Q3 Results - https://www.bseindia.com/xml-data/corpfiling/AttachLive/d1c3b810-3f8a-4818-b8e7-fc76816560ba.pdf

Splendid result in such a difficult environment for NBFCs. Reiterates the strength and market leadership of BFIN. Prudent step of the management by providing for the bad loans and containing them now itself rather than wait and watch. All in all, a happy outcome.

Another set of impressive numbers by BFL. It is a gift that keeps on giving!

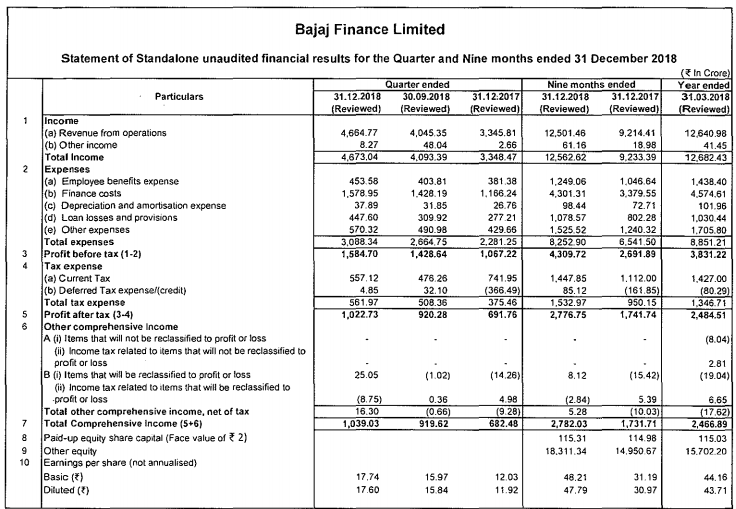

OPEX to NIM at 34.9% in Q3FY19 against 38.9% in Q3FY18. This ratio continues to fall.

@Sandeepg Can you explain this? How did you infer this from the quarterly earnings release?

Loan losses and provisions for the quarter at Rs 447.6 crore increased sharply by 44 percent sequentially and 61 percent year-on-year.

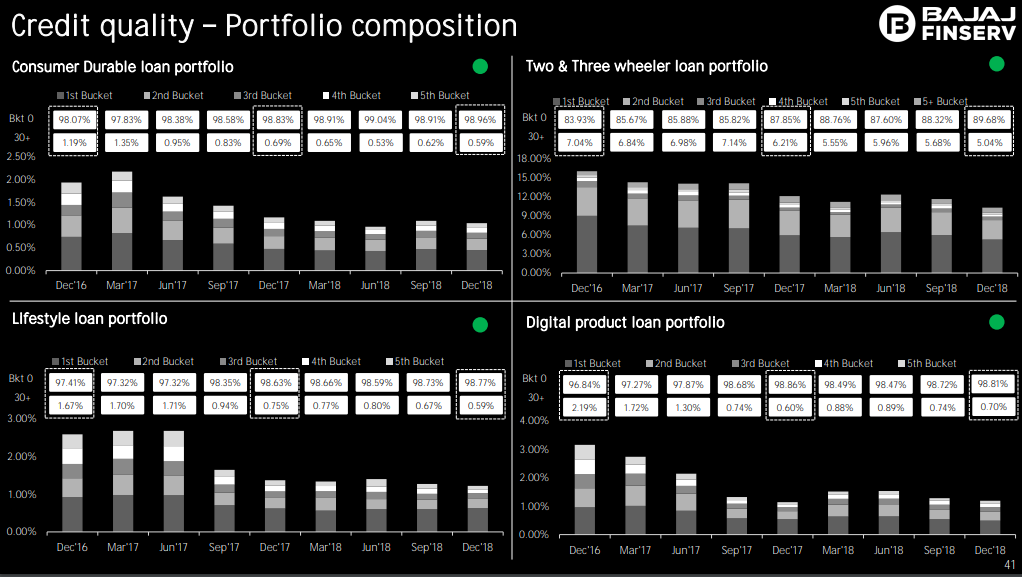

Asset quality deteriorated for the quarter ended December 2018. Gross non-performing assets (NPA) as a percentage of gross advances were higher at 1.55 percent against 1.49 percent in previous quarter. Net NPA, too, were higher at 0.62 percent in Q3 against 0.53 percent in Q2FY19.

Total slippages at the end of December quarter stood at Rs 715 crore, increased by 48 percent compared to Rs 483 crore at the end of September 2018.

Still BF has delivered impressive result which would have increased the market share as well. Very important to do this amidst the rising competition from companies making inroads into this space such as Capital first etc.

Hi guys

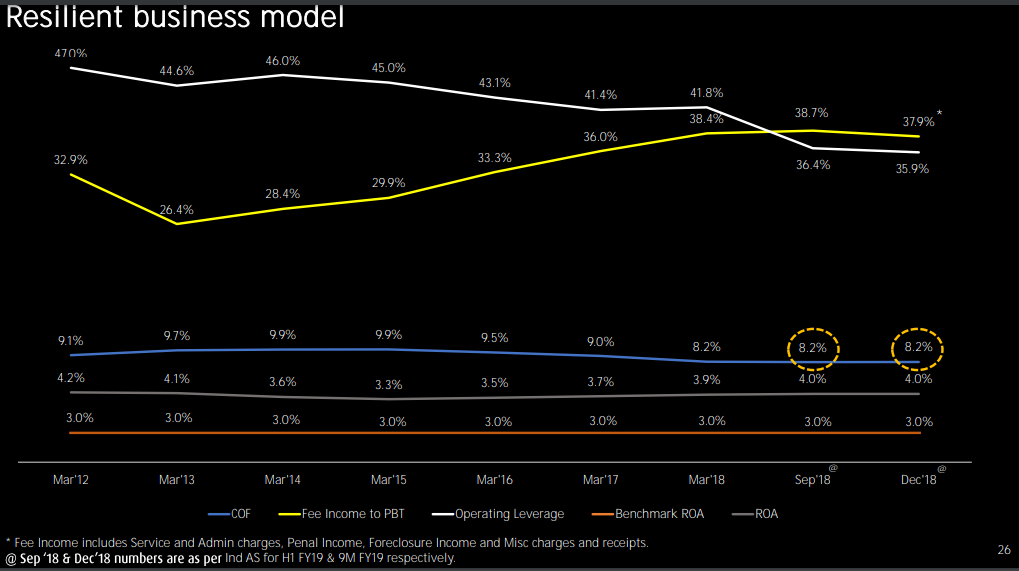

As usual strong results from BajFin. I was inquisitive to know how the cost of funds fared given the September onwards ‘liquidity crisis’ and it seems they fared well on COF. In the last two quarter’s presentation they have given the below graph.

Another key point which came 10 days or so ago was a new set of regulations to ECB allowing upto $750 Mn borrowings per FY. This quarter’s presentation calls this out too.

New External Commercial Borrowing (ECB) guidelines dated 16 Jan 2019, issued by RBI, now makes BFL eligible to raise funds in foreign currency through ECB. This would help us diversify our liability profile further.

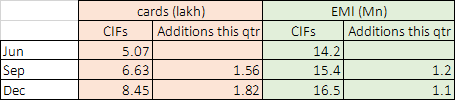

I was also interested to see the RBL co branded cards and EMI cards. They have the target of having 10L cards in force by FY end or April. It seems they will easily achieve this target. On the EMI card side in Q3 they had added fewer cards (0.1Mn less than Q2).

RBI circular for reference on ECB which came out last to last week.

I am having a major issue figuring the colours each quarter in charts such as the one below. Planning to write to the company ![]()

Rgds

Thanks for sharing. I would read the colours in the order of the key.

Gross NPA has increased due to higher provision but any thought why the net NPA has increased ?

GNPA increases due to bad loans. While NPA increases due to less provisions.

See NNPA = GNPA - Provisions

So…??

Overall the figures are very small as a percentage of total assets…

Provision coverage ratio @ 60% is very decent. It should not be a problem for BajFinance going forward.

I would worry in case the PCR slips below 50-55% which will indicate inadequate provisions and thereby excessive profits.

Disc: Invested.

Listen to Rajeev Jain of Bajaj finance. Key takeaways

- Cost of funds more or less same.

- Opex leverage kicking in ie top line getting converted into bottom line at a higher rate.

- He acknowledges that they have gained market share after q2 and is being modest that they are on their way to gain market share after the recent liquidity crisis.

- What encouraging is that he is confident of raising the balance sheet guidance for next year considerably. All this by a management which has under promised and over delivered .

PS… Invested from sub 700 levels

Will add on dips and price arnd 2200

Regards

Divyansh

This is one of the best run businesses and one of the most reasonable managements. Such humility in the interview. And they have such handle on their business. The good thing is there is no ambiguity, they know their stuff.

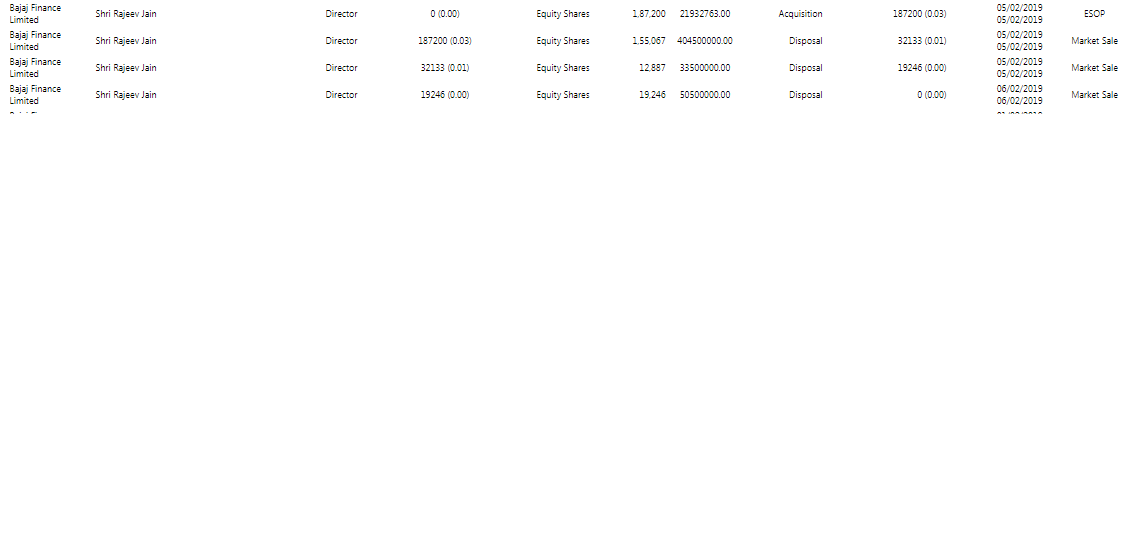

He’s been doing it for 5-6 yrs…like clockwork…selling all his ESOPs on grant. So quite possible that he thinks of leaving every year

Rgds

RR

Or it may have been mandate by the company (or maybe an individual) that CEO should sell all his ESOPs on grant so that he has no holding in the company for them to declare by March 31st.

I wouldn’t be worried if he is doing it every year… If he is doing it for the first time, then its a BIG concern!!

Disclosure : invested. Less than 2% of my PF

Rajeev Jain is probably one of the Best CEO Indian corporate have seen in recent past -he has been a visionary and have a high degree of integrity/honesty which is why he doesnt want to get influenced by share price ,which is why he keeps selling the shares when it gets vested and he puts into FD

Honestly I didn’t know what to make of it that is why I put it out here to see if people have views either way. Looks like he has been doing this consistently so there is nothing to worry about show goes on.

Here is a good article on the stress in the real estate sector. Relevant as BHFL does some form of developer financing. Although I remember that in one of the calls the management had mentioned that this segment forms a very low percentage of their overall loan book.

This link was first posted on another thread - Great Articles to read on the web.