I found there was no discussion on this particular counter so wanted to start a discussion.

BHAGERIA INDUSTRIES LIMITED was established in 1989 with an objective to serve the dyes & intermediates industry all over the globe. Company commenced its operations by setting up a Vinyl Sulphone Plant at Vapi (Gujarat) with capacity of 540 T.P.A. which has now expanded to 3600 T.P.A. Subsequently Company has gone for further expansion in other Dyes intermediates & Dyestuffs.

Nearly 70% of its production is being exported worldwide to various clients including multinationals.

Our products are being exported to Korea, Japan, Taiwan, China, Germany, U.S.A & other European and African countries. Today Bhageria Industries Limited is one of the largest Manufacturer & Exporter of Intermediates and Dyes.

Here are some of the highlights

CMP - 120 CR

NP - 36 CR FY15

P/E - 3 to 4

ROE - 30 % plus

ROCE - 30 % plus

No Equity Dilution

Last 15 Years strong Dividend payout

Major capex completed (See rise in sales figure)

Chemical industry of India had some bad years till 2013…2014 was the year of huge profits for this industry…There are reasons for this…regulations were passed In china during this time for strict environmental laws…this led to shut down of many chemical companies in China. Indian chemical industry used to face stiff competition from china…a pure demand supply mismatch over a period of time…a cartel was formed among these indian chemical companies like bageria and bodal…to shoot the price up …chemical selling for 100₹ was selling for 400₹ …so not a big surprise if these companies are doing good…its the industry not the company that has improved…this can be recommended for your own portfolio…but not for your client portfolio…situation can change soon and again china can pump in back…this story is similar to that of cement hike in south India…companies like Deccan cement…ncl industries etc have enjoyed good profitability…

One thing is not sure here is when the industry will change? How far is the threat from china? I guess this is the reason why the PE is not re rated…there is no sustainable growth seen here…

This looks like a Unique company with some great numbers in last two years, Excellent ROIC and Capital turnover.

They are getting into food processing buisness but need to figure out the huge increase in Capex, Has all of it gone to growth or maintenance as well .As per thier latest AR they just hae 19 employees and is quite strange , Time to dig !! Rest of the VP member Please share your Views.

Specifically on exports to China of Bhageria as well as other dye and intermediate manufacturers: How is the Chinese slow down likely to affect offtake? Any Chinese manufacturers that can substitute taking advantage of Yuan devaluation?

In general, I think the Chinese economy is going to play a big role in the fortunes of export led B2B companies in 2016.

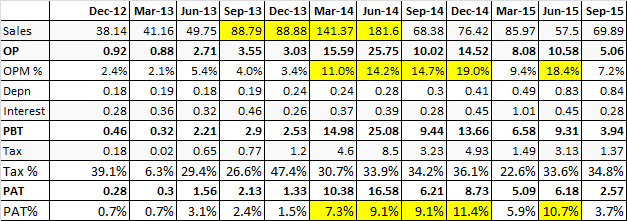

The initial look at the numbers got me interested. But something happened between Sep’13 to Jun’14 (4 quarters) which is tending to skew the numbers.

Sales shot up in this period, and tapered down later. OPM and NPM improved substantially, with some lag, and are fluctuating thereafter.

These numbers have improved the ROE and ROCE in the last 2 years and I am trying to find out what happened in this period. I think that traded goods had an impact on this. But what happened later? Did they stop trading and concentrated only on manufacturing? If yes, then will the numbers revert to the earlier periods? Not much information is given in the 2014 and 2015 annual reports.

They have also ventured into solar power generation during 2015 and are setting up a plant with investment of Rs. 11 cr. Why should they do this instead of focusing on their core business?

Some positives are:

Full tax paying company

Cash and investments are Rs 42 crore as on Sep’15 (Rs 25 cr as on Mar’15), which is about 38% of the market cap. This makes it look like a statistical bargain.

Consistent dividend payer for the last 22 consecutive years (company is in existence for 26 years).

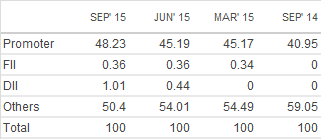

Consistent buying by promoters. They have further bought shares in Nov increasing their stake to 48.58%

There is a positive swing of Rs 11 cr (appx) in working capital between Mar’15 and Sep’15 (receivables and inventory have reduced by about 4 cr each and creditors have increased by 3 cr). This will positively impact cashflow from operations.

Debt has further reduced as on Sep’15. Debt equity is 0.15 (0.25 as of Mar’15). No long term debt.

Thanks Vinay for Analysis.

Gone through their last Annual Reports, Few of obvious red flag I observed are -

a) Salary of the Chairman Executive has been raised 158% in last year (Any specific reason).

b) Though company is in chemical business from last many year, they are not talking any opportunity from the other growth drivers. They still want to focus on the same business through the indigenous process, which is already at mercy of China’s play.

Results were pretty bad if one were to expect comparable ones on a Y-o-Y basis. That’s because H-acid contributed heavily to the margins, as I later found out after digging through news archives. The below data is from Zauba, for HS Code 29222160, which I believe is the right code.

I could not see a similar correlation for Vinyl Sulphone prices (most probably HS Code 29041090) and the company’s OPM. Here are a couple of writeups on the contribution of these chemicals to the profit growth of the company.

Company now seems to be getting into solar energy space, and has won an award from SECI, which seems to be holding up the stock today despite the comparatively poor earnings. I have no idea about the size of the contract and this was not disclosed in any exchange filing.

SECI Project win is something strange as company has not mentioned such an important announcement on stock exchanges (Which is must considering, required investment for 30 MW solar project)

Further, This project win is at aggressive price Rs 4.41/Kwh with zero VGF. At this price, there is no profit left and may be there could be some loss in supplying power at this rate. (read no RoE).

Investment required will be about Rs 180 Crs (considering Rs 6 Crs / MW).

I am awaiting further details from company / other sources to understand their rationale for quoting such an aggressive price for 30 MW Solar project.

The disclosures or lack of, to exchanges is something to note. Usually receipt of letters of allotment from SECI are announced by companies. I’m willing to give a benefit of doubt if the letter of allotment has not been issued. The other thing that nagged me is the lack of shareholding pattern for the Dec’15 quarter. Again, I can give a benefit of doubt, because I noticed this for a few other companies.

On the financials, I don’t find a reason for the realizations from dye intermediates to reach previous highs. A forward EPS of around 12 (4 times previous quarter EPS) is what I foresee. Which makes the solar energy segment the unknown quantity for now. I’m ignoring food processing, because of lack of news on that front. Average RoE of solar projects over the lifetime of 25 years is around 20%, but without enough data on revenue projections, costs and sources of funding, it would be difficult to estimate when the earnings will start to reflect in the results and how much of drag it would be.

Whether the stock is currently undervalued or overvalued would depend on what visibility can be gained into future earnings and what earnings multiple can be assigned to this company.

Project is expected to completed by first quarter 2017.

Installed capacity would be 3MW by March 2016.

Plans are for 50 MW capacity in Maharashtra by March 2017.

Would be interested to see the impact on the balance sheet, due to entry into the solar sector. Don’t have enough info yet, to do a SOTP valuation of the company.

I don’t have any verified confirmation on the shutdown of Hubei Chuyuan (or Hubei Hwalle Dyestuff Industry Co., Ltd.) though - news from Chinese sources are not easily searchable. Time to start tracking export prices though, which is a good enough lagging indicator.

Out of profit of 36 crores, 21 crores are invested in …Mutual funds! One is not averse to parking money in short term liquid funds. However of the 21, only 5 crores are parked in Short term funds. Rest of money is invested in Equity funds and even a stock - HDFC bank ! Really?

The Capex the company has made of 10 crores is not in its core manufacturing facility, but rather in Solar power plant. I am not clear on the economics of solar power plant- but let’s assume that their current power & Fuel bill comes to zero from current value of about 2 cores. Ok, so this gives a decent 20% ROI, not bad. But Bhageria has been having a ROIC of about 38% for their core business & better than 40% ROCE over 3 years, so settling for 20% ROI seems strange. Unless there is no avenue for further growth of core business, this investment in Solar power plant seems a case of capital misallocation.

Regarding shareholders - two of them viz Prism Scan and Reform Traders seem to belong to same family i.e. Lohiya & together their holding comes to about 9%. Also Choice Equity and Kamal Poddar are related entities, holding another 6%. Prism is mentioned to be a Software company and Reform traders is a commodities, trading and commission company. S P Tulsiyan is a member of board of directors too.

Zero investment in R&D, couple this with no meaningful investment in core chemicals business, it appears the company does not see growth ahead worth investing in.

The core business of commodity chemicals is not easily scalable. The process for manufacturing the chemicals (specifically H-Acid) generates a lot of pollutants due to the use of high strength acids and alkalis. Treatment of runoff is necessary to prevent groundwater contamination. The pollution norms in the developed world ensure that such units are unsustainable there. And as for the developing world like China and India, one should expect pollution control boards to start cracking on polluting units until they clean up their act (there is a similar discussion on Shree Hari Chemicals on this topic). This puts a cap on how much installed capacity can be added.

So, it’s not surprising to see management diversify to other areas. The question is whether this is diversification or “diworsefication” in the longer run.

Thanks for clarifying. The AR for 2015 is very clear that this is more to save operating expenses than diversification or diworsification. They say, The company is constantly exploring avenues for cost saving as an on-going process. To utilise the alternate sources of Energy Company initiated to setup a Solar Power Plant at Capital Cost of Rs.1097 Lacs.

There is recent run up in the share price post publication of 1QFY17 result and announcement of sub division of equity share of Rs 10 into 2 shares of Rs 5.

Does anyone knows any other factor in addition to above for such sharp run up in share price with huge volumes (17 & 18 Aug-16).

Due to the china factor, most chemicals companies will report good results since the price of end product have risen by 80-100%. As the management have already confirmed that they do not expect any rise in their sales volume, the share is fairly valued at currently levels. The stock have shoot up due to good results courtesy china play and the stock split. 350-400 is the target where I will look to book 30% of my profit. Invested since 120 level.

There are chances the stock might touch 500 also due to the momentum. I plan to continue holding rest of the investment post booking 30% profit at 375-400.