It is available on BSE website under Disclosures → Insider Trading 2015.

Here is the link.

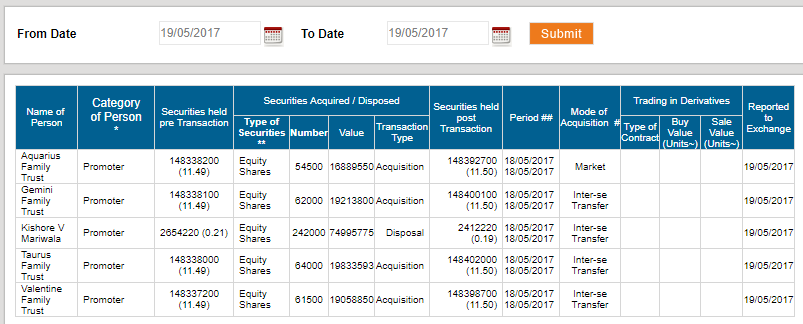

You can also get the same from NSE at this link. From there select Shareholding Structure → PIT Disclosures → Post 15-May-2015.

Do note that sometimes the quality of the data is suspect so you have to use your judgement to arrive at conclusions. Alternatively you can cross validate it on the other exchange. Here is an example which I saw recently under Marico.

@nil_71 thanks for sharing the info. The stock has corrected from 1900 odd levels to 1650. I have added to my position yesterday.

This is a wonderful business and I am invested in this for long term and hence expensive vs cheap doesn’t matter to me. Till they are growing at the same rate Bajaj finance will continue to be expensive. I know of people citing it as expensive and waiting on the sidelines since years expecting it to fall to pick it up.

BFIN CEO mentioned , this year they are expecting 30% PAT Growth. Now it is for market to decide. Also their Cost to Income ratio will be higher in next 2-3 Qtrs as they are investing in BFL2.0.

Promoter buying may make a case for undervaluation or add to the confidence to buy. On the other hand, as someone old enough to be incapable of shirking the burden of history, I feel it prudent to point out that there have been many instances of even brilliant promoters buying / selling at what in foresight seemed good and hindsight bad.

Ultimately no one, not even promoters can figure it all out.

I am thinking now, what can go wrong for BFIN as a company or Industry as a whole ? any Interest rate hike -I am fine. It will affect the industry as whole. They survived in pretty high interest regime.

NPA may spike but I have checked multiple reports and management is really finicky on NPA. They must have a tight control and eye on this. They were the 1st to flag the LAP Loan issue. Exited Infra financing also for the same reason

@diffsoft I feel it prudent to point out that there have been many instances of even brilliant promoters buying / selling at what in foresight seemed good and hindsight bad.

Yes, you are right. But when you know the person’s track record, following that is not at all wrong. So pick and chose whom you are following, rather than following every one. It is exactly like following one of the VP’s here, provided you have the conviction similar to theirs.

For a several years I have seen how people like Rahul Bajaj, Sanjiv Bajaj, Harsh Mariwala, Godrej Family, Sunil Duggal, Dabur Family, Ajay Piramal and Shriram Group have acted in an opportunistic way and the results if I had followed them would have been tremendously beneficial to myself. At the time when they buy, you have double mind to either follow or wait, thinking it is still expensive. But as the time passes buy, when you see outcomes, you get the conviction to act further.

So if you have not adopted to this technique, your mind will never agree with what you see. But you can revisit this subject down the line to judge the results. Very difficult to judge it now. Yes, there can be failures, because future can never be predicted by anyone.

We have various ways to skin the cat. And this is one among them. Not required to be followed by everyone.

Discl: Invested and added on this news, hence may be biased in my opinion.

I don’t know, but one may want to accommodate a margin of safety for the unknown. I had written earlier, just as some examples, in post no 229, on what could go wrong. It is of course not possible to foresee all that can go wrong. In any case the key point was that promoters can also get it wrong, so one may not let that be an big confidence builder.

Even if we concede promoters may not make business mistakes buying their stock when they are buying is moot was my point.

But, promoters do make mistakes and unfortunately we automatically pick survivors when, for a fit analysis, we should go back in time and pick those who were considered as good as the ones we consider today and see how they did.

Even then we can lay out some specific “mistakes in hindsight” of some of these promoters:

Rahul Bajaj - despite being the undisputed leader in scooters, missed the upcoming motorcycle boom, which was taken over by a then upstart - Hero. Bajaj Finance was ran aground with losses in the PC Leasing business, poor RoEs, which is unthinkable today, before new management took over.

Godrej Family - Geometric Software, partly owned by them struggled, before being sold to HCL group.

Ajay Piramal - DRG was the biggest acquisition of the group at ~ $ 635 million. This acquisition has produced paltry earnings in relation to the price paid.

Shriram Group - many group companies are struggling, Shriram Transport itself had a bad foray in construction finance, pulling down the core business substantially.

Am sure all made mistakes, just that we don’t know enough. And none can be guaranteed to be thriving in the distant future. As an aside, to just get a feel of the sweep of business vicissitudes, I would recommend Dr Tripathi’s Oxford History of Indian Business. Jagat Seth, for instance of the 18th century was far richer than the richest today and funded Govts and wars. I am not sure if people even know him today.

My point, to come back, is that what’s so clear in hindsight, what looks invincible today; cannot be guaranteed to be the same tomorrow. But I do agree bets must be taken on them today.

I agree with your view points. I am not buying now, rather we will wait for results to come in. As an Investor, we cannot be complacent. We need to have 2nd Order thinking working on it.

Pessimists make the most sense and sound very wise.

But in markets its the Optimistis who make money

I understand your point but its fair to say promoters always have the closest view of the business. And their buying is certainly a sign of supreme confidence. Bajaj Finance has a good growth ahead I believe. Strong management confident of its business putti g their money where their mouth is. I will be a buyer.

That’s true, I liked your point. In stock market most of the times all you have to do is gauge perception of the lay investors. As a general rule buying your own company shares is perceived as a healthy sign though it may not be the best thing to do for a promoter. We intend to correlate our conviction with that of promoters. Most of the times I wonder why promoters buy their own shares, may be they are as clueless wondering what to buy from the market. May be feeling that when all other stocks are doing so well his own company share price looks so undervalued. Either way you tend to gain if not by promoters conviction than by market’s perception.

We may be naturally tempted to think that they are buying only because of undervaluation. But that is not wholly true, and there are many reasons, besides just that

If the amount is a trivial addition (relative to their portfolio) then could well be a signalling mechanism, because they know many think promoter buying is a positive indicator, price may go up and interested parties can sell, including the company wanting to issue fresh shares.

There could be an internal promoter commitment or understanding that we are not privy to. For instance someone in the promoter group hints at selling at some time, and timing is not controlled, so you may want to proetct overall promoter shareholding. Maybe there are multuple group companies (listed and unlisted), and there could be an understanding that he will buy here and sell there.

Maybe the promoter just does not know any other company well enough, because he is not looking at the market like we do; it’s not his job and he isn’t confident. He is very optimistic about the prospects of his company (and as one can well imagine, overoptimistic). Maybe he just got a lot of cash from another transaction just feels that his company is the best he knows, and here returns don’t matter and there is signalling as well.

There could be many other reasons, and hence one should exercise prudence in assuming that promoter buying is due to relative undervaluation.

Is the rising bond yields dent nbfc margins? as the cost of borrowing would increase? can someone through light on this?how would in particular effect bajaj fin? i know its consolidating a bit given the expensive valuations?

Bajaj Finance will be impacted less than other NBFCs in my opinion. They have started taking deposits from retail, so are not only dependent on the banks for wholesale borrowing. Their assets are mostly of short duration so they would have some leeway of passing on higher rates more quickly for new loans generated.

I am checking the EPS for Bajaj Finance. It has increased from 28.68 in 2014 to 41.9 currently.

The PE re-rating happened big time from 6 in 2014 to 38 in 2018.

P/B value is 8 times. how can i value this company?