What seemed a bit surprising (positively) was management’s ability to predict the Rs. Rs. 350 Cr of Revenue for FY-17 in April-16 interview.

Few other updates:

from their website, it looks like they have ventured into following related verticals:

Agro Chemicals

Specialty Chemicals (Benzophenone, Meta chloro per benzoic Acid, 4 – Hydroxy Benzophenone)

Pharmaceuticals

20 MW of 30 MW solar power capacity has been commissioned as on 31-Mar-2017

Can someone throw light on the additional revenues that the 20MW solar plant can generate? What margins can one expect from it? With dropping solar tariffs, what would be the outlook for bhageria’s solar plant?

@abhishek90 : You mention - "a cartel was formed among these indian chemical companies like bageria and bodal" Can you mention any sources? Has situation changed?

@sammy11: You mention - "These numbers have improved the ROE and ROCE in the last 2 years and I am trying to find out what happened in this period. I think that traded goods had an impact on this. But what happened later? Did they stop trading and concentrated only on manufacturing?" Were you able to find out anything?

Q1 and Q2 results were bad and hence the stock got beaten down.

Q3 performance has been outstanding. The results were released aftermarket hours yesterday. Hopefully stock prices will zoom when the market opens on Monday.

OPM has been fluctuating widely and is likely to continue doing so based on vinyl sulphone prices.

It is nice to see the solar power plant project has generated decent profits in Q3.

Q4 results analysis at a high level. Net sales is highest in recent quarters and PAT has grown by around 50% (Source Market Mojo).

On the downside, Interest outgo has increased, while inventory turnover has touched the lowest. The question here is if the inventory turnover is lowest and net sales is highest (Source market mojo) … does that mean sales figures are inflated ? Could someone please clarify.

If the stock is doing well, then planning to add to my existing position (I have invested a small amount to keep track of the company) near support levels. If the sales figures are cooked up then would exit at a small loss.

Stock price has broken the downward channel and currently is in a gradual up channel. The price touch the top of the channel and is now falling. CMP 296 and it should find support near 280 which is the bottom of the channel. Planning to add at that level.

Inventory Turnover = Cost of good sold / Average inventory

You are saying that sales have gone up but inventory turns have gone down? Inventory turns can go down when either sales go down or when inventory levels are high. If sales number is increasing, that only means they are keeping more and more inventory. Please check if this logic applies.

I have not checked Bhageria’s numbers. Just putting down the logic.

Blockquote Inventory turnover measures how fast a company is selling inventory and is generally compared against industry averages. A low turnover implies weak sales and, therefore, excess inventory. A high ratio implies either strong sales and/or large discounts

Investopedia

If sales were highest then do expect that inventory gets churned faster. When sales are booked but inventory is not transferred then the sales could be an accounting entry to boost the PnL. This is my doubt.

Anyone familiar with the company’s business and relationship between the inventory and sales in this business can throw some light.

Here is a download from screener.in (it has some graphs and data collection template that I use) … plus raw data from screener.

Some important points :

Balance sheet growth is chiefly funded by borrowings (and that explains the increase in interest payment as well).

EPS is inconsistent Mar 14 and Mar 16 were similar, Mar 15 and Mar 17 were very much higher than the previous year. Good news is the TTM EPS is closer to the Mar 17 EPS …

Free Cash Flow has turned positive and Cash/Bank Balance has shot up in Mar 17. The high borrowing and high cash makes an inconsistent story and requires deeper investigation.

Margin compression is noted as higher quarterly sales with lesser operating profits and lesser net profits.

Prices of H-acid and Vinyl sulphone have gone up quite a bit compared to its raw material prices, so I believe June quarter will be great. Chinese court have ordered to shutdown few plants 1-2 weeks back which will create pressure on supply for the next 2-3 months.

Sensing the above development, the company should do good in the short term at least.

Disclosure - Had bought at 100 in 2015 and exited at 380 in 2016, entered again this week with average price of 304 and will keep a stop loss of 265.

Where can one find latest price of H-acid and Vinyl Sulphone ? Can anyone help with the same ?

Recent updates with the company :

Credit rating of the company has been upgraded by CARE

Last week company has announced expansion of Rs 27 crore which is to be funded from self-accrual

In investor presentation for Q1 the company has stated that debt has been reduced from Rs 83 crore to Rs 43 crore.

Company has reported lifetime Highest Turnover and lifetime Highest PAT in this Quarter.

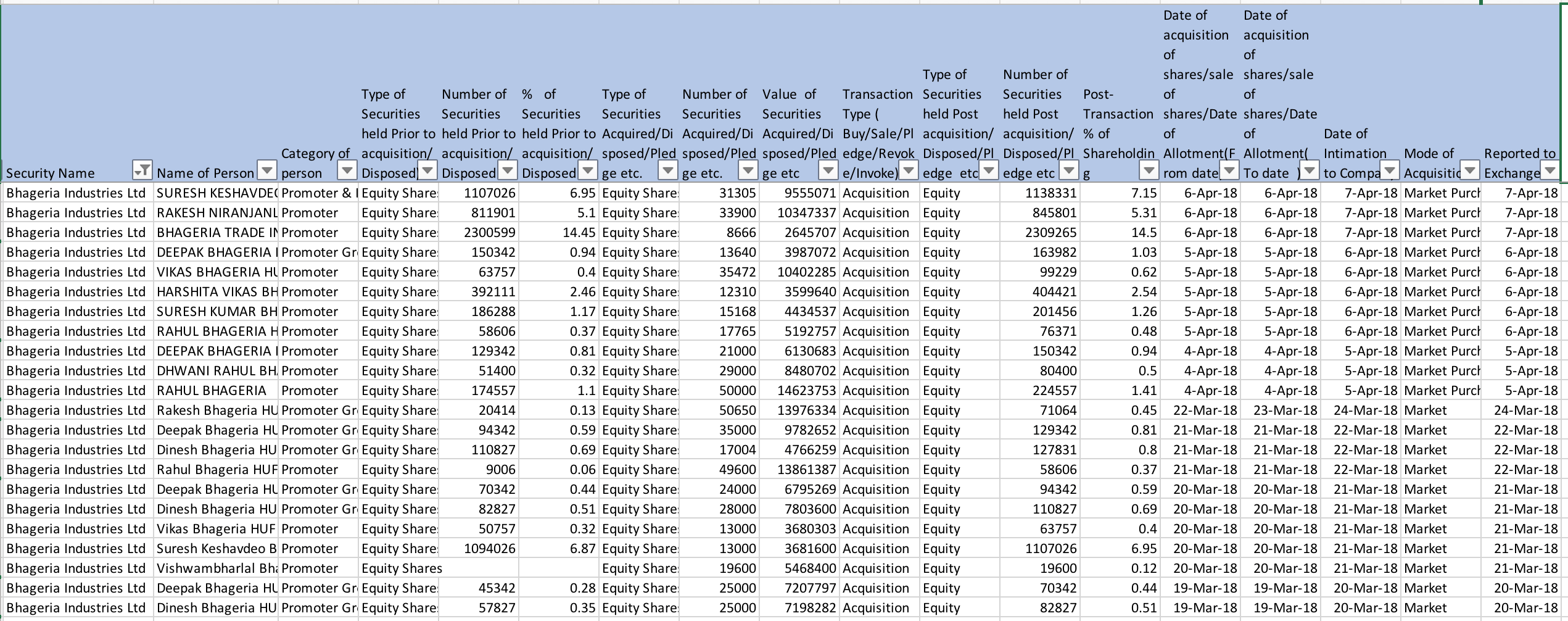

Promoters stake is constantly increasing since past 9 months.

It appears very promising to invest in the company considering various facts on hand. Further it is to be noted that the company has been consolidating since past 2 years after hitting a high of 430 levels in 2016.

Disclosure : Invested in the company at 300 Levels.

At this moment there is no definite site from where you can check this.

earlier www.Zabua.com used to publish import-export data for all this chemical.They have stopped the update starting from end 2016.But you can search in Indiamart. Lots of small company publish price over there.You can try.I generally track management.

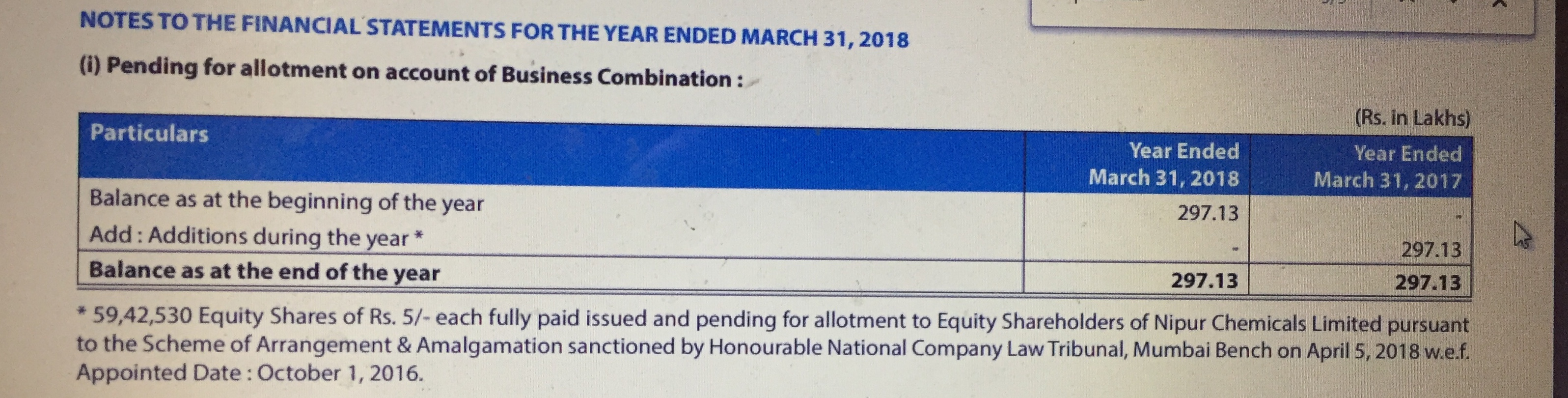

ABout 59.4 lakh equity shares of 5 Rs each are yet to be allotted on account of nipur chemicals merger, that is 30% dilution coming up in near future. Is this understandin correct? So fy18 eps actually is 18 instead of reported 25?

Second, assets allocated to solar segment is 197.58 cr as per fy18 annual report and profits generated by solar is just 2 cr. This is a case of capital miss allocation. Is there somebody with knowledge on solar business? Could someone provide long and short term return expectation from a solar project in general? I believe solar investment does not provide more than 12% ROCE from what i have heard.

Amalgamation is already completed and dilution has already taken place in May 2018. June quarter result reported EPS of 8 Rs per share post-dilution.

Further as per June 2018 Quarterly results reporting, revenue from solar power segment is 8.55 crore and profit from the same is 2.75 crore. So converting these numbers in annualized terms profit from Solar power segment will be approx 11-12 crore. Majority of loans take for the same has been repaid.

Amalgamation with Nipur chemical will further improve synergy.