BFL owns 88% of BHFL and through this you are also the owner of BHFL if you own BFL.

The stake of BHFL was sold to new shareholders while listing and the amount recieved is infused to BFL. You will not recieve the share cause you are the seller indirectly.

1 Like

Credit cost is revised for current fiscal by 20 bps owing to higher npa in the first half. For the current year target is 1.95 to 2.05. Though the company believes it has peaked and the credit cost should cool off in the H2

This demerger IPO topic is discussed already.

Selling at a discount compared to historical numbers for sure. I suppose that FIIs not buying (less demand) + Jio overhang is probably affecting the stock.

Fundamentally, there doesn’t seem to be any issue at all, its doing better than peers and growing close to 30% like it has been doing for decades.

2 Likes

A basic question. What is the formula for Gross loan loss and provision.

For example in present quarter it is 1934 cr while if I subtract the provision of 30 Sept from 30 June I am only getting 433 cr. Does it include any other component also which I am missing ? Even if I add incremental NNPA, it is only adding ~350 more.

Do direct to relevant post/ thread if it’s already been discussed.

Is there something about this stock that we don’t know but market knows.

Its unbelievable that while the profits/revenues have grown by more than 100% over last 3 years, the price hasn’t moved one bit!

With a 20-22% ROE, the EPS double from here in next 4 years. The current PE is 26. If the price doesn’t move, then the PE will come down to 14.

A company growing with 22% ROE and 25%+ top/bottom line growth cannot be trading at 14. It hasn’t happened before unless there are nasty surprises along the way.

What are we missing here? Some say that its because of Jio financial hangover but is that really true? Of course Jio has lots and lot of capital but so do many big banks. Is it really this easy to build a granular consumer book, the kind of that Bajaj Finance has, that market is jittery about Jio financial?

14 Likes

The following thoughts may look alarmist and I am not invested and clearly negatively biased, so please do enlighten me if I am wrong. This stock is much mentioned on Twitter and many are making similar arguments as we see in this thread.

The net NPA are increasing. This as of now is a small thing, but perhaps a sign of building up of stress in the economy. Retail loan growth has stagnated industrywide after RBI expressed worries about these loans. Household savings have dramatically fallen in the country and everyday I see people not able to service loans or just evergreening them(taking more loans to pay old ones). Granted, these are only from personal loans and my data is anecdotal, but there are too many anecdotes. I am sure all of you know a few such people. Economy is unmistakably slowing down. I think we are in for a broad(not specific to this stock only) PE derating phenomenon. The party cannot go on indefinitely. Cholamandalam has comparable ratios and has always been in the same zone of PE as Bajaj is for now.

3 Likes

Nothing wrong with the stock. It was trading at 12 times book in October 2021 when it made its all time high. That was clearly not sustainable even with 20% ROE. Large private banks (HDFC, Kotak) do 16-18% ROE and they trade at 2-3 times book.

So stock had to go through a time correction which I believe was mostly done by end of last year. But then RBI put a spanner in the works by tightening credit supply and which along with high cost of borrowing is acting as dampener. On top of this we have seen general FIIs selling which is always an issue for FII owned stocks.

Come next year and with rate cuts stock is expected to find its mojo back.

P.S.- For a more balanced perspective one should look at Bajaj fin valuation before and after housing finance demerger. Even after demerger, standalone business still trading at the same valuation as it did before demerger. So some value unlocking has already happened for the investors.

11 Likes

Long Range Strategy presentation

1 Like

Does anyone have the recording of the LRS presentation? Couldn’t find it on the IR section of their website or researchbytes.

Thanks in advance.

Bajaj Finance -

Q2 results and concall highlights -

Q2 consolidated financial outcomes -

AUM @ 3.73 vs 2.90 lakh cr, up 29 pc YoY

Interest Income @ 14.98 vs 11.73 k cr, up 28 pc YoY

Interest expenses @ 6.14 vs 4.53 k cr, up 36 pc YoY

NII @ 8.83 vs 7.19 k cr, up 23 pc

Other Income ( including fee + sales of services, net gain on fair value changes ) - 2.10 vs 1.65 k cr, up 27 pc

Net total Income - 10.94 vs 8.84 k cr, up 24 pc

Operating expenses - 3.63 vs 3.01 k cr, up 21 pc

Pre Prov Operating profits - 7.30 vs 5.83 k cr, up 25 pc

Laon losses and provisions - 1.909 vs 1.077 k cr, up 77 pc

PAT - 4014 vs 3551 cr, up 13 pc

New loans booked in Q2 @ 97 vs 85 lakh in Q2 LY

New customers added in Q2 @ 39.8 lakh. Aim to add 1.5 cr customers for full FY 25. Total customer franchise now stands @ 9.2 cr. Cross sell franchise stands @ 5.7 cr customers

Total employee head count ( Bajaj Finance + Housing finance + Bajaj Fin Securities ) @ 59.4 k employees. Added 4k new employees in Q2

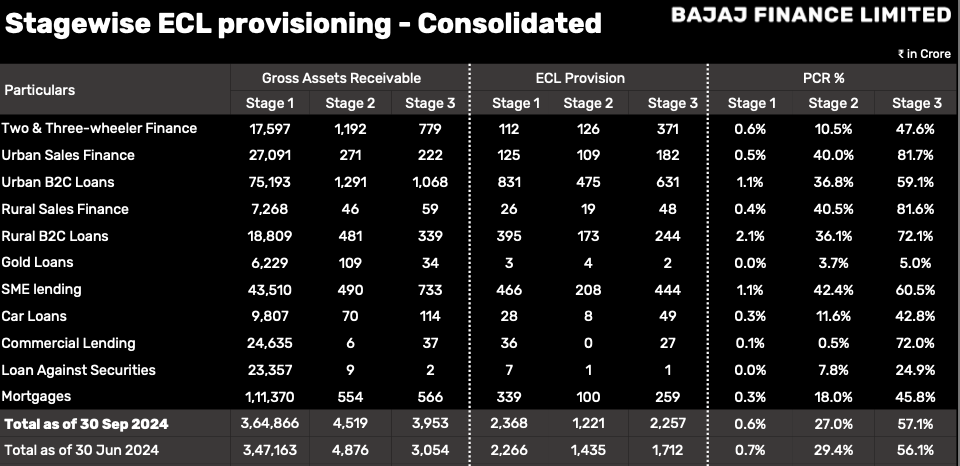

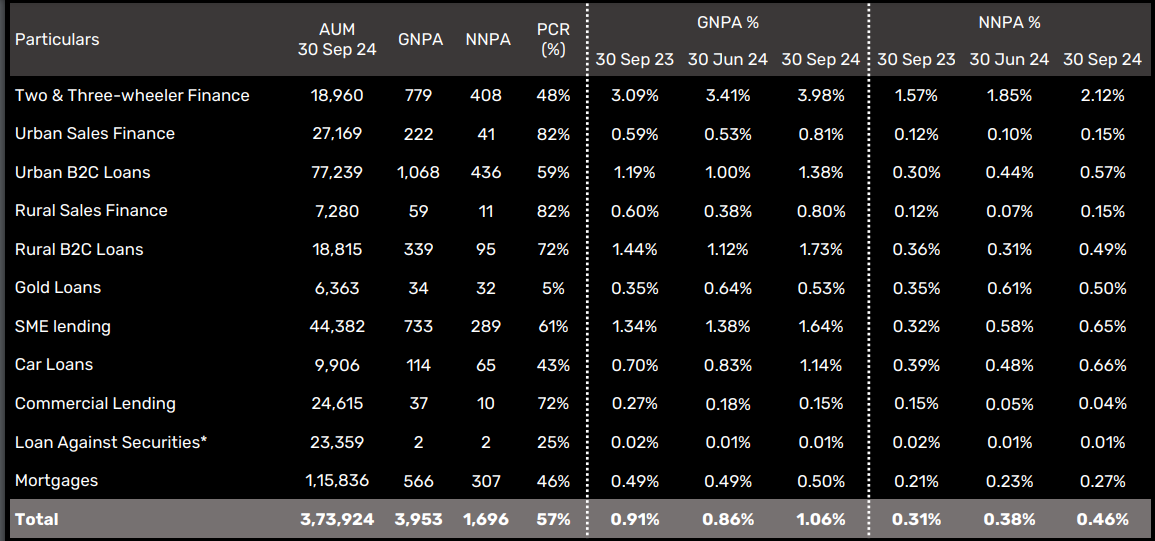

Gross NPAs @ 1.06 vs 0.91 pc

Net NPAs @ 0.46 vs 0.31 pc

In Q4 LY, Bajaj Auto started their own captive finance company by the name - Bajaj Auto Credit limited. As a result, Bajaj Finance’s share of financing of Bajaj Auto’s 2Ws and 3Ws has fallen sharply in Q1

Breakdown of company’s AUM ( loans ) as on 30 Sep 24 -

2W + 3W loans - 18.9 k cr

Urban sales finance - 27.2 k cr

Urban B2C loans - 77.2 k cr

Rural sales finance - 7.2 k cr

Rural B2C loans - 18.8 k cr

Gold Loans - 6.3 k cr

SME lending - 44.4 k cr

Car loans - 9.9 k cr

Commercial lending - 24.6 k cr

LAS - 23 k cr

Mortgages ( under Bajaj Housing Finance ) - 115.8 k cr

Total users of Bajaj Finserv App now stands @ 6.1 cr

Consolidated cost of funds stood @ 7.97 pc, up 3 bps on a QoQ basis

Opex to Total income stood @ 33.2 pc vs 34 pc YoY

Annualised employee attrition was higher vs LY @ 16.4 pc

Credit cost was elevated in Q2. Similar was the case in Q1 as well. Net increase in Stage 2 + Stage 3 loans in Q2 @ 542 cr vs Q1. Credit losses are inching up across retail and SME lines of business and across all geographies. Gross loss ratio in Q2 was 2.16 in Q2 ( @ 1909 cr ). It was 2.12 in Q1. Company estimates this ratio to fall below 2 pc by Q4. Company estimates its gross loss ratio for full FY 25 to be around 2.05

Bajaj Finance started doing non Bajaj Auto related 2W financing in Jun 22. That business has grown to - financing 35k vehicles per month. That means an annual run rate of about 4.2 lakh 2Ws. In FY 24, company did financing for 8.64 lakh 2Ws for Bajaj Auto - which in future won’t happen because of commencement of operations of BACL

Company expects to scale up their 2Ws business to about 7 lakh units by FY 26 ( after the loss of business caused by BACL )

Company believes, every 25 bps cut in Repo rate should improve their NIMs by 10-12 bps. However, company may not take the advantage of repo rate cuts via higher NIMs but via improving / increasing their secured portion of business by growing them at a faster rate

GenAI is helping company improve their operational efficiencies

Rural B2C business is now picking up some pace after growing in single digits for last 6 Qtrs. Company hopes to grow this segment @ 12-14 pc for current FY and accelerate this segment’s growth in next FY

Company did enter a lot of new lines of business in last 2-3 yrs. As these businesses are now maturing, this should give them some operating leverage and help them further improve their Opex to Total Income ratios

Out of the 4000 employees added by the company in Q2, around 2000 have been added in relatively remote geographies. This should help them fuel further growth in under penetrated areas

For full FY, company is forecasting an AUM growth of about 25 pc ( despite the run down of Bajaj Auto’s captive business )

On retail lending front, most of the stress is seen from clients having 3 or more unsecured loans. Company has reduced its exposure to such clients from 13 pc of total clients to about 9 pc now. Also, RBI has been pushing both Banks and NBFCs to reduce their exposure to unsecured lending

New lines of businesses where the company is yet to break even include - New Cars finance, CV finance, Gold Loans, Tractor finance. These new lines of businesses are helping company boost its AUM growth by 2-3 pc from say 23-24 pc to 26-27 pc

Company is seeing strong disbursement growth in their B2C - consumer durables finance business which is up 21 pc in current festive season vs last festive season. In Q1, Q2 - this business had grown disbursements by around 9 pc. Clearly, the festive demand is strong

Disc: holding Bajaj Finserv from lower levels, biased, added recently, not a buy/sell recommendation, posted for educational purposes only

8 Likes

What demerger and value unlocking are you talking about? Bajaj Finserv/Finance investors have not got any shares of Housing Finance. It was an IPO.

Bajaj Housing Finance (BHF) was a subsidiary of Bajaj Finance which got listed separately so any reason you think it’s not a demerger?

It’s a different thing that management went through ipo route instead of just giving shares to existing shareholders and where a few (not all by the way) of the latter missed out even though there was a special quota for them.

And even if you didn’t get shares of BHF, after demerger, you are still a shareholder in the latter and will gain from any appreciation in its stock prices.

Finally after demerger, operational metrics (e.g. NIM) of Bajaj Finance are going to improve especially with credit costs expected to come down later this quarter which should lead to valuation rerating.

It wasn’t a demerger because BHFL was already a separate compny even if wholly owned by Bajaj Finance.

Demerger is the creation of a second company.

The ipo doesn’t have any operational relevance to the business.

Don’t agree that IPO doesn’t have any operational relevance to the business. Before demerger, Bajaj finance’s operational metrics included BHF’s P&L. Post demerger, market will value Bajaj Finance on new risk profile, asset quality, loan book mix and NIM growth.

Bajaj Finance still holds 88.75% in BHFL - so for all practical purposes don’t think much has changed? Management said something along these lines in their quarterly call

Bajaj finance is a shareholder in BHF that sold ~12% of its stake. The ipo doesn’t change the corporate sturucture of BHF or Bajaj finance. Its not like a section of BAF’s operations were separated and created a new company or BAF reduced operational control over BHF.

That investors value it differently is a different matter but in terms of running the business things are as they were.

By your logic every ipo would be a demerger.

Of course we would gain for appreciation in the stock price. Only if the appreciation in stock price happens.

Basically the point is the demerger has not helped the existing investors in any way directly. Housing Finance is a separate company now and people had to put more money through IPO to get the shares in that.

Demerger is helpful when you as an holder of parent company actually gets those shares and then value unlocking happens. Example: Jio Financial, Aarti Pharmalabs etc.

Bajaj FInance | Q3 Concall

FY26 guidance

PAT growth of 22%-23%

AUM growth of 25%

Credit cost at 2%; provided Q4 is at 200-205bps

Lever available in terms of fee income & operating expenses

Risk followed by margin & then growth would be the priorities

Well on course to add 17 mn customers by FY25

On track to cross 100 mn customer franchise by FY25 end

Laid out a comprehensive 15 months succession plan; 12 months completed

Expect board to take a decision (on Rajiv Jain) by Q4FY25

3 Likes