Raghuram_Rajan_View_GCC.pdf (1.4 MB)

Raghu ram rajan view on GCC

1 Like

1 Like

Hi there folks!

Do we have any visibility in terms of new seats coming online in FY26?

1 Like

A very insightful discussion on how workspaces are evolving in India.

The management is quite optimistic about FY26. They are guiding for revenue growth of 30%. But it is the valuations that don’t seem comfortable.

Awfis’s 2/3rd occupancy comes from GCCs.

2nd order thinking: The way I am seeing AI impact on IT and other knowledge based roles and functions, AI will pull down gross additions (vis-a-vis estimates) for GCCs over next 2-3 years.

I like everything about awfis but this single factor may act as gravity to awfis’s growth in medium term.

1 Like

ANy business coming out of losses have high PE only later it will reduce Take an example of delihivery or any company that is poised from negative PAT to positive PAT in the first year PE looks like elivated only.

2 Likes

I m also figuring out this calculation every site has a different way, that raises a question how much money this business is really making is a question . Can someone pls help us understand.

1 Like

Even if it’s the case.. More and more companies become Lean in terms of employee strength right?

So, a 400-500 employee company may stay there or reduce to 200-300 employees assuming the same productivity can be achieved with half the size by leveraging AI

Now, If you think about it. why would companies now want to invest or continue in a big self managed spaces?

They’d rather opt to be in a flex spaces right? Coz they have no clue how their employee strength would turn out to be in the near future.

Personally, I’m currently under the impression that demand would only go up..

2 Likes

Additionally, it’s also worth looking at other metrics like Price to OCF and Price to FCF

Companies like AWFIS have huge depreciation on accounting but there’s no actual cash outflow

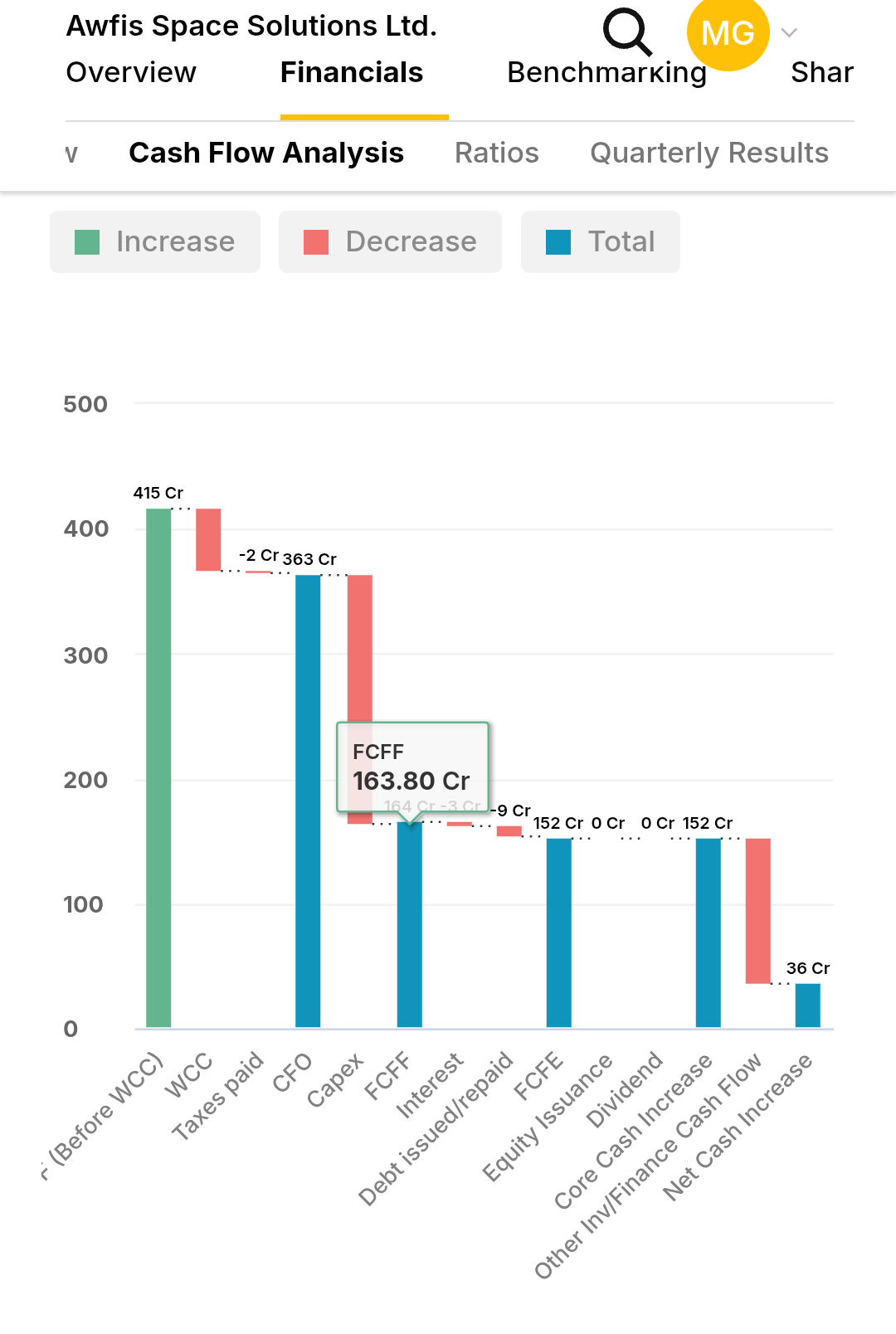

If you see, the Free Cash Flow of AWFIS for FY25 is about 160 crores.. It’s a lot of cash isn’t it?

At the current market cap, it’s trading at less than 30 times FCF which I believe is a decent value if not cheap for a high growth company (as well as the biggest player in it’s sector)

Open to hear other’s perspective as well..

Disc: Invested and Biased.

~240 cr lease liability will have to be deducted to reach correct operating cash flow I feel. It shows in financial cash flows in statement.

3 Likes

Hi Raj,

What is the source for this data?

Aside to all,

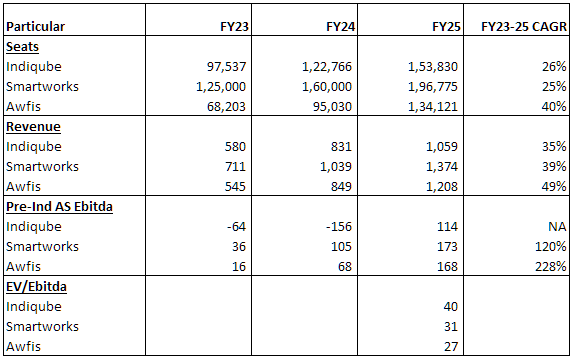

Help needed: Looking for any report that covers the competitive landscape of the industry - comparing major players in India

Not exactly the report but more info here –https://www.youtube.com/watch?v=HKORPnHVTAY&feature=youtu.be

Fident Fineprint-2 (Flex leasing vs Hotels, Malls and REITS).pdf (848.0 KB)

Deep dive on flex leasing

1 Like

Why is the stock falling so much despite good results ? any thing that I am missing ?

3 Likes