I agree with you and I would further like to mention that their almond oil (the “pony”) has a majority of mineral oil. This was not a problem a while ago but now that there is such an abundance of information availability, customers are turning away from harmful products. I think this is like a slow poison for BCC

1 Like

Sorry for the late reply , i lost access to my a/c due to some password issue and it took me almost 3 to 4 days to regain access again …weird !

i didnt know about the mineral oil part …will have to be careful then as its not a good thing to have but where have you come across this news item or information …if you dont mind can u share or its your own reading based on ingredients you observed as i have not really looked at it that closely ?

This is a known fact - its even on the label!

IMG_2650|375x500

This shouldn’t impact investment thesis as even competitors in the -Cool/non Chipku category use the same. Fact is - Its a high ROE product and people buy it.

For personal use - I wouldn’t buy it ![]()

Point to ponder, What’s the health benefits of eating biscuits or drinking coke?

2 Likes

Yes I agree that people do buy the product. However, my point is that there is a trend towards “good for you” products. We will not be able to justify unhealthy or harmful products for long as there is so much negative feedback on the internet.

Why do you think diet coke is doing as good if not better that regular coke. It is only a matter of time that people drift away from bad products. Especially if you have to apply them on your body parts. I really think that a task for the new CEO will be to remove the amount of crude oil/ mineral oil content of the product. And i think this might make the a lower ROE product (However, this is just an opinion but please read about the concept of “creative destruction” to know what I am talking about)

1 Like

If paywalled… Take a free trial

2 Likes

Found this article, interestingly it talks about -

“Rural markets have been far less impacted than the urban markets, and as most containment zones are in the urban centers.”

Disc: Invested in Satellite portfolio.

1 Like

This is interesting move by Bajaj Consumer :

Not sure, how this would pan out.

Disc : Invested in both Bajaj Consumer & IndiaMart.

Interesting thread -

My Notes on Q2FY21 Earning Call Minutes :

- Flattish Employee Cost

- Sanitizer was a tactical bet now its a crowded market and we are not planning to spend more on that as we are not going to make much money on it

- Retail demand is still struggling , wholesale has come back substantially in Sep more than Aug …and e are hoping Q3 will be much better.

-2 or 3 months before lockdown the consumer preference was towards larger Pack SKUs

-In the last 2 or 3 months --smaller SKUs are in great demand.

-No marks has continued to decline , in the last 2 or 3 Qs ADHO has shown good traction , 2% growth at this stage and secondary of ADHO is at 5% , Amala has also grown.

-Sanitizer + Amala is 5% of sales and within it , Sanitizer is less.

-Distributor days ( Non-sanitizer ) end of June : 30 days , end of Sep :30 days

-Ad Spend + Sales promotion is around 8% --spending on digital --absolute Ad spend is similar ( included Van spend ) - Urban growth is lower than rural growth but Urban is increasing, till Aug we were quite Rural focussed hence we have performed well comparativley , now our focus has shifted to Urban since Sep.

- Raw Material ( LLP ) Prices have gone up from (50.79) to 52 currently in oct & RMO has also gone up ( 108 )

- Not looking to increase the prices given the mkt demand , will focus on overhead rationalisation to protect our Margins , 1/3 of cost is raw material that has 1/3rd imapct on Gross Margins are concerned , every 3% increase on raw material has 1% impact on EBITDA Margins.

- Consumer is looking for Higher ML per Rs and not looking for smaller packs ,its value for money.

- 20Rs is the highest growing SKU

- ADHO market share we are focusing on to increase along with other products in Portfolio as well as we already have 60% Market share of ADHO so its difficult to grow substantially

- We see Urban coming back in growth to close to Normal,now we have started focusssing on Urban as we were taking advantage of Rural as a tactical opportunity in the past 3 to 4 months & we will show good results in coming Qs.

- Uptown Investment is there we are getting our licences etc but due to Covid , we are not focussing on it @ Status Quo.

- Board will decide on Dividends as this was an aberation year, we have put lot of feedback received to the Board and they will decide on Dividend distribution policy , nothing to worry about .

- Ad spend ( with sales promotion ) will not be compromised, we will look at all other cost but Ad spend if you compromise it has large long term impact hence that is something we will not compromise on it remains at 18%, it might even go up going forward basis Topline growth.

- We will continue to ensure that our EBITDA continue to grow , not as a % but in Absolute terms-- clear focus on it.

- ADHO will remain our absolute focus, we are moving away from Light hair oil to Hair oil and Amala will be a focus as well.

- M&A within India Valuation looks too high and outside we will focus in Pockets but probably from next Year

- Modern trade -Metro cities not done well, largest chains ( Future group ) had liquidity issue where we had largest exposure, we hope in Q3,Q4

- Whole-sale in the Q2 was Flat, Wholesale is coming back ( 48% Urban, 52% Rural )

- International mkt is not our focus this Year, UAE , Bangladesh , Nepal

- Volume growth is same as value growth @5%

- Southern mkt is more coconut market and our main Product Badam Almond( ADHO ) doesnt have that traction in the Southern Mkt

- Our rural drive we are looking at south now , lets see how this market pans out.

- Sales in H1 CSD no.s are flat, we will monitor our a/cs much better, CSD will not go away – we will do some more work from our end.

- No Marks has declined 30% and revenues not very substantial, this is a bit confidential but we are looking at maintaining this brand and looking at the lower price or some strategy around it.

- contribution of new SKUs - 300ml , 500ml of Amala came into being ( Aug / sep ), 35ml (Rs.20) pack came into being -No.s at this stage are Marginal.

- ADHO gross Margins remain between 60 to 62% to right upto 72% --avg of 65%

Disclaimer : Not invested , only tracking --and these may not be all the notes from the conference call., only whatever i could note down.

The link is here : https://youtu.be/y6TTRCcQ7wg

2 Likes

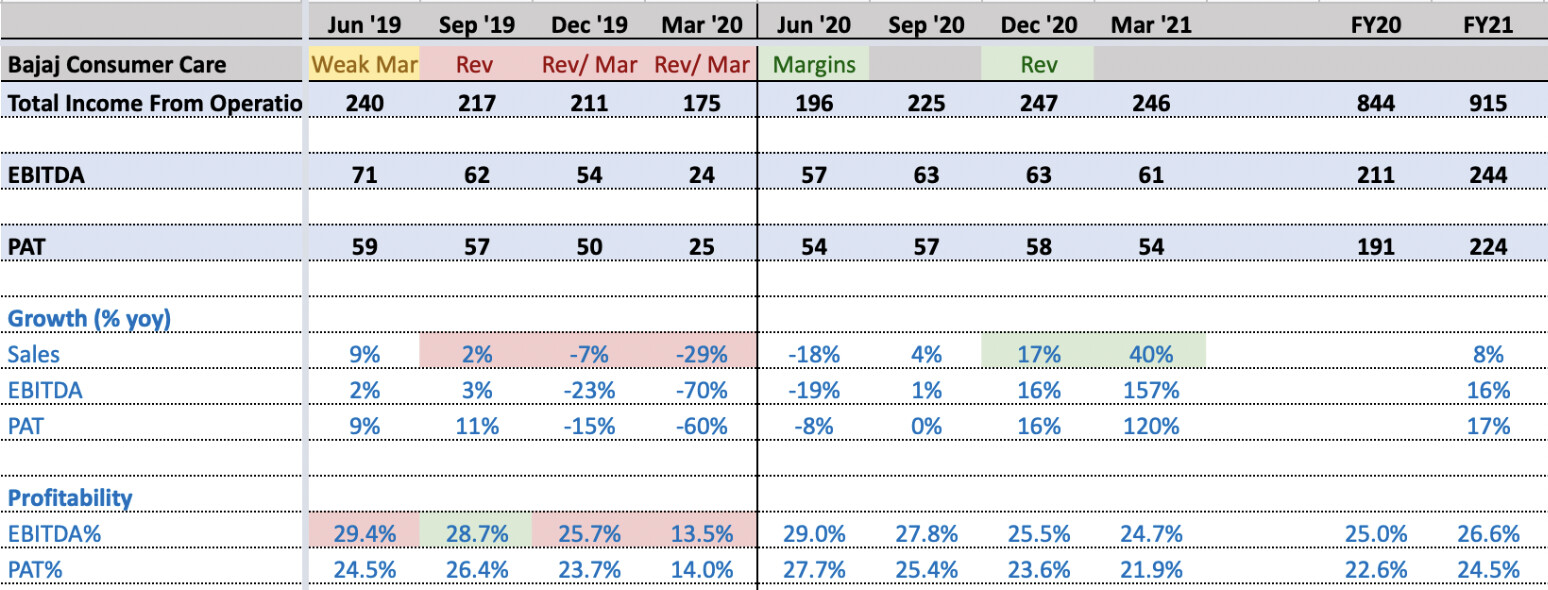

Bajaj Consumer Q4FY21 Result – Below Expectations

Negatives

- Revenues: 2-year CAGR flat … 40% yoy (off a low base)

- Gross Margins: -700 bps to 61.3% (lowest in 7 quarters) …. RM inflation, higher Amla share, provision for sanitiser inventory

Outlook

- Margins: aim to remain within the 25-28% band …. 2.5% price increase in Feb-Mar to partly mitigate RM pressure

- Hair Oil Industry: growth has revived, though revenues lagging vol due to downtrading

3 Likes

*Bajaj Consumer – Q4FY21 Concall Update

• Q4 was a robust quarter with positivity around the overall economy as higher rollouts of vaccinations are witnessed. Rural continued its growth momentum whereas urban started showing recovery. However, increase in commodity prices are putting pressure on margins across industries

• Raw material inflation impacted the gross margins during the quarter. In addition, the product mix and provision for non-moving products like sanitizers, had an impact on profitability.

• The company has taken price increases in the month of Feb and March to the tune of 2.5%, to partially cover the raw material inflation. The management believes that the higher raw material prices are likely to continue in Q1 as well which might affect the margins. The company might look for more price hikes, if need arises

• Urban is showing signs of recovery clocking a growth of 23% in Q4 after witnessing a 7% growth in Q3. However, last year’s base was lower

• Rural markets continue to be robust with a growth of 61% in Q4, supported by strong van sales operations

• Q4 saw continued recovery of Modern trade business with good traction during Republic day and Holi festival

• Hair oil market continued to stabilize in Jan-Feb’21, with value growth at 1% and volume growth at 3%

• Volume growth continues to outpace Value growth as cheaper brands, especially, the Amla category has rebounded the fastest

• Bajaj Hair Oil Market Share reached all time high at 11.1% for Jan - Feb ‘21

• International business grew by 10.2% though the overall size of the business is still relatively small however management continues to focus on being profitable

• Launched new product – Bajaj Amla Aloe Vera which is witnessing good response

• Working on the revised corporate organisation; the company has also restructured the incentives for employees and is increasing variable components in order to keep the %age cost low

• Not looking for any inorganic opportunity as of now

• ADHO has recovered sharply and has grown by 6% for FY21. Large pack size are doing well than sachets

2 Likes

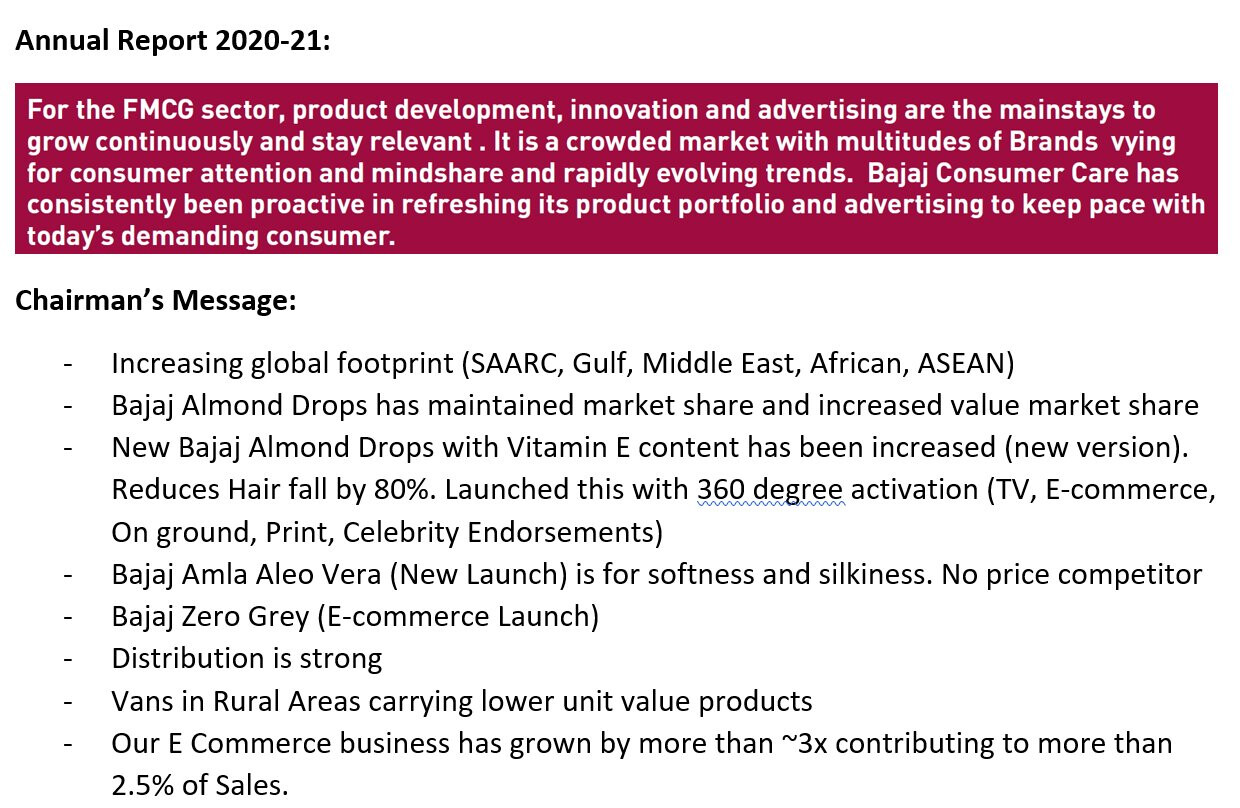

Bajaj Consumer Annual Report Summary!

Hoping to see better results of the company in Q1! (doubtful given the lockdowns)

Your thoughts in the comments, please!

Disclaimer: Tracking & Planning to Invest

2 Likes

Although I had sold off this onetime my largest holding and decided never to look back, but taking learning from @nav_1996 of never ever to write off anything - I decided to check on few things here…

When last I tracked it, the management had plans to use the IPO money for acquisitions. They started with a small acquisition to begin with to understand the complexities etc. It was Nomarks. Nomarks was a category creater and a leader in a niche segment at that time. This acquisition was to prepare the company for larger acquisition in future to transition itself from a single product to multi product company.

Almost 5 years hence -

- What is the performance & roadmap for Nomarks? Are they able to use their distribution strength to scale it up? What is the vision ahead or have they written it off because they dont seem to speak about it

- What is the situation and roadmap for the pledged shares?

- What are the plans and vision on acquisition/capital allocation?

- They drastically reduced their dividend it seems, what is the dividend policy?

- Today still they are predominantly a single product company with bajaj almonds contributing almost 90% of their sales/profits (Pls correct me if wrong) - Are they now content with being a single product company? Or do they have any plans?

As I see these will be the first questions I would ask and try to check again on this. Would be great to know others thoughts on it as well.

I can see there are lot many variables above and thats why it is available relatively cheap in FMCG pack. We need to check if it is an opportunity or a trap…

2 Likes

As far as I understand, they are trying to innovate more in the Bajaj Almonds section itself. The Bajaj Zero Grey, Bajaj Aleo Vera, etc.

1 Like

**Bajaj Consumer Care Limited has launched new Products -

Bajaj 100% Pure Oils

- Castor Oil,

- Olive Oil and

- Jojoba Oil in the domestic market.

100% pure coconut oil already in market since July 21 end**

1 Like

What value does hair oil (specially mineral oil based) provide? How people’ consumption pattern changes with increasing income? As I do not use any hair oil my self from 15+ years … except occasional use of coconut oil.

So basically one line question would be, is mineral oil based hair oil a stagnant or declining category?

I had this stock in FY19-20-21. Now tracking it for learning purpose.

1 Like

Have been studying this company for the past few weeks. In the latest concall there was an interaction which stood out. Usually when someone asks a question about the stock price the management usually says it’s better to concentrate on business performance etc… however, in the concalls there have been a lot of tired investors and Mr nandi actually tried answering it.

{kind=link}

Mr nandi is obviously a bit frustrated about the dependence on ADHO and i do believe he is trying his best to diversify the company a bit more. He has had less than 2 years to make significant changes and has been thrown into a covid, followed by inflationary environment with Bajaj consumer being particularly affected since mineral oil is a derivative of petroleum(currently studying the safety and long term viability of mineral oil and it’s FDA approved and still recommended so i don’t see an issue with the actual use of mineral oil apart from dependance on pricing). The way i see it is there is a lot of good here… ie Promoters with low chance of CG issues and good communication via presentations and concalls, High return ratios, No debt, low valuations… the main issues are

- No fixed dividend policy: This is understandable since they need to basically create brand new growth drivers and de risk from adho. If they can maintain atleast the rs. 8 of the last 2 years then the yield is good. If they can go back to their glory days of 11 to 14 then it will be a huge upward surprise. Problem is noone really knows what to expect here.

- Stagnant sales and dependance on one product: Again, dependence on a product like Adho which uses mineral oil and is a product that many of us aren’t the target market of. And hence why it’s difficult to guage what will happen here. Diversifying should improve this in the long run

The main thing is management knows the above and is obviously frustrated by it. i do believe there could be an investment opportunity here over a long term and there could be a turnaround brewing though it’s still a few quarters/years away.

Disc: Not invested. Will initiate a tracking postion after a few quarters since things look like they’ll get far worse before they get better and a good MOS is definitely needed here… at the right price it’s definitely not a bad business to own (I’m greedily hoping for low 100s)

1 Like

What are your thoughts on -

- Pledge share issue

- Promoters pledging shares not for companies growth but need in other businesses like Power.

- Stake sale for same reason

- Since IPO, they wanted to de-risk. Covid came only in 2020.

- Many FMCG firms de-risk ed during Covid itself eg. Marico created a completely new Foods division.

- I read few months back that they changed their de-risk strategy to focus on hair oils only as per suggestion by some consulting firm…nomarks acquisition also didn’t help.

All this makes me surprise how did it gain market leadership in light hair oil…and if it can do it in one area…why not in other…what’s stopping them since almost a decade?

Disc. Views personal and no buy/sell recommendation. I can be completely wrong in my assessments

Hey @Investor_No_1

You’ve been tracking/owning the company far longer than i have so my knowledge will be very base level and I’m still months away from understanding the business properly and hence posting here.

Regards pledged shares it was the first thing I checked and i referred this article which talks about stake sale to remove pledge. Made sense to me for someone who only recently began tracking the company but I’m sure there’s more under the surface that someone tracking it for a decade could add

This covered both points 1 and 3 for me… not fully satisfied but that’s all I looked into regards the pledging since it was a while back.

Roping in Mr Nandi is a sign of intent for me. In organisations like these one tends to rest on their laurels and adho was a cash cow for them until it wasn’t. Changing the culture of an entire organisation takes time… should they have started earlier? Yes… however, the company is available at current valuations because they didn’t. Time will tell if they’ll actually manage to gain market share in their other products. I’m hoping a few quarters more information will give us a signal regards the same… Mr nandi is a good horse to back for this though usually his product profile is a bit different. Using a consultant is ok in my book since they have had employees selling the same/similar product for years and outside eyes would help them see things differently.

No marks was a puzzler for me too and I’m still trying to figure it out. Again, it was a relatively small acquisition at rs. 150 crore from 2013 so I dint look into it in detail yet. However, they did say they’d look at more companies after and never did. Maybe it just dint work out the way they expected and they dint get to leverage it using their distribution channels.

All in all its a horrible business right now. However, the fact they can still maintain their market share in adho means management can scale a product and could provide some upward surprises in other products too. Only time will tell though and hence why waiting out a few quarters makes sense. I’m going to be asking for a huge margin of safety here to cover all these risks. If it does indeed crash to near rs. 100 i will be interested since I’d be willing to sit through the tough transition at that price point. Until then I’m just observing and studying and hopefully il be able to answer your questions better in a few months

Edit: A day after this post it rose 10 percent with good volumes so expecting it to go to near 100s may not happen. Sometimes buying a company at its worst point does make sense atleast to some buyers somewhere by the looks of it.

3 Likes