insider trade: Acquisition of 43,783 equity shares worth Rs 11.81 lacs by promoter groups

insider trade: Acquisition of 4,616 equity shares worth Rs 1.20 lacs by promoter groups on 15.03.2019

insider trade: Acquisition of 26,634 equity shares worth Rs 6.90 lacs by promoter groups

The article is on Synthite industries which is a leader in this segment.

https://www.outlookbusiness.com/specials/the-power-of-i_2017/indias-tastemaker-3621

1 Like

Hi Mahesh,

Hope all is well! Are you still tracking the company? What are your current views on the company and any new developments for a few years and future outlook that you can comment on? Thought the annual report was very informative. Thanks

1 Like

Hi Sahir, I’ve just begun researching AVT and noticed this thread seems fairly inactive.

The company seems well positioned for growth under its young CEO.

Would you be willing to share any of your more current research on the thread. I will do the same as I start the process.

Ive noticed that the big players in this space like Gavaudun, IFF and Symrise, probably don’t see AVT as a competitor yet, but they are a good proxy’s for AVT’s long term potential.

Hi Arjun,

Unfortunately, I have misplaced by research doc I made on AVT Natural but found the one with the questions I had. Did this a few months ago, some of the questions were answered too but I have no idea because I stopped tracking it but you might find these useful. Sorry for the delay and wish I could give you my research doc. I Will send it to you as soon as I find it

Why are the margins varying so much?

All these products, do you require to use them immediately or can they be stored over time? What is their inventory storage?

Proper facility if they have that they don’t depend on rain

How much of the raw material do they grow themselves? How much do they buy?

How much of the change are you seeing in the makeup industry?

Where is the growth coming from

What new products

What is the safety stock you maintain?

How much more can the margins contract? Worst case

How much can they expand? With new products?

Hi Sarita,

AVT is very much alive and worth buying in my opinion. But don’t take my word for it. Do some digging.

That being said:

The company has a very long track record in the oleoresin industry, is family run with very ethical management that also owns other very successful privately held companies, and seems to be at an inflection point. Namely, they are expanding from commodity goods into value added goods that they would sell directly to customers as opposed to through wholesale. It is similar to the process that companies like Marico and Godrej went through in their early days.

This inflection point is further evidenced by a healthy percentage of R&D spending over the last few years, vertical integration of their supply chain and an increased role of Rahul Thomas, the Chairman’s son. He currently leads marketing and sales but will be successor to his father over time.

This recorded general meeting gives you a good understanding of the demeanor of senior management.

https://www.avtnatural.com/shareholders-information/#sec8

The opportunity here is a 5-10 yr bet that the stock will be lifted by both steady earnings growth and multiple expansion as they transition from commodity player to value added product player. It’s currently a 2% position in my portfolio putting it in the “riskier plays” category of Indian companies I own.

Cheers,

Arjun

3 Likes

I think no one in this thread had noticed their animal nutrition business has grown from 67 lakhs to 8.8 crores from FY21 to FY22, if someone knows what they are doing with this business let us know because Animal Feed or Nutrition is a billion dollar business in India.

4 Likes

Anybody aware what’s going on with the company. The sales this quarter are down significantly. Tried to reach the IR , but there is no reply.

Anybody attended the AGM. If you can update the points here will be helpfull.

Just a follow-up on Dhawal’s reply. Did anyone attend the AGM? Any updates would be helpful. Cheers

37th AGM transcript is there on here

anybody have any update about the company, the price and volume has given sharp move this week?

1 Like

Posted QOQ better but YoY poor result

Hi everyone,

I’m new to investment journey and somehow came through this company. Does anyone tracks? A short summary on present and future outlook will be very helpful!

Is someone still tracking this company?

I have been invested in this company for quite sometime now and tbh the company doesn’t look in so much of a great shape right now. The main issue is not the business or product but the inverse situations and headwinds.

As per their latest annual report, they attributed the decline to 2 factors pre-dominantly,

- El Nino

- Chinese dumping

The issue seems to be still prevailing as results are not in line with expectations.

In addition to that the borrowings and trade receivables are at all time highs. Margins don’t seem to be bouncing back to their historical levels (for reasons as stated above).

Technically seems to taking support at 78-80 levels.

Invite counter views or additional points.

Discl. - Invested.

1 Like

I was screening for Tariff tantrum plays and this was a company with exports predominantly to the US and Europe

China+1 seems to be an inevitability irrespective of the outcome of the current trade war(despite recent news about de-escalation with China). The overarching message seems to be to curb unfair trade practices like govt subsidies, artificially weak currency etc. and could strikingly feature in deals being made.(I’m not a macro expert)

I was delighted to see the management fit my long-term buy and hold criteria

I look for CHAD management - ones with Competence, Heart, Ambition and being Down-to-earth

- Competence has already been illustrated by other posts - one point I wanted to highlight is them bagging a TWENTY YEAR arrangement with Kemin from 2008 to 2028.

- Heart - great corporate governance - strong board including a member from the Murugappa group, no balance sheet bombs, transparent in AGMs, great culture - distribution of remuneration and its growth isn’t too heavily skewed towards KMP, no firing of employees during covid, promoter’s son had to start from the bottom of the org

- Ambition - entering into multiple products to derisk out of marigold oleoresins and continuing to do so(from decaf and instant tea to animal nutrition(at 30cr in FY24 vs 13cr in FY23) and proposed forays into crop science), R&D spend % consistently trending up which is impressive in a co like this where it’s easy to sit on the laurels of the current Kemin contracts

- Down-to-earth - display of calibrated confidence in their commentary in AGMs, owning their losses as much as wins (eg. in rosemary extracts), not gluttons for assets to stroke egos - letting cash sit on the balance sheet(described as a common tendency in large business groups in the book Face Value by Debashis Basu + plenty of anecdotes and examples still present in India Inc)

The industry structure and competitive position left much to be desired. However this seems to have the potential to change given the recent developments.

The legacy products and their applications have been thoroughly discussed in this forum so I hope I can add something around the margins

Marigold oleoresins - Management claims that the Chinese undercutting in the feed grade market is primarily a result of govt subsidies - the exact practice that Trump is against. Feed grade market is 70-80% of the marigold market so this could be massive. While customers have signalled intent to procure from India for strategic diversification reasons, the Chinese set the benchmark prices for these negotiations. Any deal involving better Chinese business practices/a lower but permanent tariff rates goes a long way. The margins here are 18-22% (twice that of spice oleoresins)

The speciality teas segment seems to have caught the attention of people over the last few years. Fellow Huberman Lab listeners would know the madness around yerba mate(which is NOT grown in India). Neither am I knowledgable enough to know other such trends in the teas segment nor is the management willing to disclose more on specific products/end uses. I could however observe growth in a HS code probably linked to similar trends(data below)

Information is scant regarding the animal nutrition and crop protection segments but the 100cr target in the former(and 30cr in FY24) inspires confidence

There are little things that represent a well-run organisation such as the choice of instruments to park funds in. All their surplus money is in arbitrage funds.

Supporting data for the above claims:

| Year | No. of Employees | % Increase in Median Employee Remuneration | % Increase in Median Non-Management Employee Remuneration | % Increase in Median Management Remuneration | Management Personnel & Salary (Rs.) | % Increase in Management Personnel Salary |

|---|---|---|---|---|---|---|

| 2015 | 215 | 38.62% | - | - | Mr. M.S.A. Kumar (MD): 2,19,79,800 | 20.76% |

| Mr. A. Ramadas (Sr. VP & CFO): 4,655,839 | 10.23% | |||||

| Mr. Dileepraj. P (Company Secretary): 1,597,891 | 7.35% | |||||

| 2016 | 226 | -17.46% | - | - | Mr. M.N. Satheesh Kumar (President & COO – Manager): Not Specified | -8.93% |

| Mr. A. Ramadas (Sr. VP & CFO): Not Specified | - | |||||

| Mr. Dileepraj. P (Company Secretary): Not Specified | 3.41% | |||||

| 2017 | 231 | 6.17% | - | - | Mr. Ajit Thomas (Non-Executive Chairman): 39,85,100 | 11.69% |

| Mr. M.N. Satheesh Kumar (President and CEO): 82,24,000 | 14.44% | |||||

| Mr. A. Ramadas (Sr. Vice President and CFO): 53,36,000 | 5.72% | |||||

| Mr. Dileepraj. P (Company Secretary): 18,17,000 | 6.48% | |||||

| 2018 | 244 | 6.33% | - | - | Mr. Ajit Thomas (Non-Executive Chairman): 34,39,000 | (13.70)% |

| Mr. M.N. Satheesh Kumar (President and CEO): 91,49,000 | Not Specified | |||||

| Mr. A. Ramadas (Sr. Vice President and CFO): 13,39,000 | Not Specified | |||||

| Mr. Dileepraj. P (Company Secretary): 19,42,000 | 9.24% | |||||

| 2019 | 252 | 14.53% | 15.01% (Non-Managerial) | 1.36% (Managerial) | Mr. Ajit Thomas (Non-Executive Chairman): 29,60,000 | (13.94)% |

| Mr. M.N. Satheesh Kumar (President and CEO): 95,46,000 | 4.34% | |||||

| Mr. A. Ramadas (Sr. Vice President and CFO): 62,83,000 | 6.12% | |||||

| Mr. Dileepraj. P (Company Secretary): 20,89,000 | 7.57% | |||||

| 2020 | 275 | 4.68% | 4.54% (employees other than managerial personnel) | 6.10% (managerial personnel) | Mr. M.N. Satheesh Kumar (President and CEO): 1,03,13,200 | 8.03% |

| Mr. A. Ramadas (Sr. Vice President and CFO): 65,20,761 | 3.79% | |||||

| Mr. Dileepraj. P (Company Secretary): 22,24,504 | 6.49% | |||||

| 2021 | 322 | 7% | 6.89% (employees other than managerial personnel) | 7.63% (average increase in managerial personnel) | Mr. M.N. Satheesh Kumar (President and CEO): 1,12,86,667 | 9.44% |

| Mr. A. Ramadas (Sr. Vice President and CFO): 68,69,831 | 5.35% | |||||

| Mr. Dileepraj. P (Company Secretary): 24,04,458 | 8.09% | |||||

| Sharon Josh (Company Secretary): 86,694 | N/A (Appointed mid-year) | |||||

| 2022 | 320 | 6.34% | 6.34% (employees other than managerial personnel) | No increase (in salaries of managerial personnel) | Mr. B. Krishna Kumar (Sr. Vice President Operations and Manager): 75,68,000 | NIL |

| Mr. A. Ramadas (Sr. Vice President and CFO): 71,89,000 | 4.65% | |||||

| Mr. Sharon Josh (Company Secretary): 6,64,000 | N/A (Full year salary, no prior year data in this table) | |||||

| 2023 | 294 | 12.87% | 13.05% (employees other than managerial personnel) | 15.47% (average increase in managerial personnel) | Mr. B. Krishna Kumar (Sr. Vice President Operations and Manager): 87,38,000 | 15.47% |

| Mr. A. Ramadas (Sr. Vice President and CFO): 78,88,000 | 10.97% | |||||

| Mr. Sharon Josh (Company Secretary): 8,61,000 | 29.74% | |||||

| 2024 | 315 | 22.76% | 17.77% (employees other than managerial personnel) | 10.33% (average increase in managerial personnel) | Mr. B. Krishna Kumar (President & Manager): 99,33,000 | 13.67% |

| Mr. A. Ramadas (Sr. Vice President and CFO): 84,88,000 | 6.40% | |||||

| Sharon Josh (Company Secretary): 9,56,000 | 10.92% |

Rahul Thomas’s career(son of Ajit Thomas):

Pre-AVT Experience and Education:

-

Rahul Thomas holds a Bachelor’s degree in Economics from the University of British Columbia

-

He worked for 3 years at Shell Energy North America (Canada) Inc., Calgary, AB in various capacities: Contract Coordinator, Risk Analyst, and Operations Analyst. This provided him with experience in Sales contract administration, Risk management, and Logistics

-

Subsequently, Mr. Rahul Thomas completed a Master of Business Administration (MBA) from the University of Alberta, Edmonton AB, specializing in International Business, Family Business, and Finance

-

Post his MBA, he had a short stint with KPMG as a Senior Consultant

-

During the year 2005, he worked as a Summer Intern at AVT McCormick Ingredients Private Limited and as a Marketing Intern at McCormick, Canada

Career Progression within AVT Natural Products Limited:

February 3, 2014: Mr. Rahul Thomas started working with AVT Natural Products Limited as Manager (Strategic Planning & New Business Development)

Up to March 31, 2017: His salary in this role was less than Rs. 2.50 lakh per month

2017-2023: He continued in the role of Manager (Strategic Planning & New Business Development) with an annual remuneration exceeding Rs. 30 lakhs (as mentioned in the 2018 report).

March 31, 2023: Mr. Rahul Thomas ceased to be an employee of the parent company, AVT Natural Products Limited .

April 1, 2023: He was appointed as Director / General Manager in a Subsidiary of AVT Natural Products Limited. The specific subsidiary is identified in the 2023 report as AVT Natural FZCO (AVT Dubai), a wholly-owned subsidiary incorporated on March 28, 2023, in Dubai, UAE, for marketing various products .

June 12, 2024: Mr. Rahul Thomas was appointed as an Additional Director of AVT Natural Products Limited

R&D:

| Year | Total R&D Expenditure (Rs.) | Consolidated Revenue (Rs.) | R&D Expenditure as % of Consolidated Revenue |

|---|---|---|---|

| 2012 | 2,10,38,971 | ||

| 2014 | 3,73,40,359 | ||

| 2015 | 3,01,14,024 | ||

| 2015-16 | 3,83,70,791 | 274,49,39,068 | 0.14% |

| 2016-17 | 4,19,69,039 | 314,77,06,829 | 0.13% |

| 2017-18 | 4,43,34,105 | 32,82,76,100 | 1.35% |

| 2018-19 | 7,05,58,078 | 39,64,10,500 | 1.78% |

| 2019-20 | 10,63,18,573 | 51,72,59,200 | 2.06% |

| 2020-21 | 10,39,26,769 | 48,51,27,900 | 2.14% |

| 2021-22 | 10,42,58,569 | 55,93,89,300 | 1.86% |

| 2022-23 | 13,16,85,712 | 58,21,65,700 | 2.26% |

| 2023-24 | 15,06,53,268 | 51,72,59,200 | 2.91% |

They claim to have tie-ups with universities abroad for R&D which could have its own advantages - based on the nature of the arrangement, R&D equipment capacity & consumables could be fungible based on the arrangement + a silo away from the business operations would really help focus on breakthroughs without fretting over business outcomes, problems like the innovator’s dilemma etc so they should get a non-trivially better outcome out of a lot of these spends

Product Segments:

By company’s segmentation:

| Year | Marigold Oleo Resin/Extracts (Rs. lakhs) | Marigold Oleo Resin/Extracts (%) | Spice Oleo Resin/Extracts (Rs. lakhs) | Spice Oleo Resin/Extracts (%) | Instant and De-Caffeinated Tea (Rs. lakhs) | Instant and De-Caffeinated Tea (%) | Animal Nutrition (Rs. lakhs) | Animal Nutrition (%) | Job work income (Rs. lakhs) | Job work income (%) | Total Revenue (Rs. lakhs) |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2019 | 15360.26 | 40.49% | 11262.78 | 29.69% | 9754.02 | 25.71% | 420.72 | 1.11% | - | - | 37938.50 |

| 2020 | 15360.26 | 40.49% | 11262.78 | 29.69% | 11082.93 | 29.21% | 232.53 | 0.61% | - | - | 37738.50[^1] |

| 2021 | 16276.13 | 34.60% | 17936.69 | 38.13% | 12762.05 | 27.13% | 68.02 | 0.14% | - | - | 47042.89 |

| 2022 | 24073.72 | 44.86% | 17487.60 | 32.60% | 10205.27 | 19.02% | 764.42 | 1.42% | 1122.36 | 2.09% | 53653.37 |

| 2023 | 25452.31 | 43.71% | 14986.48 | 25.74% | 14916.11 | 25.62% | 1775.62 | 3.05% | 1094.75 | 1.88% | 58225.27[^2] |

| 2024 | 17829.36 | 34.47% | 13768.37 | 26.62% | 16203.97 | 31.32% | 3031.90 | 5.86% | 892.32 | 1.73% | 51725.92 |

By HS code:

| 8-digit HS Code | Description | FY23 Export Value ($) | FY23 Sales % | YoY Growth FY23 to FY24 (%) | FY24 Export Value ($) | FY24 Sales % | FY25 Export Value ($) | FY25 Sales % | YoY Growth FY24 to FY25 (%) |

|---|---|---|---|---|---|---|---|---|---|

| 33019029 | Other essential oils and oleoresins | 9,700,000 | 13.90 | -55.67 | 4,300,000 | 10.73 | 7,000,000 | 12.89 | 62.79 |

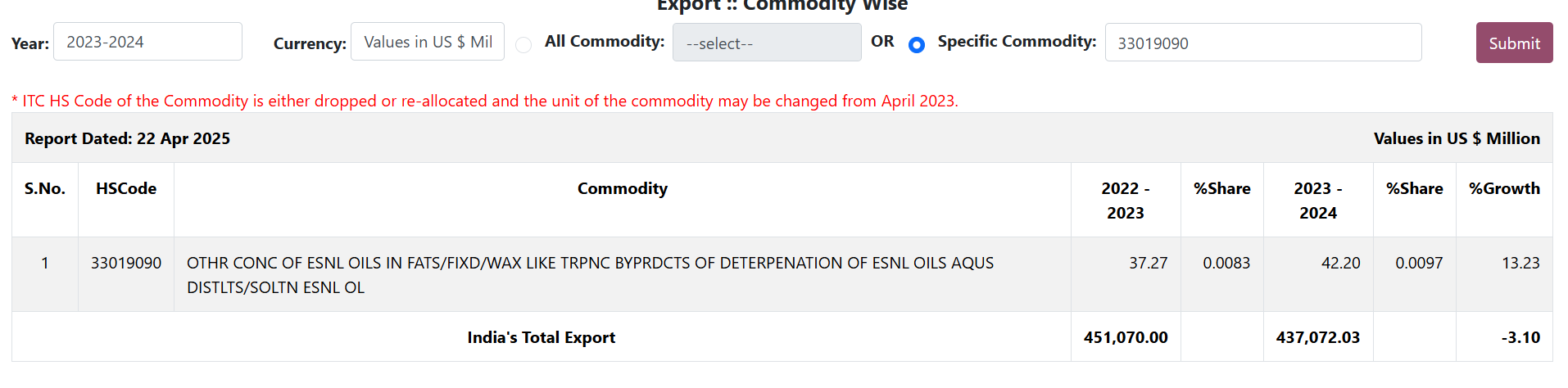

| 33019090 | Other concentrates of essential oils | 30,600,000 | 43.85 | -30.07 | 21,400,000 | 53.38 | 18,700,000 | 34.44 | -12.62 |

| 33019022 | Capsicum oleoresins | 6,700,000 | 9.60 | 20.90 | 8,100,000 | 20.21 | 6,400,000 | 11.79 | -20.99 |

| 33012950 | Other essential oils, n.e.s. | 866,700 | 1.24 | 15.39 | 1,000,000 | 2.49 | 1,600,000 | 2.95 | 60.00 |

| 33019013 | Oleoresins of ginger | 756,800 | 1.08 | 243.64 | 2,600,000 | 6.49 | 1,000,000 | 1.84 | -61.54 |

| 33019014 | Oleoresins of turmeric | 1,500,000 | 2.15 | 33.33 | 2,000,000 | 4.99 | 1,600,000 | 2.95 | -20.00 |

| 33019016 | Oleoresins of celery seed | 10,700 | 0.02 | 130.84 | 24,700 | 0.06 | 22,900 | 0.04 | -7.29 |

| 33012935 | Essential oils of pepper | 73,400 | 0.11 | -23.57 | 56,100 | 0.14 | 96,600 | 0.18 | 72.19 |

| 33012949 | Essential oils, n.e.s. | 663.80 | 0.00 | -31.84 | 452.50 | 0.00 | 1,200 | 0.00 | 165.19 |

| 33012926 | Essential oils of fennel | 7,700 | 0.01 | -50.65 | 3,800 | 0.01 | 14,500 | 0.03 | 281.58 |

| 33012942 | Essential oils of coriander | 0 | 0.00 | N/A | 48,900 | 0.12 | 24,900 | 0.05 | -49.08 |

| 33019011 | Fenugreek oleoresins | 5,200 | 0.01 | 25.00 | 6,500 | 0.02 | 46,900 | 0.09 | 621.54 |

| 33012590 | Other mint oils | 201,000 | 0.29 | -100.00 | 0 | 0.00 | 1,900,000 | 3.50 | N/A |

| 33019017 | Oleoresins of cumin | 8,500 | 0.01 | 50.59 | 12,800 | 0.03 | 12,900 | 0.02 | 0.78 |

| 33012990 | Other essential oils, n.e.s. | 31,000 | 0.04 | -52.90 | 14,600 | 0.04 | 350.70 | 0.00 | -97.60 |

| 33019012 | Oleoresins of mustard | 203,100 | 0.29 | -99.36 | 1,300 | 0.00 | 16,400 | 0.03 | 1161.54 |

| 33019024 | Oleoresins of nutmeg | 16,600 | 0.02 | -86.75 | 2,200 | 0.01 | 21,600 | 0.04 | 881.82 |

| 33012922 | Essential oils of cumin | 4,800 | 0.01 | 4.17 | 5,000 | 0.01 | 3,700 | 0.01 | -26.00 |

| 33019023 | Oleoresins of cardamom | 9,700 | 0.01 | -75.26 | 2,400 | 0.01 | 3,400 | 0.01 | 41.67 |

| 33019021 | Oleoresins of clove | 0 | 0.00 | N/A | 0 | 0.00 | 613.40 | 0.00 | N/A |

| 33021090 | Other mixtures of odoriferous substances | 468,100 | 0.67 | -8.86 | 426,700 | 1.06 | 0 | 0.00 | -100.00 |

| 21012010 | Tea extracts | 12,300,000 | 17.62 | 1.63 | 12,500,000 | 31.18 | 9,500,000 | 17.50 | -24.00 |

| 21012090 | Other tea or maté extracts | 1,100,000 | 1.58 | 27.27 | 1,400,000 | 3.49 | 2,400,000 | 4.42 | 71.43 |

| 12119029 | Other plants and parts for perfumery | 396,600 | 0.57 | -72.09 | 110,700 | 0.28 | 3,100,000 | 5.71 | 2699.46 |

| 11063010 | Flour, meal of mango | 171,500 | 0.25 | -26.59 | 125,900 | 0.31 | 168,000 | 0.31 | 33.44 |

| 31010099 | Other animal or vegetable fertilizers | 0 | 0.00 | N/A | 0 | 0.00 | 14 | 0.00 | N/A |

| 84195099 | Other heat exchange units | 0 | 0.00 | N/A | 0 | 0.00 | 7,200 | 0.00 | N/A |

| 09024090 | Other black tea (fermented) | 4,200,000 | 6.02 | -100.00 | 0 | 0.00 | 0 | 0.00 | 0.00 |

| 09022090 | Other green tea | 385,200 | 0.55 | -100.00 | 0 | 0.00 | 0 | 0.00 | 0.00 |

| 09024030 | Black tea dust | 102,300 | 0.15 | -100.00 | 0 | 0.00 | 0 | 0.00 | 0.00 |

| 09041190 | Other pepper, neither crushed nor ground | 35,600 | 0.05 | -100.00 | 0 | 0.00 | 0 | 0.00 | 0.00 |

| 13021919 | Other vegetable saps and extracts | 285 | 0.00 | -100.00 | 0 | 0.00 | 0 | 0.00 | 0.00 |

| 33019015 | Oleoresins of asafoetida | 6,200 | 0.01 | -100.00 | 0 | 0.00 | 0 | 0. |

All over the place and a bit puzzling. Other than some minor consistent growth products like Other tea or maté extracts, I’m not really sure what the conclusion to be drawn is.

Management doesn’t give market share but we could check the total exports from India per HS code and calculate market share but it doesn’t seem like the company doesn’t have all the products within the HS code.

eg. Marigold oleoresins seem to come under 33019090 but doesn’t seem to be the only product under that code. FY23 market share seems insane but drops off a cliff in FY24 to around 50%

Fwiw, good Q4 to get us through to the AGM where we can get more clarity regarding the implications of the Tariff tantrum. Not sure if anything can be inferred from this quarter yet.

Some things which are very unlikely to change in this business are inventory days unless the harvest period of the product mix spreads perfectly across the calendar

However, them gaining enough size and strategic importance would lead to contracts softening these issues if they aren’t like that already(eg. Foods & Inns’s domestic customers - Pepsi and Coca Cola(I think they supply 50% and 25% of mango pulp(or more) to each iirc… don’t quote me) have contracts with them which have warehousing and interest costs for WC loan built into them) so higher inventory days doesn’t necessarily make it a bad model unless their storage infra is so poor leading to massive write-off potential(which hasn’t happened historically here)

Overall, this seems to be a very well-run business at an interesting juncture on multiple fronts that could significantly alter the future earnings quality, growth and hence valuations.

Disc: invested, pushback highly encouraged

NotebookLM used to collate data only from annual reports. Verified to the best extent but Inaccuracies can’t be ruled out

4 Likes