Thank you for sharing valuable information.

Regards,

Salil

Thank you for sharing valuable information.

Regards,

Salil

As I have pointed out earlier in this thread, the moat of this company is increasingly getting stronger with each passing day. Dare I say, it is becoming impregnable now. The closest competitor to this company in it key segments till last year was Capital First. However, with the integration with IDFC Bank, Mr. Vaidyanathan has his hands full now, thus allowing Bajaj Finance to have a free run and keep increasing its market share. Frankly speaking, I don’t see any credible competitor to Bajaj Finance for at least 3 more years.

With all this noise about FinTech and its growing clout ,my humble submission is that Bajaj Finance is the ultimate FinTech entity. They were one of the earliest adopters of Fintech in the Industry and they are riding the entire wave very profitably. It is mind boggling to see a NBFC post 80% PAT Growth on such a large base and all the investments done over the last couple of years will ensure that this growth rate is sustainable over the next 3 years.

There were a lot of skeptics in this forum when the share price had slipped to 1600 during November last year and the skeptics in this counter will never vanish. But, I suggest that we should not miss the woods for the trees. This is a very very special company being created and is the ultimate play on the consumption boom in India. Can this company command a market cap of 10 Lac Crores in the next 3-5 years? I for one won’t be betting against it.

Q1 Concall summary (source: capital market):

The company has posted one of the strongest start of first quarter in the last few years. The businesses have continued to focus on granularity of the portfolio across product and geographies to reduce risk and augment profitability. It reflected in better margin, lower costs and better risk metrics in Q1FY19. The loan book of the company has surged 35% end June 2018 over June 2017.

Bajaj Housing Finance has become fully operational from February 2018. BHFL is progressing well and the company is confident that business will deliver high growth along with threshold ROEs.

The company has expanded its presence in the current quarter and is now present in 1,486 locations. It added 150 locations in Q1FY219, while expects geographic expansion to continue at 15%-20% annualized growth rate.

The Opex to NIM came is very strong aided by stronger fee momentum and better cost management. The company has guided at opex to NII of 40% for FY2019.

The company continued to manage its ALM well with a judicious mix of borrowings between banks, money markets and deposits. Liquidity and interest rates have hardened over last 90 days, while the company is well covered on ALM to manage any impact on P&L over short to medium term period.

Portfolio quality remained at its record best in Q1 FY19. With strong portfolio quality, the company is well placed to grow its business rapidly.

Company continues to expand user adoption of its Bajaj Finserv Mobikwik wallet to increase engagement with customers and increase repeat purchase rate. Bajaj Finserv Mobikwik wallet has 2.2 million active wallet users as of 30 June 2018, with their EMI card linked to the wallet.

The board of directors has approved purchase of 100% stake of Bajaj Financial Securities (BFINSEC), a 100% subsidiary of Bajaj Housing Finance and an indirect 100% subsidiary of Bajaj Finance. The strategy is to offer full product suite (demat & broking) to Loan against securities clients and grow profit pool of LAS business.

Total Slippages for the quarter were Rs 379 crore in Q1FY2019. The consolidated gross NPA and net NPA stood at 1.39% and 0.37% respectively end June 2018.

I also attended the AGM. It was my first AGM ever and a very good experience. Excellent summaries have been posted by @mukesh_gt and @basumallick. Adding my inputs:

Ecommerce transactions can only be done by existing EMI card holders. BFL has 15 million card holders in total. Because of this value proposition Amazon and Flipkart like to deal with BFL. Flipkart has started (or announced plan to start) its own NBFC. The MD declined to comment on this. Since I come from a corporate banking background, I know that giving loans is easy. Getting the interest and principal back is a different game and this is where prudent risk management comes in. With its own NBFC, Flipkart may find it easy to get customers but maintaining low NPAs and getting the right customers is a different ball game. That is where good NBFCs hold advantage.

About 508,000 cards in circulation now, will hit the 1 million mark by March 2019. BFL will be among the top 5 credit card issuers by that time.

BFL has gone from 0% to 12% in 5 years, in terms of the share of deposits (retail + corporate) to their total liabilities. Will end FY19 at 18%. These deposits are less volatile and give BFL more predictability in terms of tenure and cost of funds. As a benchmark - HDFC has 34% retail deposit share of their liabilities. Earlier the strategy was to borrow wholesale and lend retail. Going forward the strategy will be to borrow retail and lend wholesale (SMEs).

The MD mentioned that mortgages and commercial lending growth will be higher than in previous quarters. Good SMEs are going away from PSU banks, which are being ultra conservative now due to the NPA crisis. This is an advantage for BFL.

The MD mentioned that its still early to judge the investment in Mobikwik. The investment will help them digitise their EMI cards, which is a saving of Rs 70-100 per card (printing & shipping charges). Also this enables the EMI card holders to do more with BFL at the PoS (points of sale). As mentioned in the presentation, 73% of the loans come from existing customers. This is unprecedented and unheard of in other NBFCs. As @maverickroger mentioned the moat of this company is growing stronger by the day. Digital EMI cards will further be an enabler to this trend!

The MD also mentioned something about digital card strategy working wonderfully for some companies in China. However it was unclear to me. If fellow members have more clarity on this then please elaborate.

someone I know got a whopping Rs 1.8 lakh loan from BFL for a medical procedure. Minimum documentation. This person was an existing customer, but she was told by the executive that the applicant will be treated as a new customer since the loan is much bigger. processing done in two days. minimum documentation. what if the borrower does not pay back?

wonder how many defaults happen in this business.

disclosure:holding

Let me share my experience…

I have availed close to 8lacs loan recently with BFL… I am salaried and get take home close to 1lac pm…The loan category is flexi loan… With rate of interest 14.2%…

To my surprise no one providing this category of loan… Had checked with Hdfc and Kotak… Where I am existing customer and executive of these banks said there is no facility like this availble with them(.its there buts it’s just on credit card for 50to 60k approx)…

While taking loan they tried to sold me lots of other things like insurance and higher rate of interest 15% and other charges … Since my credit profile is great I didn’t acepect this… and finally got loan for 14.2% and charges comparable to others…Though these terms itself are high… In case of bad profile Iam sure customer had to accept all of their terms…

Bottom line is these people are so so smart than all the traditional players while selling products …compare to …great lenders like Hdfc and kotaks they could fetch much charge higher interest rates… Processing fees and other charges… Thats why higher margins and net profit…

However, any 2008 kind of situation… Iam really have doubts about their survival… They may get into situations like how Axis and ICICI got into interms of NPA …till then I am sure it’s free run for these guys…

The salaried class does not default (generally) unless they lose their jobs. Only a crisis which leads to large scale job losses can affect BFL. If there are large scale job losses in the economy then there will be no places to hide corporate lenders who are performing poorly with a GDP growth of 7% will fare even worse. Even during the 2008 crisis how many people actually lost jobs in India? Sure the valuation can take a beating but the underlying business won’t be as severely affected

‘What if the borrower does not pay back?’ Well I think you are questioning the entire banking industry, not just BFL. Some of the borrowers do not pay back. That is truth. As long as the non repaying borrowers are a tiny fraction, then it is Ok. You don’t have to wonder about the defaults, banks and NBFCs are required to declare their non-performing loans and also provision for them regularly. BFL has net NPAs of 0.38% (Net NPA = Gross NPA -Provisions). I think this post will help you - How to analyze NBFC companies?

BFL gets 73% of loans frm existing customers. This is infact some kind of concern for me. Obviously the same customer will not keep borrowing quarter after quarter. So real growth should come from new customers and not existing. Views invited

Its cross-selling and that is their biggest pitch…

Like one person has taken a consumer durable loan, next they pitch for same customer personal loan then home loan etc etc…

Its always better to keep the existing customer, as you will give another loan if he/she is paying back his/her previous loan.

They have invested good amount of money in data analytics and they are using existing customer data to fullest … Its one of the best stocks in Indian market growing very fast & proxy to Indian consumption story (They are providing loans now on even Groccery as well :))

why the rate of interest is so high? every bank provides at 11 to 12% for personal loans and what is the rationale for you to go with BFL?

I think one should be cautious about bajaj finance at these valuations in case evaluating fresh investments regardless of how bullish one is about prospects. At 9 times book value - it is more than well valued plus its a well discovered and followed business. We have seen how great businesses if they come down a notch and become good - the effect on valuations is violent cuts. There is a substantial valuation risk to bajaj finance even for those who have purchased it at much lower levels. Just my views. Bajaj finance was available at 2 times book a few years ago leading to a rerating. It has consistently delivered an ROE of 20-21% and will probably continue to do the same in the future.

It is an overdraft facility which other banks dont provide. You can use only what you require and pay back whenever you have extra cash and then withdraw again, its like a bank’s savings account. Interest is calculated based on the outstanding amount on a daily basis. All the customers will not utilize the limit of say 8 lakhs all the time, but BFL needs to have this amount ready in case the customer needs it thus resulting in some loss of interest. That is why the interest rate is higher. For normal personal loans interest rates are comparable with other banks

Roughly speaking in financials:

So till there is any question mark on growth or quality, this difference would remain, quantum can vary based on market sentiments/quarterly performance. In last 2 qtrs growth surpassed market expectations, and quantum increased.

Now it is more a question of individual’s portfolio risk management as to what allocation one would do to these high growth names vs others.

No prizes for guessing which co is being referred here.

source : - The Final Relaxo Lecture – Fundoo Professor

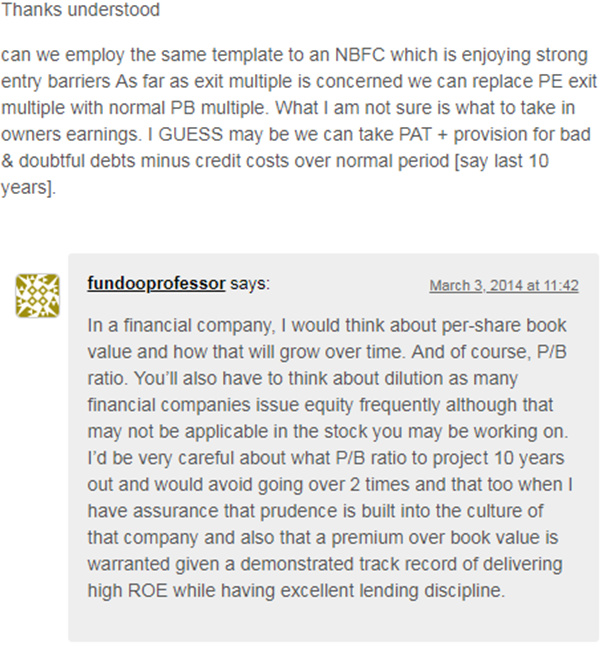

In case one hasn’t seen it already, the transcript on this link above is also a very informative read and provides a nice template to reflect on valuations.

Best

Bheeshma

Forget Bajaj Finance, loook at IndusInd/HDFC Bank… the above philosophy of not paying more than 2x book has been consistently trashed by market for last 8-10 years if not longer … who is wrong - above philosophy or the market for extended duration?

Markets are not made of AI bots and robots trading fair value. What humans perceive as fair value over long durations is fair enough to make money.

Hi @RamanTiwari / @poddy

Investors can pay the price they are comfortable with. I posted the above link because of the thought process which i felt was good. Different investors have different thought processes. In the above passage and in the transcript , prof urges fellow investors to think in terms of expected returns and exit multiples.

The fundoprof blog has some very good discussions esp the q&a at the end of the post. At the least its an interesting read.

Best

Bheeshma

In the Indian context I believe there is a serious dearth of quality companies to invest. If we had sufficient number of such companies the economic growth will be more and the employment will be better. The valuations of quality companies will be reasonable. But then this is what we have and we need to live with it. We expect these companies like Bajaj Finance and DMart to give 15-20% CAGR for 10 years. We will ride out any underperformance in between. Even if it only 12% we will get something at the end of the period.

We can’t say the same about a lot of other companies. In fact even Rakesh Jhunjhunwala says of the 6000 companies on the stock exchange 5500 are not worth looking into. I do not like these high valuations but then who am I to determine valuations?

Yes blog is a good source of learning and I have read it a lot and learnt from it.Prof I think doesn’t invest in financials, I have seen many other investors/fund managers refraining from financials for similar reason, or at least capping sector weight to lets say 30%.