Who is to say what is the right multiple. Gruh used to trade at 5-6 times price to book in 2011-12 and the consensus was it is very expensive eventually it went on to trade at 17 times P/B in 2017 before settling at a P/B of 10-11. PayTM which makes bigger and bigger losses each year gets a valuation of around $17B. If you look a little ahead (FY21) BAF’s book value should be around 700 and EPS around 140, which gives a P/B multiple of 6 and P/E of 30. There is no guarantee that the said growth rates will be achieved but then there is nothing guaranteed in the stock market.

7 Likes

Valuations of a company depends only upon the company’s fundamentals and the price it is trading at. It should not depend upon how trendy the stock is (just a general comment, not commenting on Gruh as I never followed this company)

P.S. I don’t think Bajaj Finance is overvalued. Though I haven’t invested, but I will definitely invest if the stock corrects from here.

I don’t think there is a connection with karvy fiasco and bajaj finance. LAS is an easy business with 100% secured and liquid security backing…

Remember Global Trust Bank. LAS is not an easy business. You can get carried away very easily. Post GTB fiasco only RBI came with LAS Limits.

yes… that’s true… they were funding pretty heavily to stock market traders against securities… Only way to screw LAS funding is, funding against financially weak / tumbling shares without appropriate hair cuts and delaying margin calls / selling shares…

How does Karvy fiasco affect Bajaj Finance? I am not dismissing your statement, just curious about it.

Their LAS book is about 7000 Cr.

Disclosure: Bajaj Finance is the single largest holding in my portfolio.

1 Like

It would affect them only if they have funded Karvy.

If it’s TRUE and If suppose they re call even 50% LAS loan book, how would they show loan book growth in December quater!?

Read somewhere on Twitter… I cannot verify any information myself.

Disclosure: invested

You mean to say that if BFL had funded Karvy’s loans, fradulently taken against shares owned by Karvy’s clients? Cannot be ruled out, but seems highly unlikely given BFL’s underwriting standards.

As far as I remember from the concalls, the MD had mentioned that since they are already into LAS, it makes sense to get their LAS clients to trade through Bajaj’s broking business. So it seems like most of Bajaj’s LAS clients were individuals. Bajaj Financial Securities Ltd has commenced its broking and depositary service business during Q2 FY20.

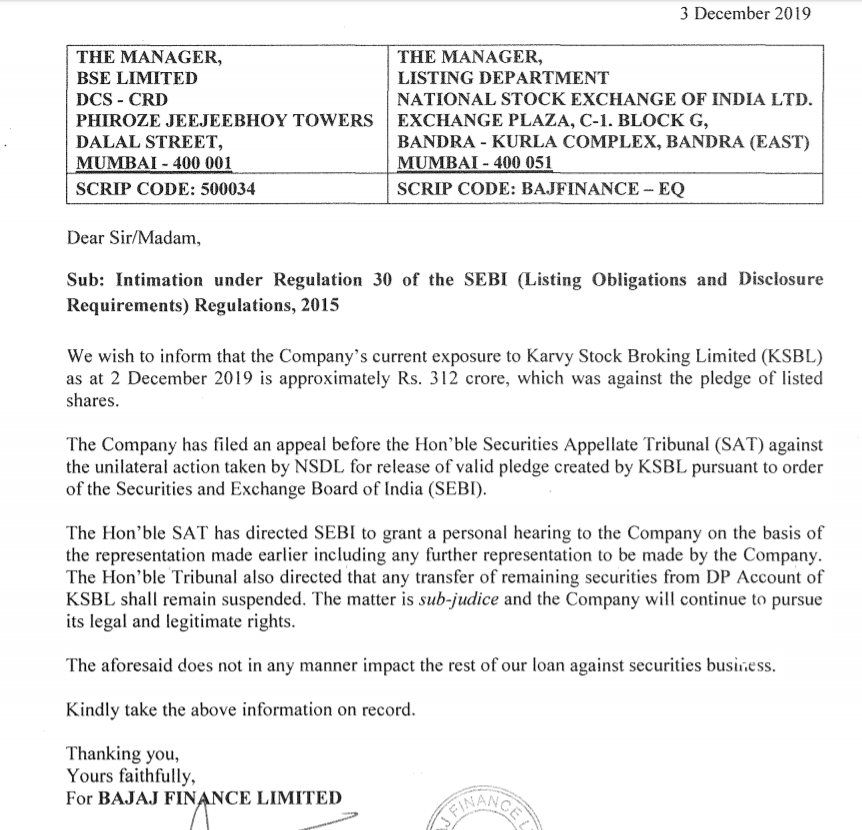

As per newspaper reports, Bajaj Fin exposure to Karvy is just 250cr.

Rgds

RR

1 Like

Can you please share the source of this? According to LiveMint the exposure is Rs 385 crores.

Exposure to Karvy and exposure to clients whose pledged shares were held with Karvy, are 2 very different things. From what I have understood so far, SEBI has directed Karvy to transfer pledged shares to it’s clients accounts. The problem is that these shares were pledged against funds borrowed from banks and NBFCs. So I am not really sure if this Rs 385 crores is a direct exposure to Karvy or to clients whose pledged shares were held with Karvy?

EDIT: These shares were fraudulently claimed to be its own by Karvy, when actually they beloned to its clients. Karvy illegally transferred these shares to its own demat account and then borrowed from banks/NBFCs by pledging these shares. NSDL transferred shares back to the clients demat accounts. So it seems like banks/NBFCs won’t be able to invoke pledges or get access to these shares.

3 Likes

It was in Business Standard.

This Rs 312 crore seems like a permanent loss, unless Karvy decides to repay it using its own money. Its unlikely that BFL or other banks will get access to these shares since they have already been transferred to the rightful owners’ accounts by NSDL.

How can SEBI just decide to take the shares from Bajaj Finance and hand over to Karvy clients. Ethically may be correct but its scary to imagine the repercussion. Just because the assets is in digital form means SEBI can transfer asset of bajaj finance to someone else without asking bajaj finance. If it is physical gold then was it even possible for SEBI to transfer it without asking entity under whose possession it is lying? The whole concept of loan against shares, or pledging of shares will go haywire.

1 Like

dude karvy was pledging your and my shares. that is illegal. for the sake of your investment in bajaj finance dont lose your moral compass

16 Likes

What Karvy did it is completely wrong and illegal but what SEBI was doing then when Karvy was illegally pledging client’s share? Why SEBI did not stopped them at that point of time ? Why there is no such monitoring system available in the system to check whether some institution is pledging someone else’s security ? What the role of market watchdog then ?

Due to sebi’s inefficiency why Bajaj Fin ,HDFC ,ICICI will suffer ?

As a Bajaj fin investor I don;t have any problem that if clients get back their securities ,But Along with Karvy SEBI should be also be held responsible for this . Let us see how higher court reacts …

dude karvy is taking a loan from bajaj finance and pledging client shares for the same.

before giving the loan was it not bajaj finance’s responsibility to do due diligence. Bajaj Finance, HDFC Bank have faulty processes. Whenever they screw up why blame regulator or Government

4 Likes

Dude let us know what is the correct process then ?

How could you know whether that share belongs to client or Karvy company when it is pledged to you for LAS from Karvy company’s own account ?

Sir it is always easier to blame/scapegoat the private companies because SEBI/Government can’t ever wrong . The consequences we are already watching on economy.

1 Like

Yes Right . Karvy lifted shares from demat accounts of it’s clients to it’s own demat acct & offered the same to HDFC/BFL as it’s own shares. Not only that , BFL/Banks sent pledge request to NSDL & they confirmed . Then why NSDL confirmed it in first place ?

Once pledging confirmed by NSDL ,and pledge is marked in KSBL DP . There’d be no reason for banks to doubt ownership. Thats why they issued the loan.

3 Likes