Hi All

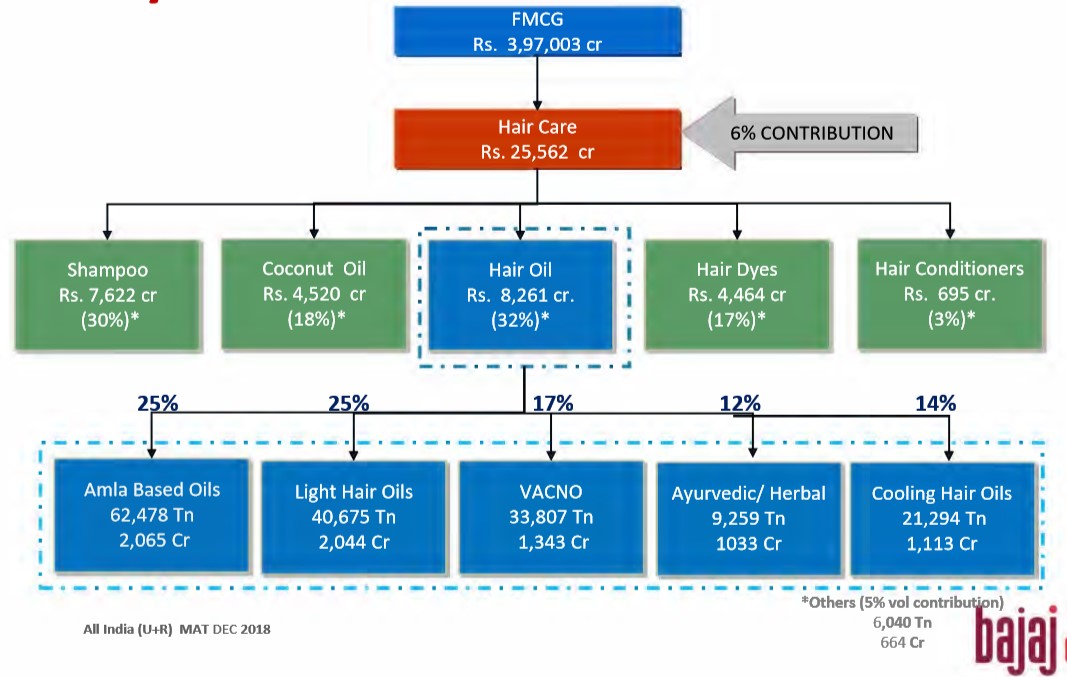

the sector break up given by the company is quite helpful -

I find it difficult to determine – what is the total addressable market for Bajaj Consumer – is it Coconut Oil + Other Hair Oil (12,781 Crores, 1.8bn USD), only Non Coconut Hair Oil (8,261 Crores, 1.16bn USD) or only Light Hair Oil (2,044 Crores, 288mn USD)? This assumes significance when one looks at the market shares below –

| Total Oil |

MS % |

Non Coconut Oil |

MS % |

Light Hair Oil |

MS % |

| Marico |

46% |

Marico |

17% |

Bajaj |

60% |

| Bajaj |

10% |

Bajaj |

15% |

Others |

40% |

| Dabur |

8% |

Dabur |

12% |

Total |

100% |

| Emami |

7% |

Emami |

11% |

|

|

| Shalimar |

3% |

Shalimar |

4% |

|

|

| Total |

74% |

Total |

58% |

|

|

The thought behind figuring out addressable market was to understand if Bajaj Cons had scale advantages in the entire hair oil market or is it merely big in a small category? With such high levels of concentration in the overall market and a distinct differentiation by consumers for non-coconut oils (due to non-stickiness and other benefits), Bajaj Consumer can employ economies of scale even when the category it competes in is classified as Non Coconut hair oil.

Despite its premium pricing, Bajaj Consumer has increased its market share continuously as can be seen from below –

| Particulars |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

| Value Share |

7.7% |

8.5% |

9.5% |

9.9% |

9.7% |

9.7% |

9.8% |

9.5% |

9.6% |

| Volume Share |

4.7% |

5.8% |

6.6% |

6.7% |

7.1% |

7.4% |

7.3% |

7.3% |

7.8% |

| 100ml Price |

50 |

|

55 |

|

60 |

60 |

60 |

60 |

65 |

2 main negatives for me are -

#1 – Pledging of Shares and Sale by promoters – In order to raise financing for its power company Lalitput Power Generation Company Ltd, in a liquidity crunch due to non payment by state discoms, promoters have pledged a large part of their shareholding - 61%, up from 26% in FY 2015. Further highlighting liquidity constraint, promoters also sold 7% stake in the company in FY19, and their holding presently stands at 60%. At a recent investor meeting in May 2019, the promoters have commented that power project issues are easing and no more promoter selling is envisaged. Resembles sale of family gold to save the copper.

#2 – Low Audit Fees – For a 4,000 crore (560mn USD) m-cap, its quite surprising that the audit fees charged are merely 10 lakhs (14k USD), and the audit firm is a sole proprietorship in Bombay. With such low compensation and size of the firm, even stock audits all over India in various depots might be difficult. With 265 crores (37mn USD) lying in company’s accounts, a weak external oversight is worrisome.

You can read my entire thesis on the company here -

Disc. - Invested.

hope this helps!