Could not find much data on this company. Mgmt does not conduct oncalls, press releases etc. Can anyone throw some light on near/mid/long term growth triggers for this company. Textile as a whole sector has multiple tailwinds which could increase demand for cotton machineries but apart from this are there any other major growth triggers ?

1 Like

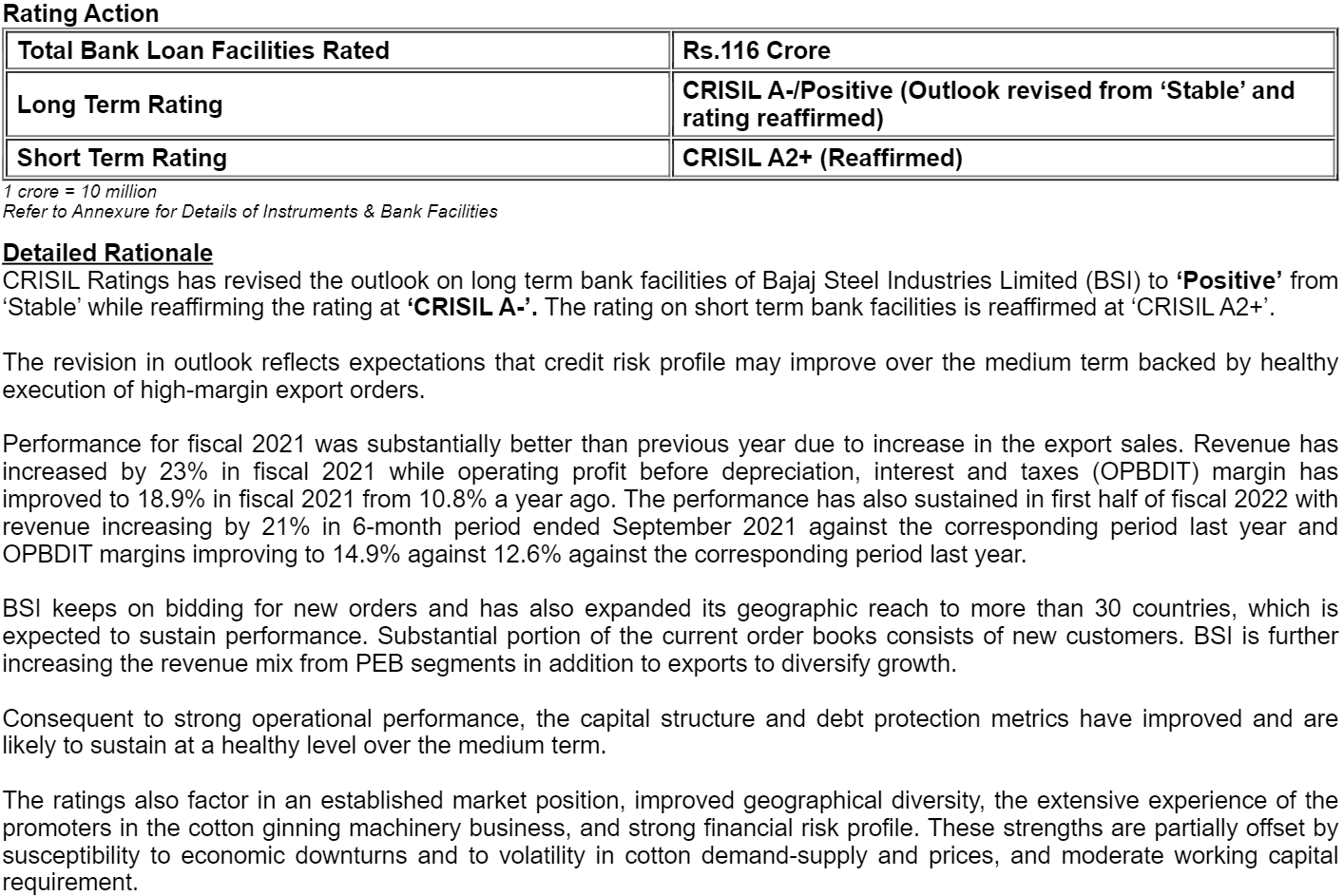

Bajaj Steel- Highlights from Annual Report (FY 2020-21)

-

The increase in turnover is attributable to the better explorement to new markets

-

The profitability of the company has increased due to the increase in turnover including exports orders which has resulted in better allocation of fixed expenses.

-

The company has developed Drying & Humidification Systems for cotton and cotton seed which are under testing

-

The general engineering fabrication and machining work are now being undertaken by the company to enhance the capacity utilization.

-

The growth potentials of products of all the divisions of the company are good. The Company is also expanding its activities in the selling of complete firefighting systems including Fire extinguishers, Hydrant systems, Sprinkle systems and Fire Diversion Systems and Steel Doors etc

-

The future outlook of the company appears good as the cotton sector is doing quite well and with increased income in the hands of cotton producers more demand for the new plants machinery is likely to be there in the near future. The other sectors of operation of the company are also increasing their order booking to improve the working of the company.

4 Likes

Dramatic decline in all segments.

Company is not bad, but no interaction with investors, maybe growth was just because of entering US and African market. Trying to do too many things, not worth the risk, as it is business is bound to be deep cyclical, once cotton machinery is bought, repeat/replacement sales will be tiny, difficult to predict growth here. Better to stay invested in predictable, well analysed, transparent biz

It may also just be a game to allow big fishes to make entry bit cheaply

Disc: exited

1 Like

Good video on cotton processing. Refers to cotton gin and one can see Samuel Jackson machines being used

They have a tie up with SJ

Disc- tracking position

5 Likes

")

Bajaj steel - a lot seems to be changing, from a majority one product / one industry/ india focused to more of a engg solutions provider/ multiple industry /multiple country player. Corporate video above gives a good idea.

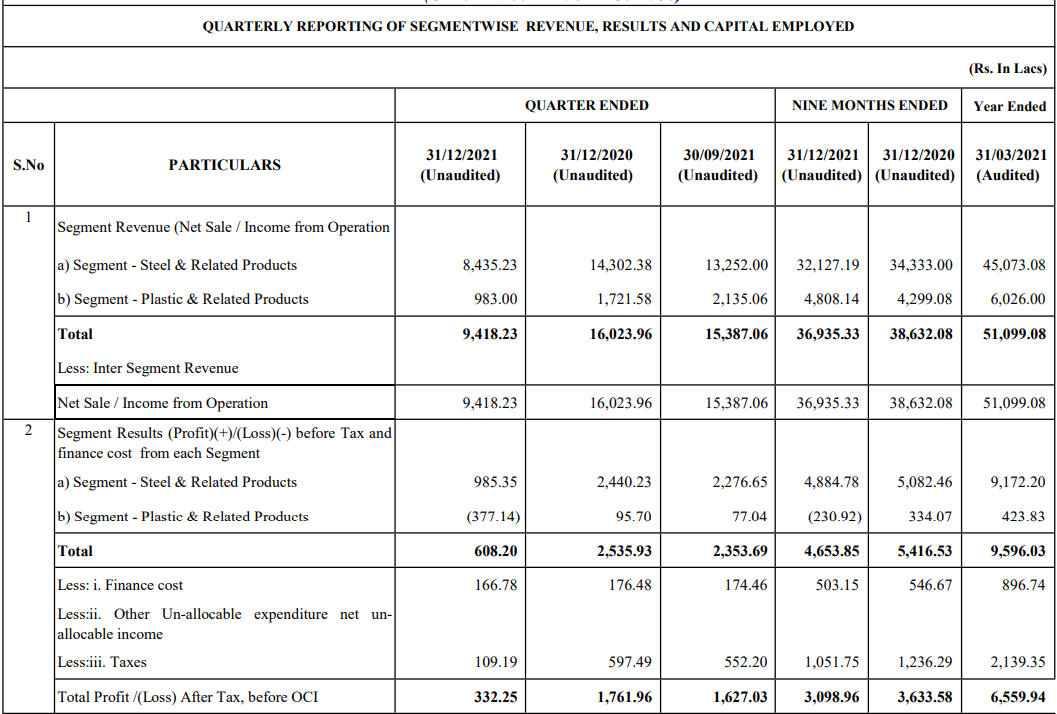

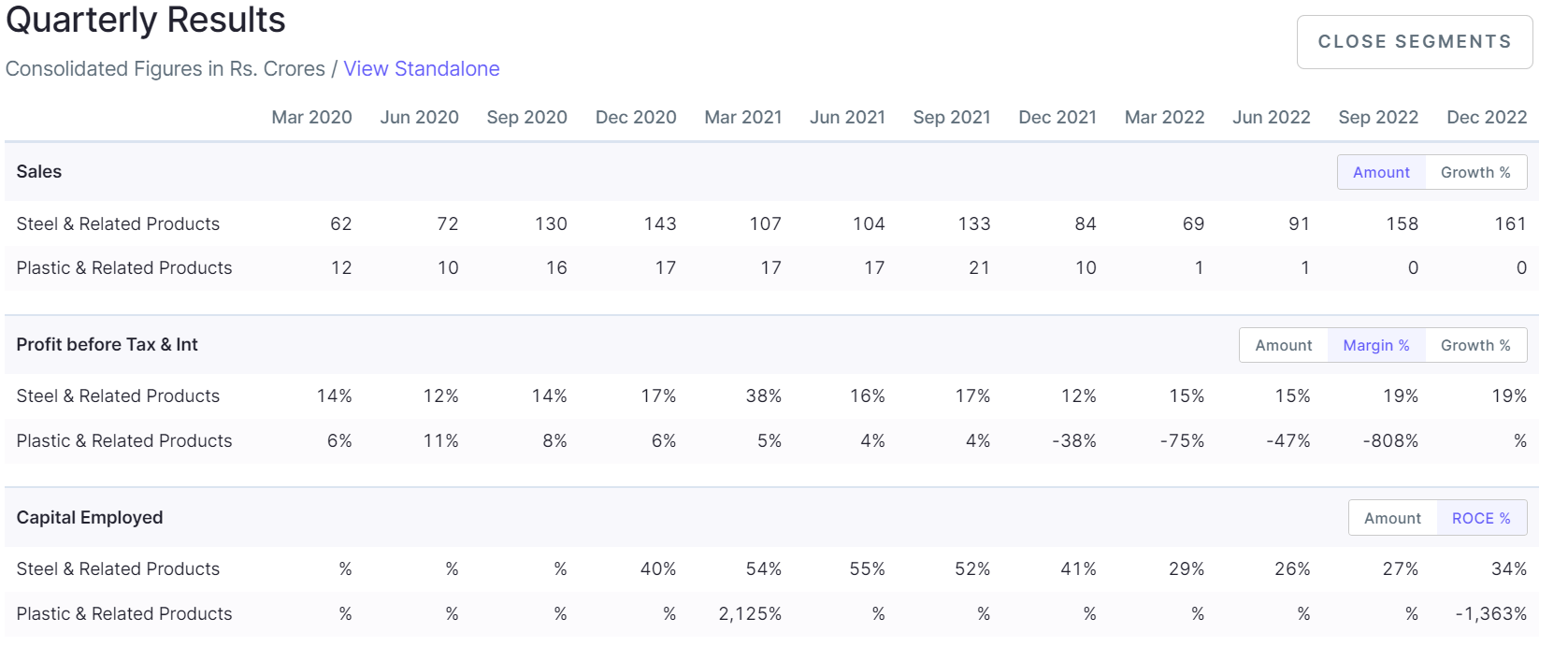

quick glimpse on numbers

recent developments

- Hived off loss making business

- Exiting of a set of promoter (took plastic biz) - clean run for current set of mgmt

- per recent credit report - sizable order book from PEB(pre engineering bldg - infra play - has done 1000+ projects per website) and many new customer + new geo for core biz

- Stable margins across last few qtrs (wd be better once hived off plastic biz no hit goes away)

- Focus on consumables + exports helping remove cyclicality for ginning machine consumables - AR and credit reports give good insights

- Strong export trajectory to US (via Baja coneagle - local setup in US)

- Good price action with good delivery based accumulation

- textile revival should augur well for ginning mills (a sizable end customer biz), as well as RM cool off to help

- Since they are one of majority player in ginning machinery exports - one can track same to get idea of trend - though that is not the only thing they do

Valuations - TTM basis 11PE is not demanding for a ginning leadership co and leadership position in ginning machinery and upcoming PEB verticals to expand opportunity size, clean bal sheet. Promoter holds substantial stake (incldg grp co under pulic holdg) and have increase recently.

Risk - Still ginning(cotton processing) heavy, Q2 and Q3 traditionally has been stronger though trend is smoothening, upcoming Q4 numbers need to confirm same. Not much communication from mgmt. to market besides YT channel. Success of other verticals stay a key watch out.

Conducive price action with good delivery % indicates accumulation. closer to ATH

D - Invested

15 Likes

This one is setting up well on charts if anyone’s tracking it. Textile sector has been picking up off late and it could be ripe for its second run.

1 Like

ginning machines are neither a high growth business, nor a large market, replacement cycles are long. any benefit from textile growth will be limited and with lag. just look at their 3/5/10year sales CAGR

they have a few other segments - engineering & construction, plastic batches, etc. which are not material yet.

2 Likes

I have shared my thesis on Bajaj steel & why people might be discounting it as a Ginning machine business, however, it has slowly transitioned into a multi-product engineering company.

Link- https://youtu.be/w-FfbXerPGo?si=VSB2LwPILRgQODN1

Disclosure - Holding

7 Likes

Company has put in some efforts to come up with a good presentation this time, explaining different verticals as well as capabilities/clients/credentials , deserves credit for incubating and scaling non ginning verticals. Though imv company has done periodic updates via YT more focused on capabilities and helps both prespective customers and investors to get a good glimpse of company evolution in recent times

Here is the latest Investor deck

https://www.bseindia.com/xml-data/corpfiling/AttachHis/6dbc774f-a7e9-48c1-b8e2-6654bc552f60.pdf

as usual Mr Mkt has sensed and rewarded them

if we were to look at each vertical and possiblities

- Cotton/Ginning machinery - Based on some cursory search and some of YT videos of mgmt (https://youtu.be/jqTKy7azKTU?si=tvMHVxdnArt5esBy ) , Ginning machinery is small mkt worldwide with 1200 cr and Bajaj probably holds 500 cr - looks like last man standing and will continue to do so backed by capabilities of supporting all formats of ginning machines, some potential of policy support for productivity aspects in India as well hinted in above interview. A good cash cow businesses which has helped mgmt incubale other verticals

- PEB/Infra - Dhruv has nicely covered this fast growing industry segment in his videos, Pennar ind is peer which is highly bullish on this segment and we all can see massive structure of industry expansion all around india leveraging PEBs - near term potential for Bajaj per deck . Comany new capacities coming online in Q4.

- Electrical panel division very relevant and fast growing segment of both energy and capax value chain - mgmt here talks about right to win https://youtu.be/lG6MpP_Li-Q?si=ZUs-mzaKy4pWM6E7 , new plant coming online in H1 26 which will increase capacities multi fold.

-

Heavy engineering - some serious clients and heavy engg products delivered (including Aero bridges)

-

Other engg products also appear well thought an niches extending on their enginnering capabilities -

e.g. Specialty conveyors, • Fire fighting systems, • Industrial fans and impellers, • Hydraulic cylinders, • Power transmission products, • Office Furniture, • Steel Doors, • Ducting’s for various applications.

Financials - front and underneath

This is a good view on transition belwo the front nos whch looks nothing great to boast of on cursory looks

coupling the Order Book in hand and capacity expansion in each vertical (outside cotton) - 1 year from now picture will tilt in favor of other engg dominant trajectory from current state of Cotton heavy to engg incubating.

- Growth Drivers - multiple capacities coming online in coming 2-3 quarters, backed by OBs

Cherry on cake

- Front runner in Torre-faction plant and Bio Mass Pellets Plants for reputed clients like Prime metals - USA , Danelli,- Italy, Prodesa, -Spain, TSI- USAetc. Government of India mandated the usage of Biomass Pellets in Power Plant Industry of 5-7 % as coal substitute, this provides an opportunity to the Company to manufacture and sell such machineries/structures - This particular vertical has policy support with govt manadting usage going up to 20% Ashish Mittal on LinkedIn: I have been working in biomass industry since last several years and as…

- Very high OB in Cotton ginning machinery - a boost in H2 - for context typical qtrly run rate is sub 130 cr/qtr - need to see if this OB has long legs for FY26

All in all a very small company out of nagpur region becomes world leader in an engineering segment, utilizes the cash flows to incubate multiple relevant and high growth engg capabilities and signs of becoming a serious contender in each of them(pristine balance sheet and no dilution yet to deliver this growth), nimble to let go of businesses which were a drag ( plastic biz spin off) , New generation(Luv Bajaj) actively involved and professionals running each BU - all of these while India itself offer lot of opportunities can mean a lot can happen here on.

Risks - regional mfg concentration near nagpur may need a relook at some point, Cotton ginning spikes/seasonality may continue to affect QoQ variances though it shd reduce as other vertical scale meaningfully in future

D - Invested

11 Likes

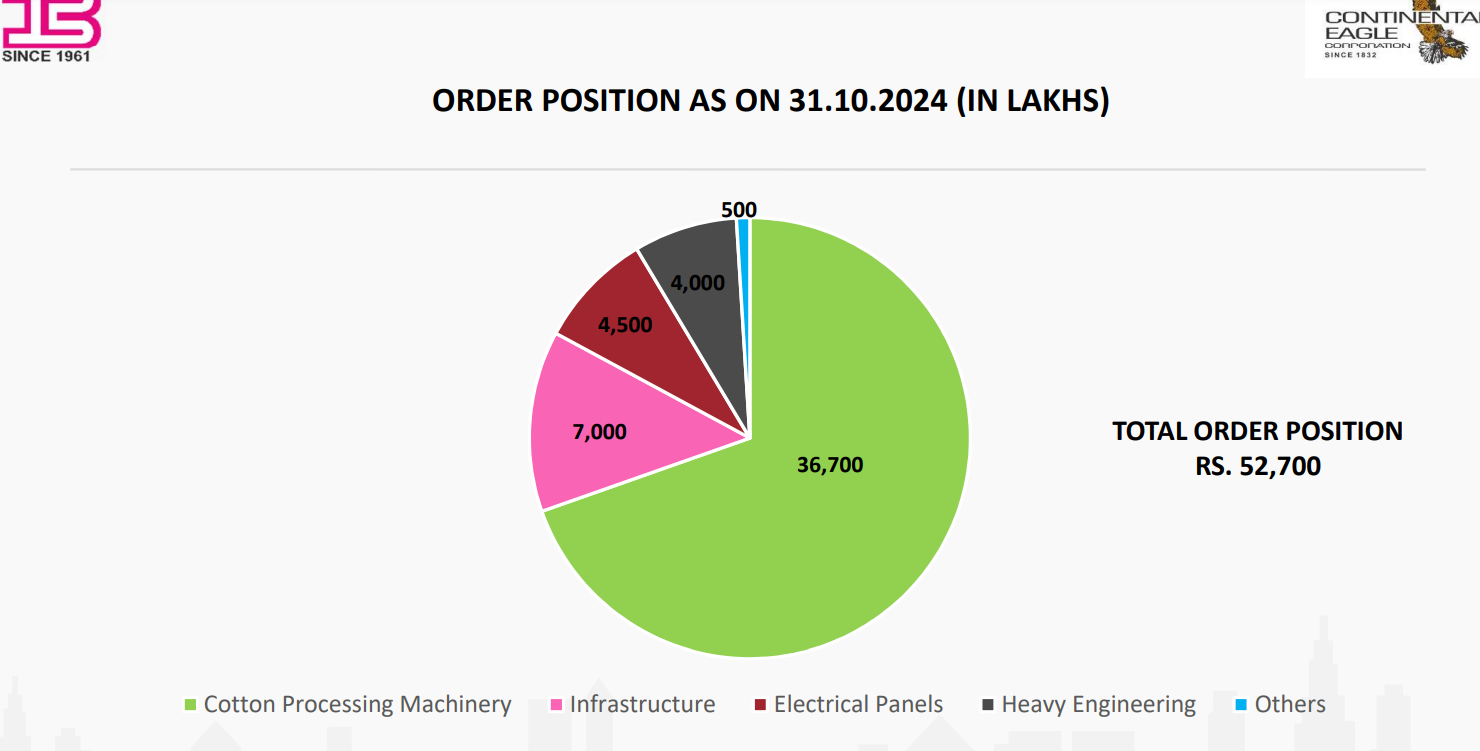

Do we have details on the total open order book? Unable to find it from the latest presentation.

1 Like

slide 18 in deck has OB and breakup by segment as well, deck also mentions execution timeline for each segment execution as well in earlier slides, going by that H2 could get closer to (500 cr+) 1.7X of H1 (sub 300 cr), if delivered - a significant feat by all means

3 Likes

Thanks for sharing the slide. What i am trying to understand is whether this run rate (1.7 X H1) is sustainable beyond H2. Maybe, pipeline info would have helped.

1 Like