Assuming there isn’t much same store sales growth and the margin improvements are at their peak, is the understanding right that further growth will more or less directly correspond to the percentage of new stores added? This of course assumes that the new stores would be in similar location, similarly sized, catering to similar demographic and will be received the same way. But for simplicity, let’s assume that.

If the above assumptions are right, sooner or later base effect will come into play if they continue to add 20-30 stores per year, going by 131 Stores in FY17 (21 New - 19% new stores) and 155 stores in FY18 (24 New - 18% new stores). From here on, base effect itself should slow down the growth and in addition to it if any of the assumptions in the beginning of this post w.r.t margin deterioration or de-growth in same stores or new store revenues lower than current mean would only adversely impact numbers. None of these would be a problem if this were even trading at 60 P/E.

Yes, a higher base of mature stores will impact the growth rate. However, it should do an earnings growth of 20% -25%. Every time it adds a new store, the unit economics improves and it has recently entered some new clusters.

The reason for the margins that dmart has are structural in nature rather than market led. Low debt, low rent etc are all conscious choices and the quality of margins is much superior so I am not convinced about peak margins. They can improve further is my view and could be wrong about it as well.

The other aspect of dmart is that it pays its suppliers super fast. In essence it funds the working capital needs of its suppliers. If you are a supplier to dmart and it constitutes a major part of your business then you are likely to have a low receivable period and are cash flow positive. This would enable you to grow quickly. The supply chain of dmart is very stable for this reason. The importance of a strong supply chain cannot be highlighted enough in retail. In many cases the main source of working capital financing is not a bank but dmart.

Normal same store sales growth rate for a retail store is 10-12% at an average D-Mart same store growth stands at 14% considering the base effect of 2.2% for GST [so without GST we can consider it at around 16%]. Their historical average was very high which is at 20% but obviously that is not sustainable we all know. But we the reason behind this high same store sales growth is most of store is very new and yet to mature and their strategy to open 20-30 store every year will not only add to new store growth but also as it’s maturity will take 1-2 years at least so it will add up to the high same store sales growth as well.

As I have already mentioned about the valuation I am not very good at specially for a quality company but if market is giving it a PE of 100 even after same store sales growth at 14% which is sustainable if we consider the economy is growing at 7% and consumer staple easily get a growth rate of 14% i.e. 2 times of GDP. So I guess market is having something in it’s mind.

I have already mentioned why black swan effect like Jio is not possible here because this business is a low margin business and having a very high delivery cost compare to the low ticket size so anyone trying give online delivery of a consumer staple is not very sustainable for very long since they can’t offer it at a discount. Also D-Mart is having various moat like low cost producer, strong trusted stable supplier network, hub and spoke model [which I believe the most important for a Retail chain to grow], culture inside the business house [this is very much important to run a low margin business]

See no one can predict if they can open 30 store every year or not. But considering their history they have always done better that what they have committed so for this part of concern we have to give benefit of doubt to the quality of the management.

BTW…If you take Rs 21-22 as next year EPS (from research reports of various research houses) - its already trading at that PE( ~60-65). So, its expensive , however not too much expensive also…consider it as a Big & Strong fish ready to eat other fishes just like Amazon, Google etc…it has the characteristics to be a winner…Now its up to you to convince yourself either way…after all its your money… if it rises, you gain…if it comes down…you lose.

I think what @phreakv6 is trying to point out that if sales growth slows down which is certain to happen due to the growing share of mature stores in the business and margins don’t expand and contract instead which is also possible, the valuations will nosedive violently. This is definitely possible and one must be cognizant of this valuation risk as it is a real one and can take your capital out.

In my view, Valuations have to be taken more seriously and one cannot brush them aside. We have had some discussions around valuations in various threads but not of the same level that we have seen discussions around business happening.

Those invested in Avanti know what peak margins can do to your wealth.

Yes growth will slow down specially the same store sales as I have already mentioned since the saturation level is 12% considering the Industry peers and GDP growth of 7%. D-Mart as per the last quarter stands at 14% but it’s keep on opening 30 store per annum so how can the overall growth will be affected by this at-least in coming 5 years. So the question is how much PE we should give to it? The industry itself having a strong tailwind towards organized players.

That’s what everyone is saying

In the beginning you have 30 stores, add 30 stores (100pc growth)

Next you hv 60 stores, add 30 stores (50pc growth)

Year 3 you have 90 stores, add 30 stores (33pc growth)

HIn FY20 you will be looking at 57 PE multiple if stock remains at the same price. If the company can grow at 20% for next 5 years till say 2025 , and the PE multiple sustains at 57 , you get 14% cagr returns by 2025 from now. It can be 17% if PE multiple is close to 67. I agree to @phreakv6 and you that we have to be aware and look closely at the growth at all points in time till 2025. Margins surely seem to be close to a peak ( may not be full throttle though) , but I think assumption that store sizes are going to be similar as before is not right. Store sizes are becoming bigger , and increase in total sq.foot continues to be above 20%. I am counting on a slight increase in revenue per sq.ft for next 2-3 years , due to a good amount of recent stores becoming more productive and another assumption is no net margin contraction.

Don’t think that @bheeshma is indicating DMART is in peak margin if you go through his earlier posts. Network Economics is yet to play fully so there is still scope of margin expansion.Most Important question is there any 30% + predictable growth quality consumer story available in Market (Non Financial) ? If there it is then it’s valuation premium will decrease otherwise not .The correction which is going one it is across market…

Just came home from a Dmart outlet in Mumbai. The sheer amount of customers inside the store filling up their shopping carts is a delightful scene as an investor.

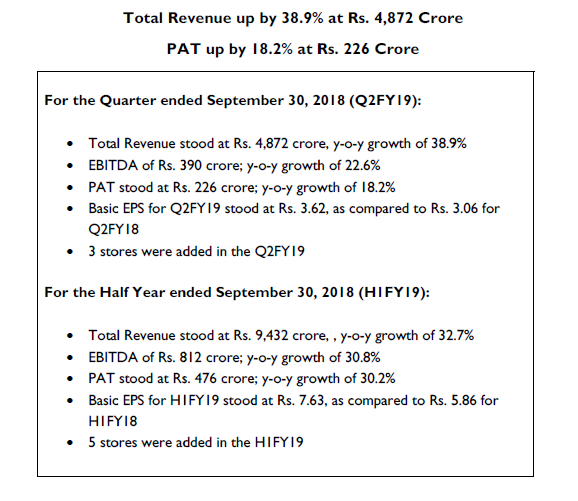

Any specific reason for this margin contraction in q2 while H1 numbers still look ok but not great in the context of high valuation? What is TTM PE it should settle now given this subpar PAT growth in Q2? I had exited @1100 in some family accounts I manage and looked like a bad decision. Would like to get in at right valuation.

Looks like this is the slowest they have grown in their existence. 18% PAT growth with margin compression and only 3 stores in the quarter - Looks like a potent cocktail to me with the current valuations.

I think DMART must undergo some correction considering we are valuing DMART at par with Amazon. DMART is super efficient etc, but the fact is, to grow its business it will need constant capital feeding. The compression in margins are here to stay considering peer pressure from both offline and online. Moreover, DMART is nothing but institutional version of my nearby Kirana Store (more than 70% sales from daily needs). Also many people look at YoY of these kind of business which is again wrong in my opinion. It should be seen as sequential SSG with some approximation of base period.

Does it not result actually good? 40% increase in sales.Expense increased due to increase in Change in inventories of stock-in-trade (-225 from -335) which can be sorted out in coming quarters.