting insights which I would like to highlight.

Profile of Board members looks extensive & quite top notch. (Page 24)

Through out they have shown images of employees working, what is more interesting is the CSR details. Where they have shown images of ppl benefiting (Page 60 onwards) & testimonials from ppl (page 65 & 68).

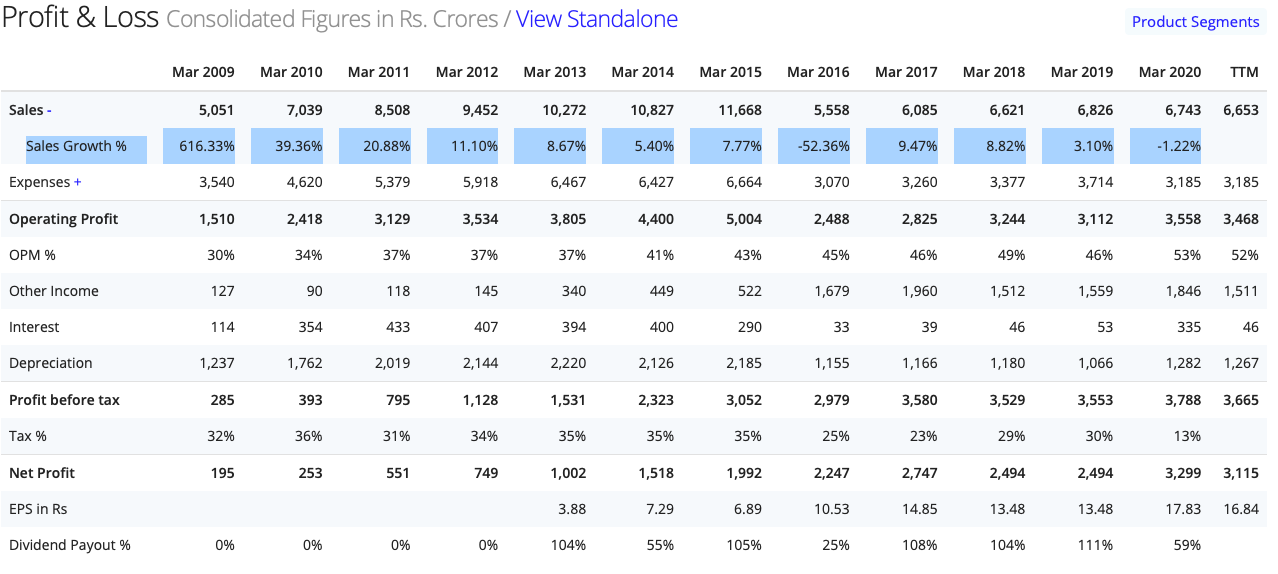

Though the sales has taken a dip of around 1.2%, their travelling expense has taken a much more dip. Which is in fact good. From Rs 160 million (FY 18-19) to Rs 140 million (FY 19-20). (Page 207)

Being in to corporate travel, I always take it as +ve. (Any growing company should have a growing travel spend & vice versa).

Few red flags :

I fail to understand why their Debt has increased, as visible on Screener as well. Highlighted in Blue.

As per the merger agreement, Vodafone-Idea and Providence have the option to receive shares or cash for 11.15% and 3.35% stakes in Indus respectively.

It was mentioned in their con-call that this debt was raised for cash payment to Vodafone-Idea and Providence.

Bharti Infratel is deliberately delaying this merger due to SC AGR ruling. They are waiting for final ruling from SC and if it is favorable to Voda-Idea and Voda-Idea survives, then they may go ahead with merger process.

Also, one of the main benefit mentioned for merger was double taxation of dividend paid by Indus Towers till FY20 (Tax on Indus dividend payment to Bharti Infra and similar tax on Bharti Infra dividend payment to its shareholders). But with new dividend taxation rule, its taxed only in the hand of Bharti Infra shareholders.

I don’t think anyone have doubt on Airtel survival. But for Bharti Infra shareholders, real question is what’ll happen to Voda-Idea. If Voda-Idea gets favorable ruling from SC and they are able to bring equity by themselves or selling their stake to someone else, then Bharti Infra could turn out out to be a great compounding story.

If you’ll see the listed Tower companies around the world, they are among the best compounders of last 2 decades with good dividend yields.

Disc: Invested (before SC AGR ruling) and still holding

Here’s my thoughts on Infratel. I have never analysed the telecom space prior to this so i could be (very likely am) completely off the mark. Would appreciate thoughts from people who know this sector well to throw some light on the correct way to think about this.

Infratel did EBITDA margins of 50% in FY20 and sell side expects ~ 53% margins over the next 3 years. Based on these expectations, net lev by FY23 end is expected to be just 0.1x , so essentially net debt free. Div yield is expected to be near 8.5% based on CMP. When REITs are yielding 6.5%, this is not bad at all given that tower cos are largely utility kind of businesses vs. commercial real estate which (all else equal) i feel have more uncertainty as regards their cash flow sustainability. On valuations, Infratel is trading near ~5.4x EV/EBITDA vs. long term avg of 8.5x, so a significant discount given the uncertainty on VIL and hence Indus Towers. The big assumption baked into the current sell side estimates is that VIL survives. If that happens, that makes Infratel a much much easier story to bet into. But my thinking is that if VIL does go under, their entire subscriber base has to shift to Jio and Airtel. Now, can Airtel and Jio’s existing tower infrastructure handle THIS level of large influx from incoming customers? Likely not poss. While they would certainly sweat their existing tower infra more, they would definitely need more tower infrastructure to accommodate the incoming customers. So while they could build out their own tower infra over time, in such a case of “buy vs. build”, it might make more sense to go for ‘buy’ as customer migration will be very swift. In such a case, the tower rentals that Infratel gets from VIL currently might quickly get replaced by Jio/Airtel via either these cos buying out the VIL related towers or or some such transaction. While Infratel could still end up with spare capacity / lower utilization and lesser bargaining power (2 customers vs. 3 currently), it doesn’t look like it will become a zero revenue thing as far as tower capacity used up by VIL is concerned right now. So the worst case isn’t likely to be an entire loss of revenue from the VIL related towers but rather a haircut on the same. How much is the haircut is debatable but my point here is that it isn’t likely to go to zero. It would create a lot of volatility and headline risk for Infratel in the short term but if we are to take lets say a 5-7-10 yr view, i think this is def worth exploring. If you see Tower cos in the US, they’ve created enormous value, (see tickers AMT, CCI and SBAC) , much more vs the Telecom companies themselves (VZ, T, etc.). Their regulatory environment as well as their interest rate environment is not comparable to ours but basically, if a tower co has a decent regulatory environment and a steady interest rate regime, can be a very good asset class that yields dividends as well as capital appreciation.

Disc : Not invested in Infratel or any of the companies mentioned above except Embassy REIT.

Tower companies take land or building areas on lease for longer duration and build a tower there. These towers could be for single tenant or multi tenant. These are the major fixed cost for tower companies.

Now if the tower is single tenant one, then it cannot host more than one tenant. And here RoCE might be like utility companies. So if the telecom companies have enough money (which they haven’t as of now) and can manage their towers efficiently, they might keep them as captive towers rather than giving good returns to tower companies. (Before Jio onslaught, both Vodafone n idea had captive towers which they later sold to others. And Jio also built its own towers and is in process of selling them to Brookfield to reduce its debt. Most Jio captive towers or maybe all of them are single tenant towers.)

In case of multi tenant towers, things become interesting. The cost for setting up multi tenant tower is more because of bigger tower and more leased area. But if you have single tenant, it won’t be willing to give you more rental than rental for single tenant tower. So with single tenant, tower companies might not even make cost of capital. But if it gets second n third tenant, then operating leverage kicks in. With more tenants, tower companies reduce rentals for all tenants and still makes good RoCE. This is mutually beneficial for all participants. Telecom companies can’t build towers cheaper than rental for multi tenant towers and also they don’t have to make large capital investments in infrastructure.

Most of the Bharti infratel n Indus towers are multi tenant towers. In case Vodafone Idea shuts down, their returns will drop drastically as they have to bear the cost of more leased area and bigger towers. And being operational creditor, I don’t think they’ll get any relief in IBC.

Out of this borrowing of 4627 Cr, 2208 Cr was lease liability and 2385 Cr was short term loan. Also, they had 5438 Cr in mutual funds and government bonds and 112 Cr as cash and bank balances. (Mar 2020)

And, they have further reduced the short-term loan to approx. 1100 Cr, as on Jun-2020.

Yes Indeed.

Wats more interesting is that the merger would save more than 550 Cr annually for the company & a turnover of Rs 25000 Cr. Which is like 2.2 % of Turnover.

However this cost saving may take OPM to inch towards 55% from current 51-52% (as per screener).

Just a thought, isn’t it better to invest in Infratel than the Airtel.

The shares issued to Vodafone would be equivalent to 28.2% in the Combined Company. Bharti Airtel’s shareholding in Bharti Infratel would be diluted from 53.5% to 36.7%. Bharti Airtel and Vodafone will jointly control the Combined Company.

Vodafone Idea would receive approximately INR 40 billion in cash upon completion and a prepayment in cash of INR 24 billion to be made at completion of the transaction by Vodafone Idea (the “Prepayment”) to the Combined Company in respect of present and future obligations under the MSA. ( The prepayment amount will be adjusted to the extent of 50% of all undisputed and due amounts payable by VIL to the merged tower entity post-closing and VIL will be required to pay only the balance 50% of undisputed dues. The prepayment amount will accrue interest at 6% p.a. This will continue until the entire prepayment amount with accrued interest is fully adjusted.)

A primary and secondary pledge over shares owned by Vodafone in the Combined Company with a value of INR 82.5 billion.

This implementation is subject to consent from Vodafone’s existing lenders (Vodafone pledged Indus shares to take €1.3 billion loan to fund its contribution to the Vodafone Idea rights issue in 2019), regulatory approvals and on an extraordinary dividend of INR 48 billion (€552 million) being declared by the Combined Company within three months after completion. This extraordinary dividend value maybe around INR 17.5/share. (Lender consent is expected within 21 days)

Infratel is very much dependent on Voda-Idea survival. So, if we want to bet on Infratel, we have to be sure that Voda-Idea will survive.

In some article, i have read that voda-idea accounts for roughly 1/3rd of merged entity tenancy. So, if possible we may calculate and guess worst case valuation for Infratel and then take the decision to buy or not.

Airtel is in a win-win situation. Tariffs are going to be higher in either case. If voda-idea shuts down, jio n airtel can raise tariffs very quickly. Voda-idea can’t survive on current tariff rates. If it has to survive, tariffs will have to move much higher.

I have been hearing about the story about tenancy drop linked to Idea-Voda survival. In case Idea-Voda doesn’t survive, dont you think what is lost will be made up from the other two large players? (pardon me if i’m completely wrong with my understanding on this one).

You’re making a valid point AJ. What happens to the Subscribers if Vodafone falls, who will give service?

Whoever gives service will pay Tower Dues. Existing Reveiveables will suffer which could lead to a short term shock for Infratel.

My base case assumption is that voda-idea will survive. And, in worst case scenario govt may take over it temporarily to run day-to-day services because of its importance to the nation and the inconvenience it can cause to large no. of citizens.

But in the scenario of its shutting down and govt not taking over, Airtel n Jio will benefit. These companies might not need those many tenancies as vacated by voda-idea. First they’ll increase capacities on their existing towers rather than taking over voda-idea tenancies. Also, Jio will prefer to use its existing towers to enhance capacity and only in case it needs new tenancy, it’ll look to other tower companies.

And voda-idea 2G population, only airtel n bsnl will be able to serve them. I don’t know if they’ll need large no. of new tenancies to serve this market, as the load on their existing 2G infrastructure might already be normal because of 4G migration.

Also if voda-idea shuts down, there will be large tenancy losses for most of the tower companies. It may lead to price war in tower companies. So, whatever new tenancies they may get, it won’t be very profitable.

Tomorrow voda-idea board meeting is there for fund-raising. I am waiting for outcome of this meeting. I feel for such a large and consolidated market, they should easily get the investors.

For those interested in understanding the economics of the business, you should look at American Tower Investor Relations. (NYSE: AMT)

The 2nd/3rd tenant on the properties has super high ROIC.

Once the AGR issue is resolved and there’s less doubt about the survival of Voda-Idea, I don’t see why management shouldn’t lever the business up a few turns of EBITDA. AMT is around 4-5x. This is a rather safe business, perfect for leverage, and allows increased returns to equity holders.

This obsession with a net cash balance sheet is harmful to shareholder returns, especially when the underlying business has such solid economics and return characteristics, given the inherent nature.

And interesting transaction would be to take leverage and buyback Airtel’s stake or a part of it.

Also, not sure how easy is it in corporate governance sense if 2 out of 3 customers are also your biggest shareholders. How will there be independence in pricing and contracts?