Deep pockets can’t have same effect in NBFC as startup like Flipkart. You have to ensure the money lent is returned. Else you will end up disbursing 10 billion $ in a year and 20% NPA. Even players with experience of years can struggle a lot. I’ll give two examples.

Bandhan Bank had decade of experience in MFI. They became bank and first corporate lending they did was ILFS.

Motilal Oswal had decades of experience in financial markets. One of the promoters Ramdev is renowned investor too. Still Aspire housing finance just grew loan book and didn’t pay much attention to risk. Today Aspire is saddled with 15% NPA and more is coming.

Of all the startup disruptions in world, nobody has cracked and proven record in Banking. Payments have been disrupted. Even asset management is disrupted by likes of Alipay and Robo advisories. Banking is tougher nut to crack and a disruptor has to stay afloat for few years to prove anything (there are few startup tech-only banks in UK and Europe who are successful so far. But they have years to prove it).

My first AC loan was with HDB Financial & second AC loan was with Bajaj Finance. As a busy individual i could not find any difference between the two or why i should choose Bajaj over HDB.

What could be the reason that reputed NBFC like Bajaj Finance, Sundaram finance and Chola are not applying for banking license inspite of access to lower cost CASA ? Am i missing something ?

Last time they applied it got rejected in 2014 only bandhan and idfc got approval

Bajaj, edelweiss, IBHF, LIC HF, JM fin, Shriram etc among the list that got rejected

Bajaj Finance had said in the past that they are not interested in Banking License because of the ownership % concerns. They don’t want to reduce promoter stake to a level RBI is comfortable with…

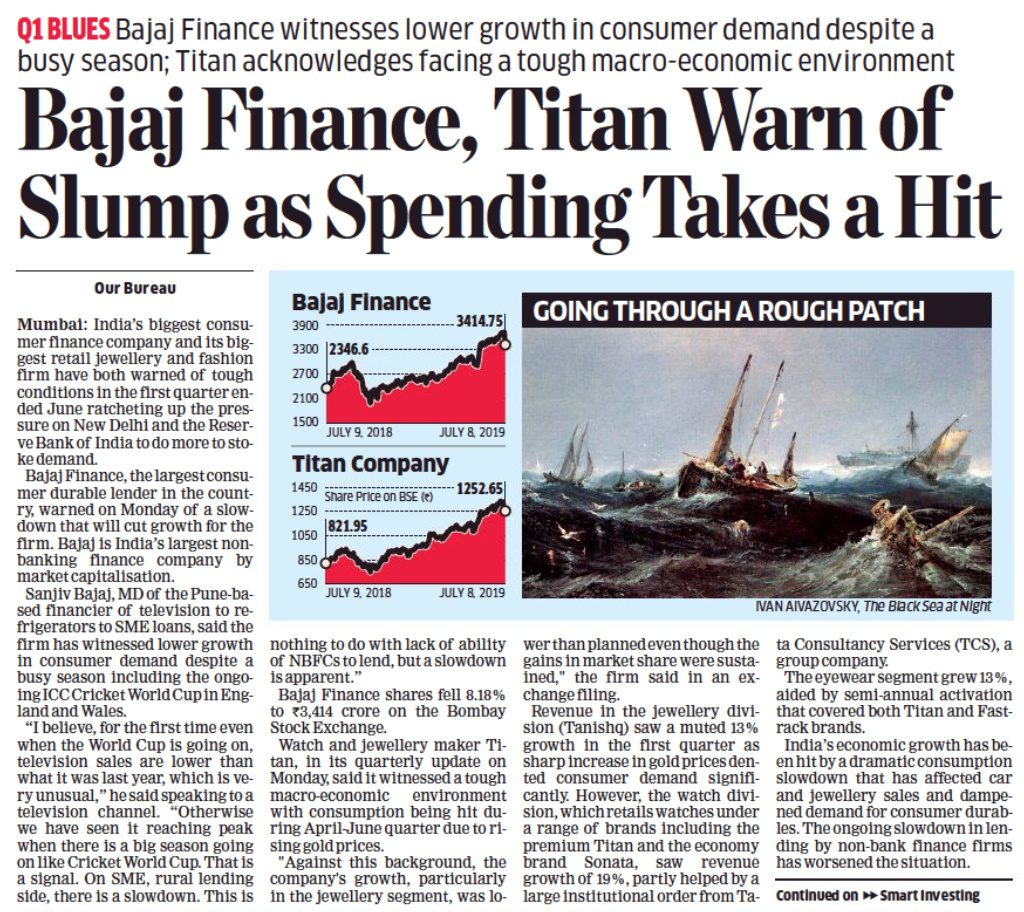

Yesterday Sanjeev Bajaj on CNBC said that the slowdown in the economy will reflect in the numbers of Bajaj Finance. He specifically mentioned consumer, sme and rural as areas which were affected the most. I don’t know how you can call a 41% growth in AUM as slowdown, maybe the slowdown in consumer, sme and rural was offset by growth in other areas like mortgage

Yes its in response to yesterday sanjiv bajaj interview where he was talking about general consumption slowdown but media took it as slowdown in his company and hence today’s response. Follow his latest tweet if you want to know more

I was going through AR of Bajaj Finance Ltd (BFL) - as per it

BFL was the largest financier of Bajaj Auto motorcycles and three-wheelers in FY2019.

BFL crossed a milestone of financing 1 million number of motorcycles in FY2019.

Gross deployments in FY2019 were H 8,271 crore — a growth of 55% over the previous year.

Financed over 40% of Bajaj motorcycles and some 36% of Bajaj three-wheelers in FY2019.

TRIO - Bajaj Finance Ltd, Bjaja Finserv (Insurance) and Bajaj Auto - all three business are synergistic for each others growth. E.g. Bajaj Auto grows due to easy financing option from Bajaj Finance and Bajaj Finance grows due to growth of Bajaj Auto. Bajaj finser Insuranc business grows due to network effect of Bajaj finannce’s registered members. Lot of cross selling oppotunity within group …e.g. for consumer durable loan bajaj finance provide insurance option from bajaj finserve.

This is an excellent model of business i see and considering opportunity size in india, it has excellent future ahead.

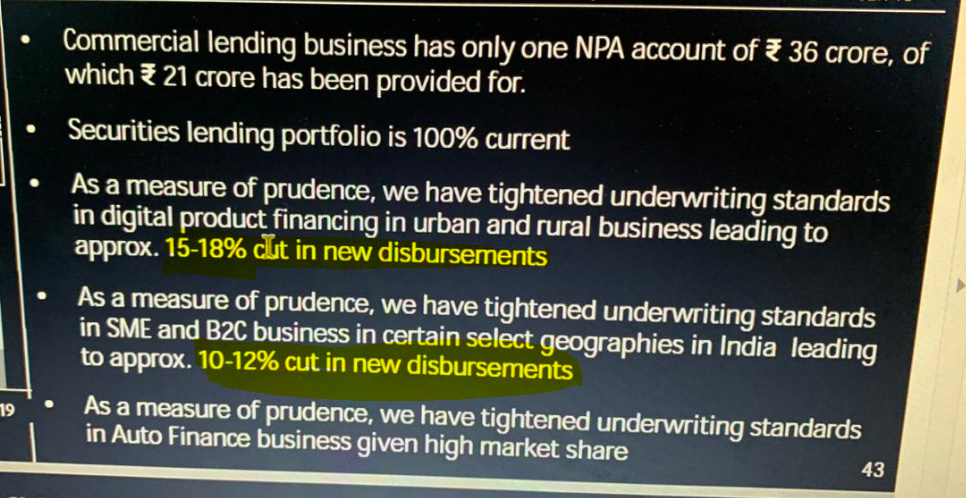

However, in bad time all three could impacted due to domino effect also. e.g. in auto slowdown, bajaj finance and bajaj finserv (insurance) could affect negatively.This might be reason for 1Q2020 - weak/muted outlook given by Bajaj finance ltd

Auto Finance is only 8% of the AUM… So slowdown there will not affect bajaj finance…

I also dont think outlook was weak. They are just more cautious and that is good sign in tough times… You dont want to keep growing at the cost of higher NPAs…

But I agree with you fully… All 3 companies have lot of synergies…

DISC… Bajfinance is the largest holding of my portfolio