My understanding is that If we compare Dmart’s previous year’s Q2 result we could see that Dmart might built inventory but not accounted in Income statement fully in this quarter due to accounting method. Because earlier festive season was in mid October whereas in current year it is in November, hence in earlier year quarter Check-In-Inventory was -320 cr approx where as in current year quarter it is -220 cr which means it does not built full festive inventory yet in Q2 and will do it Q3 which means in coming Q3 Check-in -Inventory will be comparatively less than previous year Q3 (+232 cr).Correct me I am wrong here.

Dmart valued inventory at average. I know the US company they are trying to copy value inventory at first in last out

Probably first in last out will capture cost increases much sooner.

With average inventory, if prices across many skus are at cost plus margin, they will likely not capture price increases that much sooner.

Perhaps. I find it interesting that retailers like Dmart , Future Retail etc follow the weighted average cost method because goods are non standard and are not homogeneous. Maybe because of the sheer volume, its more easy to use this method but i am not sure it accurately represents gross margins.

Amongst other things, for e.g during Dussera/Diwali etc a lot of apparels may be sold so the ideal situation would be to account for the cost of those apparels sold however the weighted average cost makes no distinction between these things and averages out all the cost over all items. So unless, the distribution of items sold closely matches the distribution of items taken in the cost of goods sold the gross margins may be distorted especially in the period around the festive season where shopping habits are materially different.

Maybe i am trying to fit an explanation to the gross margin reduction and that is certainly possible. However, the standard definition of weighted cost of inventory doesnt seem to be well suited to retail where the timing & price of goods sold is vastly different from the timing & cost of their purchase esp for non perishable items.

Hi @bheeshma ,

Thanks for your reply. Here is my attempt to get an idea about upcoming H2 result.

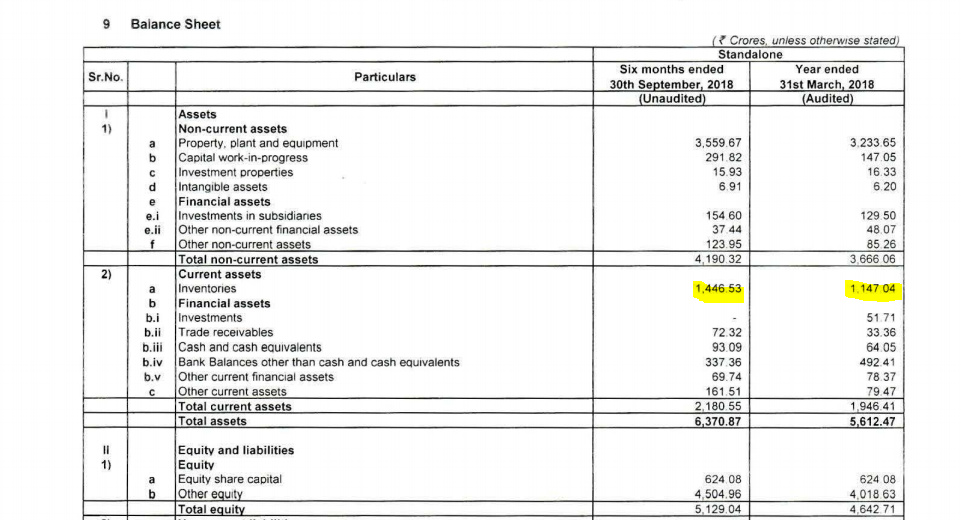

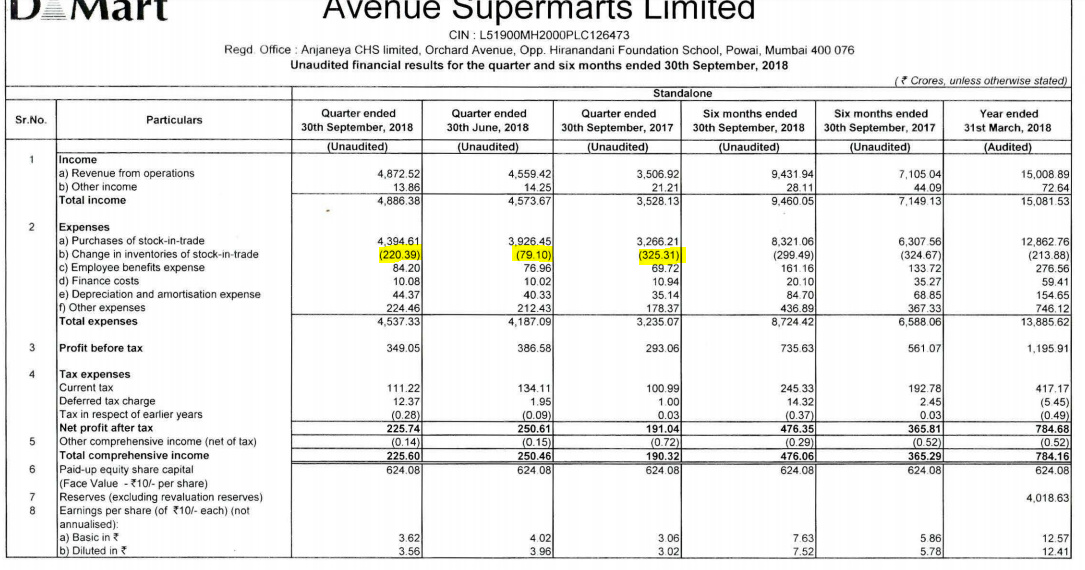

At beginning of H1 2018-19 ,DMART’s inventory was 1147 cr and at the end of this H1 2018-19 is 1446 cr which is almost 300 cr. If we check the same from income statement we will see it in the ’ Change in Inventories of stock in trade ’ -220 cr and -79 cr in Q2,2018-19 and Q1 2018-19 respectively (Minus figure in expense because they still not turned into Sales)

.So if we look at the result from Half yearly perspective rather than quarterly perspective it is not that bad (with 32% rev growth and 30% EBITDA Growth)

Now if we consider that inventory will grow as per the sales in this current financial year ,then we can assume by H2 end the inventory will be 1550 cr approx which means we can expect 100 cr of 'Change in inventories of stock-in-trade ’ in coming H2 2018-19 against 111 cr (237cr -126cr) . which will be the almost same. So EBTIDA will be as per the purchase/sales ratio assuming they will do inventory turnover efficiently as they did in past many years.

Now coming to expense ratio, there is a trend it has been observed that in Q3 and Q4 is 7-7.5% and 9-8.5% range respectively ,so expecting there will be not be any uptick in expense ratio font also .

So as per my understanding there will not be big decline in Gross Margins and EBTIDA margins in H2 which various brokerage reports are forecasting that there will be declines in EBITDA margin in coming quarter also.

Please let me know your views.

Discl: I am not a sebi registered analyst . These are my personal views and I have vested interest in this stock as I am invested.

I think most investors feel and have felt since the longest time that Dmart is an overvalued stock, but i am not in that camp of investors because i really think that it is an outstanding business with a lot of social value. But let me not get into that as i realize that i am a shareholder first and a shopper later.

In my view, the quest in investing is to

A) find business that are scalable + have tremendous entry barriers + ability to hold or increase margins

In time, the basis of investing depends upon the quality of your underlying thesis about the long term earnings growth and how correct you were on that all important call. You have to be correct about your thesis in the end.

The idea is to have a beginning thesis that makes sense and make incremental adjustments to it taking in the confirming and disconfirming pieces of information by having an open mind and then (D) your way through all of it.

My humble submission is every investor has to develop the capacity to suffer from time to time however, the quest really is to be right about the long term earnings growth through a well developed insight which is both different and better.

Having a thesis that is different and better than the prevailing one is what that i am continually trying to inculcate.

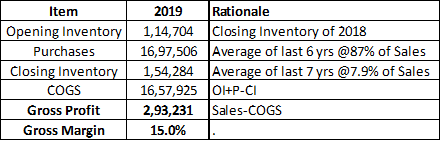

Yes, that would be my view as well. There are some other nos that i have put together which indicate one should expect a good margin improvement rather than a decrease as both the Closing Stock and Purchases number seem to have deviated from historical averages. Here is what i have

The average closing inventory % to sales has been 7.9% over the last 7 years. So i have taken than number. The yoy growth in Sales is 39% and the H1 growth is 33% so i have taken 30% as growth in sales for 2019.

The Purchases figure , I have taken as 87% of Sales which is again the historical average.

Putting all of it together, my estimate of Gross Profit with the Rationale.

If historical inventory and purchase ratios revert to their original in 2019, i think 2019 may be the best ever year for Dmart in their history. I think that Mr Neville Noronha probably knows this and has already started reducing gross margin levels and hence H1 and Q2 was soft. Once the flywheel is in motion its difficult to stop it and all one can do is slow it down.

Do comment if you find an error in the logic. Differential views are always welcome.

Margin does not drop this time due to any business model change and eventually if Lease & Operate model going to happen management never mentioned it was for Growth purpose but mainly for the location of property which they are not getting the ownership.

Location is highly important part of D-Mart core strategy and we can only compare this to the early days strategy of MacD.

Even if I consider margin going to impact due this we are yet not sure how much % they are actually focusing on Lease & Operate model and what % will account for ownership model. As far as I can understand from management commentary that there is no such change in business model but they are open to the alternative if they will not get the property in the right location.

Inventory pilling is a very normal strategy for any retail business considering festive season is around the corner. So even if the margin got impacted nothing has changed fundamentally.

Point to be check in the concall is what % of growth projection they are claiming to achieve in next FY. And for me that should be all to take a decision for new investment in this stock.

The tendency to try and bring everything down to a number is natural for those mathematically bent, including myself. Experience, whether running even the simplest of business or an investment portfolio, however teaches you that boiling everything down to numbers arrived at by mathematical calculations, leads to an automatic anchoring to some sort of mental precision, that seems deceivingly true. But in reality it is false and highly misleading.

I can say this life lesson has been drilled into my cranium so often that it would me remiss of me not to share.

G K Chesterton says it best, “Life is not an illogicality; yet it is a trap for logicians. It looks just a little more mathematical and regular than it is; its exactitude is obvious, but its inexactitude is hidden; its wildness lies in wait.”

Well, when DMart Leases new stores, Revenues will go up. I have a hard time picturing why DMart would lease a new store if it’s not to boost sales. The CEO has been quoted saying that they wish to increase the rate of store growth and they’re not above leasing stores.

Yes, I’ve posted the same thing in this thread already.

Of course, nobody does. As I’ve already explained in this thread several posts earlier, I’ve simply tried to assume Growth in line with the CEO’s comments about increasing store growth rate from 8-10 to 15-20. I’ve also shown how my assumptions are justified. Please do read above.

I didn’t say there’s any fundamental slippage in DMart. It’s still a very good company in my eyes.

That’s fine. But Value doesn’t come from next year’s growth alone. It comes from several years’ growth. But I’m beyond starting another discussion on Valuation in this thread. If I’m right, I’ll get shot down by comments we just saw (Which thankfully are removed now). If I’m wrong, I’ll be shot down anyway. There’s no winning it seems.

Do you really think the industry which is having 10% of penetration only doesn’t have a multiyear growth.

And the margin that has been a concern so far for everyone I would ask them to wait for one more quarter to see since from this level it will only grow.

The only concern remain here is the growth for me whether it will be sustainable or not at this level but for this I guess we have to give a benefit of doubt to the credibility of the management and their projection of growth.

I think that’s the central finding of behavioral investing and all the great men and women who have contributed to it. Things are just way more unpredictable and random than we think they are but we fail in consistent ways in dealing with that unpredictability.

Ironically, when we try and predict the unpredictable the system just becomes more unpredictable.

By building multiple redundancies into the system. In other words, by having a margin of safety. In TA the margin of safety is the stop loss. In FA, its trying to buy a co well below its true value. Mother nature knows it best because she designed the human body such that if one part fails , you can still continue functioning.

The below medical journal seems to be an apt analogy. When we try to predict the future , we will eventually fail! Works for Business and investing too.

IIM - A has a good case on Big Basket , detailing out the challenges of online grocery and the various models that online grocers follow. Though a bit old - its fairly detailed.

My takeway from the case are the various models that online grocery stores follow

Inventory model followed by Big Basket

Hyper local - where u dont own the supply chain completely

Mobile app based

Hybrid - where the action is shifting slowly.

The other takeway is that delivery costs are the main culprit contributing to loss making online ecommerce firms. There are only so many delivery boys to go around.

This fact is corroborated by the following article

Recently i spoke to a delivery boy from amazon, each delivery they get Rs 20 and if they deliver from 7 am to 10 pm , they make about 70 deliveries per day. This also confirms numbers from the above article.

I am now contemplating leaving my job and becoming a delivery boy for Amazon.

Hi @bheeshma,I am in same page with you . As per the trend in Other Expenses(Including Employee Exp) for past 2 quarters ,we can assume other expenses ratio will be ~ 6.3% for next two quarters which means EBITDA margin will be near ~8.7% by FY19E. Let me know if you think different .