When I say “fair knowledge”, I mean knowledge of stastics. I’m not pulling the numbers out of thin air. I can show you a normal distribution of the Cost of Capital for Indian Corporates. But I can see that you’re not interested (Since you clearly didn’t understand what I was trying to say).

Regarding your second point about me becoming rich, that’s a really childish way of looking at things. We’re all here to learn. I hope in the future you’re more open to healthy debates, rather than turning every conversation into a pissing contest.

Look up Ernst and young study mate

The cost of capital is not 10pc and not across all industries

I didn’t ask your personal wealth score, I meant none of the model and efficient market theory or the analysts that use them have managed to create wealth for themselves

When you take a normal analyst study route or as a ca the first thing they teach you is market is highly efficient and then they ask you to memorise it and test your knowledge

It becomes part of you and like the Chinese who take prisioners of war and start with small requests in writing on why your country is not great you keep on adding to that thought that the markets are efficient and the models are correct

Dinesh,

Keep those numbers coming, we are here to learn new things. Remember using the capm model while doing the MBA, based on the risk free rate, D/E ration and long term expected returns from equity of 15%. Remember the valuation exercise used to be an exercise in tweaking excel so that the share price reaches close to market value.The terminal value forms a large part of the share price which is difficult to predict.

The other option is what Pabrai suggests, consider as if you are holding the business for 10 years and then sell the business for x times the cash flow of 10th year. Don’t remember the x now,but was there in the book(Dhando investor).

You did a valuation for KRBL, but one single incident made the valuation go all awry. Looks like it is a dynamic exercise or you could view KRBL as undervalued.

Yes, all of those things still remain the same, except the long-term return on the indices is about 13% now. The terminal value still forms a large part of the total Value, but the Terminal Value depends a lot on the assumptions you make for the High Growth period, so it’s not as bad as you think. Prof. Damodaran wrote a very informative post addressing this question:

Yes, even Prof. Bakshi uses this kind of a Valuation model, made popular by none other than Mr. Charlie Munger, in his famous 1966 talk Practical Thought on Practical Thought (He values Coco-Cola):

However, nobody I know has explained the ‘exit multiple’ using fundamentals (So it appears to be a random number picked out of nowhere, when in fact it is not). Prof. Bakshi touches upon this in his Relaxo Lecture:

You can follow my thread Numbers and Narratives to know what changes I made to the original Valuation of KRBL (In short, someone pointed out a few silly mistakes I had made and I changed them). I have not updated the excel otherwise. You can view it here, which would show that KRBL is slightly overvalued. I don’t think the illegal trading row has any bearing on the fundamentals of KRBL in the long term, but of course, the trust of the promoters has gone for a toss (Which is obviously a very tricky thing to assess, so much so that even investors like Pabrai weren’t able to do it properly).

A note on my Valuations is that, since my public Valuations tend to be viewed by many people, it would be illogical to impose my risk-aversion on the model. Personally, I always use a 15% Discounting Rate and a 30% Mos (Whereas in the KRBL exercise, I used a 9.41% CAPM-based Discounting Rate and a 5% MoS).

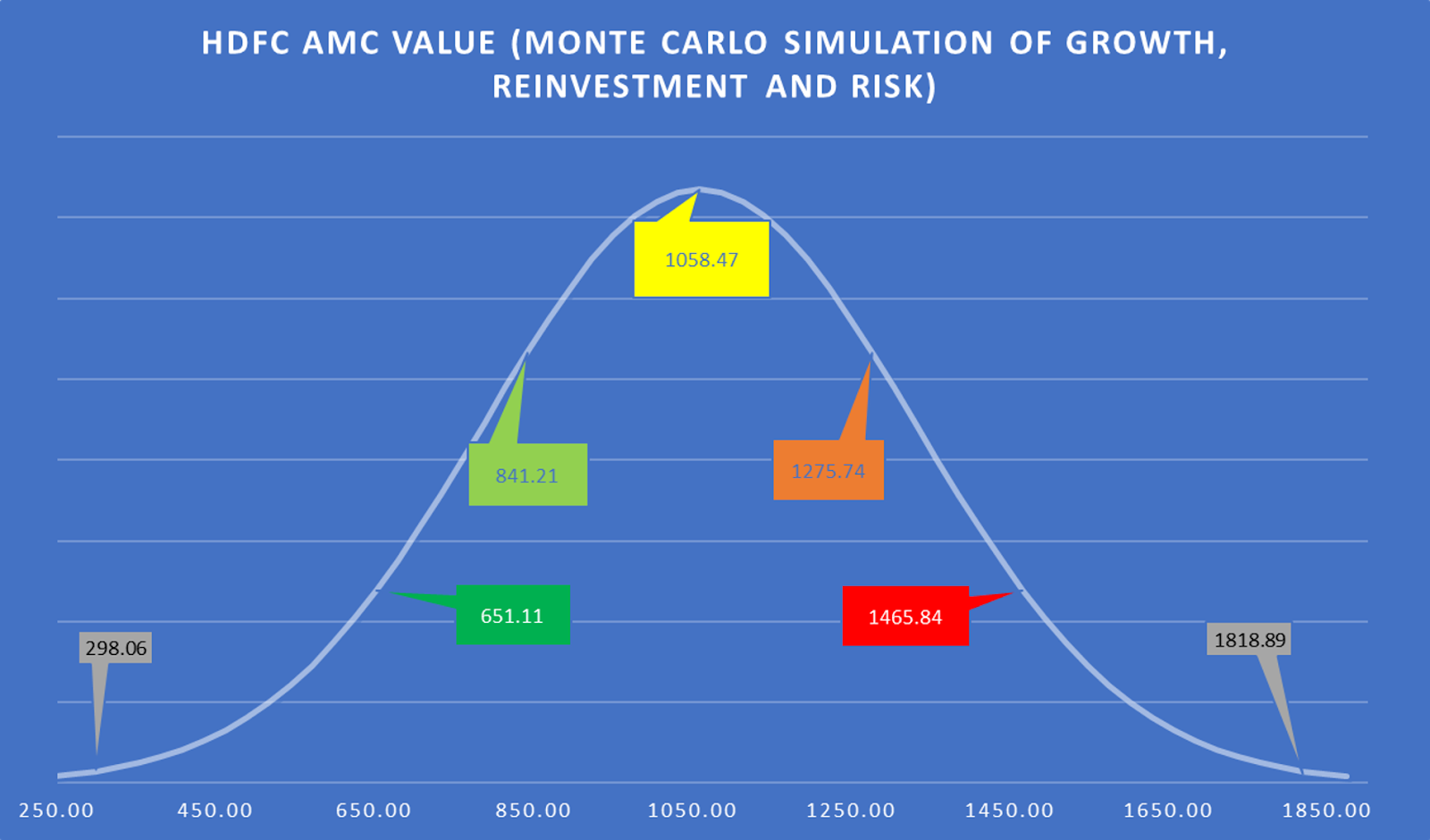

You can understand how this would affect my public Valuations Vs my Valuations for personal use. However, I never fail to post a ‘range of Values’, to allow people to decided the Value for themselves personally. I do this based on a Monte-Carlo simulation. I recently Valued HDFC AMC at Rs. 1011. But my ‘range of Values’ showed this:

Today I was discussing with One of my Friend regarding above mentioned posts of Valuation Model,Exit Multiples etc of this thread , After going through these he told me "Thank God I was not aware of this valuation Models,Exit Multiples else I would miss my 6 Bagger Page which I am remain invested from 2013 “, " You know not knowing is some kind of protection and it is also give you the courage to decide .The more you know you become indecisive.”

When every sell side analysts shouting Sell Sell Sell for past 1.5 years but the stock is refusing to come down then the problem is not with the stock. It is with those analysts. They don’t have any clue how they will fit their analysis in Excel Valuation Model . Excel Investing at its best !!!

The great thing about Valuing stocks for yourself is you don’t have to adhere to the market. Your example is cherry-picking at its best. If I showed an example of a stock being Statically Overvalued at some point and actually crashing or going sideways afterwards, would you agree that the model works? That’s exactly what you’re asking people to do (Well, the opposite) with your Page example.

That’s not the point of Valuing a stock at all. No Analyst worth his salt will claim that his model Values are accurate. Nobody’s model will be. The point is to arrive at a baseline price (According to your estimates) and then buying way below that level.

On a corollary note, another great thing about the stock market is that great opportunities are always around the corner. You just have to buy into the opportunity when your idea of Value (Whatever it may be) is above the Price. If your idea of Value is that “I believe in the management and I think the historical performance is great”, then that’s speculation, since there’s no input on the decision making from your side.

Agree 100pc but no body said that management quality alone is sole criteria in the discussion

They raised 1870 crore in equity last time and are now they are raising 1500 crore in debt in tranches

Cash flow of dcf needs assumptions

The call really is if they can do even 1/10 if what Wal-Mart did in USA

Wal-Mart is 3pc of USA gdp

Dmart is 0.01pc of Indian gdp

What form of finance is best I don’t know, the management apparently doesn’t want to dilute else they could have easily raised more capital

It’s run by someone who has been and studied in USA and has a good exposure on Indian markets

Ofcourse you’d want a company that can be run by monkeys and still make money if time comes to that. Does the business need mba quality of personnel to run

Or is it a relatively straightforward business

Where does DMart’s financial information figure in your thesis? Are you telling me that you’ll be able to make an investment decision without looking at a company’s financial statements and figuring out a Value for the company?

If the answer is no, I request you to kindly make your case for DMart’s Value (Not the Market Cap, but a Value to you personally) based on the company’s financials.

Hi Dinesh

I don’t think nobody is here telling that take decision only by looking at management ,business or financial. You need to consider everything but excel should be given very less importance for quality investing.

Let me give you an example . You applied this same excel formulas and derived KRBL’s value price at Rs 540 on March,18 but see where the price is now. So my advise is to you don’t try to put your formula’s everywhere . You will do a grave mistake if you fit DMART,PIDILITE,PAGE,BRITANNIA and KRBL in single excel format.So to judge quality companies you need to consider to look at bigger picture which is an Art not science. I am neither criticizing your approach/valuation model just only telling you, it does not work for all companies specially qualities

Rest depend on you Best of Luck !

The spreadsheet is basic

I use something similar and autohotkey populates screener figures into the spreadsheet so I can do the basic analysis of many companies very fast before doing more research

But I wouldn’t just use it for my buy decision

Look ht media for instance, it’s so undervalued, owner of good newspapers, online and offline

You can have a billion ton of Rdx in your warehouse. To explode, you also need a spark

I take it from your response that you did not read the entire thread, but simply picked out response that supported your argument.

I’ve said it here a few posts back and even in the Numbers and Narratives thread, that someone pointed out some silly mistakes I’d made and I did the changes. As per my model, KRBL is slightly overvalued now. I’d even provided a link to the updated model, which again I figure, you didn’t look at. Please take a moment to read my words just a few posts back.

But apart from that, the model can be used to Value everything ranging from KRBL to Apple (As an aside, the model has an option to display the figures in upto 20 different currencies). Like I’ve said time and again, it’s not the model that’s inaccurate, it’s the ability of the Valuer to use sensible assumptions and then support them with facts grounded in reality that breaks or makes it.

That’s wonderful. Please do share your spreadsheet for Avenue Supermart. I’m most interested in understanding how you justify its Value to you personally.

If someone figures out a method to know what stock price will be next Friday, and the information is then made public knowledge, and if the current price is trading at 25pc lower, someone will buy it today. Over a course of few minutes, so many people will buy it today that the expected price of next Friday will be realised a week in advance

Once a method call it dcf or anything is known it’s no longer effective to predict future value

There are many companies that trade at a discount. I gave you h t media, why don’t you buy that’s if your value doesn’t consider things like market size, management history, product they are selling, demand etc

The method of “figuring out value” differs from person to person. Even if we assume that the entire world uses a DCF model, there would still be varying estimates of Value… because Value is personal. Risk is personal. So your argument doesn’t hold water.

Even assuming it does… does it mean that, since you already mentioned that Avenue Supermart can be Valued using 0.03% of India’s GDP, it will make the market buy up the stock and thus make the stock an unattractive investment? So does this mean you will be selling the stock soon? See how ridiculous that argument sounds? That’s how yours sounds to me.

It is not my Value. That’s he beauty of Valuation. You could find a stock undervalued, I could find it overvalued and we’d both be right.

Also, feel free to answer my question any time:

The onus of this discussion is about how you arrived at a Value for Avenue Supermart. Let’s not distract ourselves.

Use the growth of 13pc in your spreadsheet and it will arrive at valuation today

But Dmart grow much more faster than that

They would want to have a first mover advantage

And the new debenture issue is pointing towards that

Yes they also research many many companies

If you are not good at maths you atleast need to be very good at populating spreadsheets

It should take one second to populate and arrive at a basic value

Will you buy everything that comes up as a value, no

You will look further

You are selling dcf as an all important decision making tool

Either be good at maths or be good and populating excel really fast

If munger would be looking at Dmart, he would have already spent his first 2 seconds to arrive at dcf and then spend his next days researching further

When? Please make a quote of one of my posts where I did that.

Valuation is the final frontier. You don’t Value a company and then research it. You research it, build a sense of the business and then Value it.

I sold a DCF (Or Valuation in general) as an important part of investment decision making. It’s not everything in investing, but one of the most important things.

After doing that, I simply asked for your Valuation for DMart, since I wanted to compare notes. You blatantly denied this, even though, according to you, all it takes is a click on Screener. And you accused me of finding faults in your Valuation (When I haven’t even looked at yours). I don’t Value a company unless I research and understand the business (Which takes time). Since you’re already interested in the company, I thought you already did the due research. But it looks like you haven’t. My bad for asking.

So sure, it doesn’t make sense to continue this conversation anymore. I’d still keep my promise of Valuing DMart, even if you don’t keep yours.