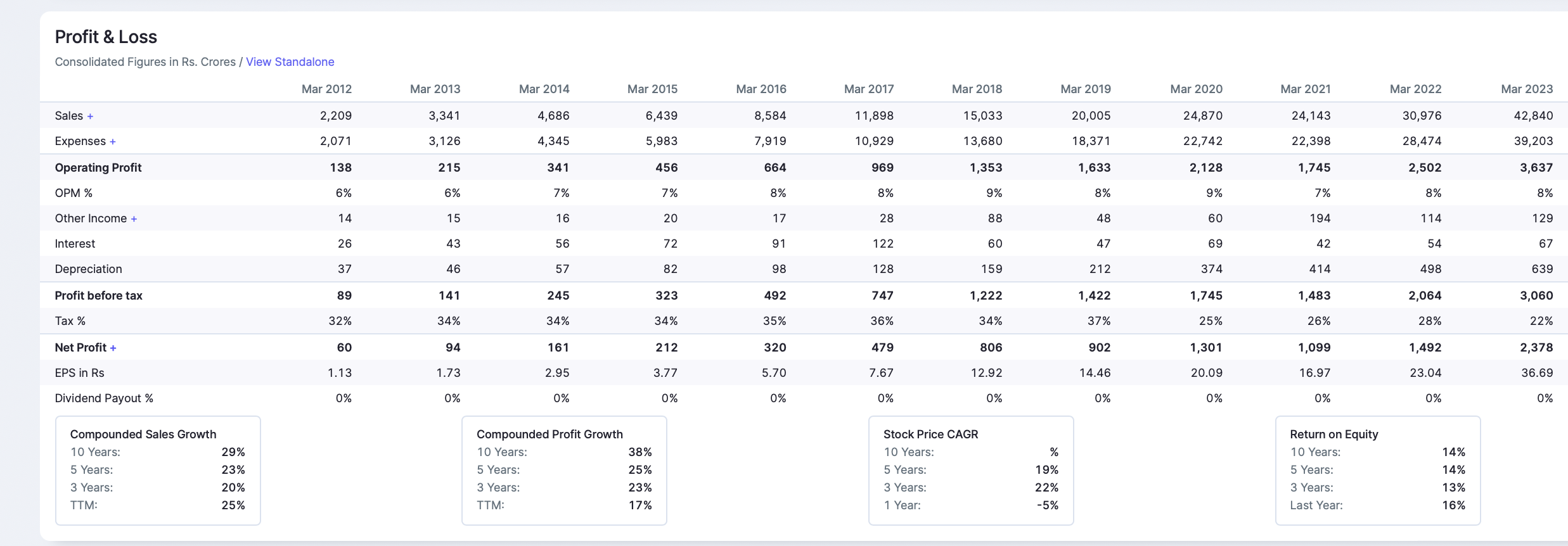

It is mentioned in investor presentation that like to like 2 years revenue growth is 24.2% (page 10).

Number of stores at that time were 234 and Sq. Ft. were 8800000 and revenue from it was 24143 cr.

Rest is mathematics.

It is mentioned in investor presentation that like to like 2 years revenue growth is 24.2% (page 10).

Number of stores at that time were 234 and Sq. Ft. were 8800000 and revenue from it was 24143 cr.

Rest is mathematics.

Rahul-ji , as retail sq ft is 8800000 and Rev is 24143 cr , then the rev /sqft is Rs 27435 for fy21 . But in company update it was mentioned that “Two years and older DMart stores grew by 24.2% during FY 2023 as compared to FY 2022.”

So as per your calculation , Rs 34074 is the Rev/sqft for fy23 with 24.2% growth that means fy 22 rev/sqft is Rs 27435 that means are you assuming that those stores have not grown from fy21 to fy22 ?

Someone above has very well explained about like for like growth. Number of bill cuts- let’s say I and you go to dmart. You bought goods of 50 rupees and I bought that of 30 rupees. Then total bill cuts will be 2. This metric doesn’t tells you anything about the value of those bills.

thanks for pointing out. Yes, agreed as 24.2% growth is over FY22 revenue of stores that existed in FY21. so in above calculations growth from fy21 to fy22 needs to be added.

That shall push 34075 higher and 25755 further lower.

Dmart to justify its valuation needs more profitable growth and that can come from other than grocery sale for which they need to work differently as only selling cheap may not work.

Career Portal [https://career10.successfactors.com/career?company=avenuesupe] of DMART shows below listed openings, which opened in July 2023.

Since these roles never appeared on the portal in the past, I see this as a glimpse of new WIP areas in the business.

Category manager is a pretty common role. This includes buyers, who will determine the selection in each category, and negotiate with suppliers for buying the articles. HPC means home and personal care, which is one of the biggest categories within FMCG non food.

Western womens wear looks like a new category. But it will take sometime to establish. This is because of the high SKU count required ( each design will have multiple sizes). Also, you would need changing rooms in the stores. But this has good margin.

Rest two are pretty standard roles for any retailer.

Any comments on Q1 results? Profit growth softened.

Discretionary spend is yet to pick up. Hence despite revenue growth, no profit growth seen.

When compared with VMART q4 results, it appears people are giving a miss to apparels with ASP of around 300-350 (largely stocked by DMART) but rather choosing at slightly higher levels of ASP around 500 INR - owing to higher aspirations.

With Jun-19 as the base [Ignoring COVID drawdown and recovery period], CAGR of Sale and Profit looks in sync. @iyeron provided the rationale for the drop in OPM else PAT’s CAGR would have been better than sales.

| Jun-19 | Jun-23 | CAGR | |

|---|---|---|---|

| Sales + | 5815 | 11,865 | 20% |

| Operating Profit | 591 | 1,035 | 15% |

| OPM % | 10% | 9% | |

| Net Profit + | 323 | 659 | 20% |

Can you elaborate little more please as I don’t track Vmart ?

An apple to apple comparison for DMART’s apparel (high margin) segment would be VMART, which not only derives 90% of its revenue from fashion clothing but also operates at similar price points.

VMART’s performance trends in FY23 shows 100% growth over FY22 for ASP of 500 plus. Moreover, higher transaction size of around 2000 INR are seen at ASP of ~500-560 INR and transaction size of around 900 INR at ASP of ~380 INR.

It shows people are willing to spend more on high price apparels and also buy more in terms of volume. FY23 sales of other apparel companies (operating at higher price points) show similar trends. While DMART which largely operates at around 300-350 INR ASP seems to have missed the party leading to reduced gross margins.

i think thats a solid bingo observation supported by excellent data points…

India is growing in aspirations and businesses need to match up than just play on value…

zudio is although low in price points (as compared to westside) but equally high on fashion quotient and trends…

as you rightly pointed amd proved with data points as well, dmart lost this value fashion bus… at least as of now…as they seem to stuck to too much value sans increase in fashion quotient…

But the management has been slow and steady and although stick to their original principals but willing to change for better… like how slowly & steadily they adopted and building ecommerce with a unique business model of dmart ready

i happened to visit one dmart ready today…it was one of my first visits to any dmart/dmart ready since many years as i avoid the huge rush

was happy to find it less crowded but a decent sized store having many non grocery items i could scan and purchase with ease…in meantime few people were dropping in for their online grocery orders and some of them picking up few items from decently kept store…

overall this value fashion vs aspiration & trends is something we need to keep close watch … losing this bus for longer time may not be a good proposition…

having said that i trust the management eye for it, future plans for it and ability to change stance if needed… need to watch and learn from them …what they do and when…

disc: invested in trent, dmart hence critical and biased. not a buy/sell recommendation.

with 20%Sales CAGR , operating profit and NP is expected to be in higher range to justify the valuation. Agree with some reasons given above especially comparison with zudio. Growth in Dmart’s sale other than grocery will be key in coming qtrs. And hopefully Addition of ONLY 3 stores per qtr must be one off, otherwise that can be a concern if repeated.

Every store of Dmart has brisk business and is highly profitable. The management will obviously want to open as many stores as possible with same profitability, and clearly limiting to only three stores isn’t because of lack of funds. Shows how difficult it is to build and grow the network of self owned stores like Dmart while ensuring the efficiency of distribution network and preserving the profitability levels they have. It is not something one can do just by providing sufficient money otherwise Reliance would have copied their model by now.

Expensive valuation is also because of logitivity of business nature and not only because of growth , with barely any growth Walmart and Costco get valuation at 30PE - 40 PE, so 80PE-100PE for dmart is justified as the journey is too long to get it to mature phase like Walmart etc.

Costco is 35x NTM because it’s a differentiated business model - flywheel is stronger than it has ever been and market is giving it credit for that.

Walmart is 25x NTM, meanwhile OPM has dropped from 6% to 4% over the last 10 years. 70%-80% of share price appreciation over the last 10yrs has been multiple expansion. Market is giving that multiple since they’re investing into e-commerce. (so it is more a matter of investing through the income statement and multiple expansion reflects that accounting earnings number)

Dmart is at 75x NTM. I think it is the highest quality retail model in India but don’t think there is room for margin expansion (that’s simply not the business model - the idea is to drive topline through passing on savings to the consumer)

If the sales/profits can 10x over the next 10 years - and I slap a 25x multiple on those earnings - you’re getting a 13% cagr - so a LT market average type return. I am not willing to make the bet that the multiple stays at 75x, maybe it falls to 50x.

I think there is longevity of growth and it implies that maybe they can grow earnings for 20 years at 25% - and then if I put a 25x on those earnings - then I make a 18.3% cagr.

Very high quality business, but not a lot of margin of safety at the moment - for a good IRR I need near perfect execution (20yrs of 25% cagr in earnings - that’s 87 times)

I bought at 2k, and thought it was very expensive then. Then it went up to over 5k. I exited at 4.3k.

In last 10 years, 5 year, 3 year Sales growth was 29%/23%/20% ( despite Covid and low inflation ) while profit growth was 38%, 25%, 23% , I feel a similar story can repeat in the next 10 years ( Inflation effect still need to adjust ) so even you growth estimation is lower, also 25 multiple means there is no growth left which I do not see happening, I would still assign 35-50 multiple as there will be plenty room for growth.

~2.5 Hrs. conference call with Analysts/ Institutional Investors : Recording @ DMart (Analyst - Investor Meet Audio Recording - 26.07.2023)

My takeaways:

Thanks for sharing the takeaways…this above point is not very clear… if you can elaborate…what reset and replace merchandise its talking about? which people are key issue and which many new other categories its refering to? Thanks

This should be related to changes in housewear trends - people seem to opt for athleisure for dual purposes. Observed this in one of the recent concall of Page Industries.